SPM

Summary

for Policymakers

Coordinating Lead Authors:

Ottmar Edenhofer (Germany), Ramon Pichs-Madruga (Cuba),

Youba Sokona (Ethiopia/Mali), Kristin Seyboth (Germany/USA)

Lead Authors:

Dan Arvizu (USA), Thomas Bruckner (Germany), John Christensen (Denmark),

Helena Chum (USA/Brazil) Jean-Michel Devernay (France), Andre Faaij (The Netherlands),

Manfred Fischedick (Germany), Barry Goldstein (Australia), Gerrit Hansen (Germany),

John Huckerby (New Zealand), Arnulf Jäger-Waldau (Italy/Germany), Susanne Kadner (Germany),

Daniel Kammen (USA), Volker Krey (Austria/Germany), Arun Kumar (India),

Anthony Lewis (Ireland), Oswaldo Lucon (Brazil), Patrick Matschoss (Germany),

Lourdes Maurice (USA), Catherine Mitchell (United Kingdom), William Moomaw (USA),

José Moreira (Brazil), Alain Nadai (France), Lars J. Nilsson (Sweden), John Nyboer (Canada),

Atiq Rahman (Bangladesh), Jayant Sathaye (USA), Janet Sawin (USA), Roberto Schaeffer (Brazil),

Tormod Schei (Norway), Steffen Schlömer (Germany), Ralph Sims (New Zealand),

Christoph von Stechow (Germany), Aviel Verbruggen (Belgium), Kevin Urama (Kenya/Nigeria),

Ryan Wiser (USA), Francis Yamba (Zambia), Timm Zwickel (Germany

)

Special Advisor:

Jeffrey Logan (USA)

This chapter should be cited as:

IPCC, 2011: Summary for Policymakers. In: IPCC Special Report on Renewable Energy Sources and Climate Change Mitigation

[O. Edenhofer, R. Pichs-Madruga, Y. Sokona, K. Seyboth, P. Matschoss, S. Kadner, T. Zwickel, P. Eickemeier, G. Hansen,

S. Schlömer, C. von Stechow (eds)], Cambridge University Press, Cambridge, United Kingdom and New York, NY, USA.

4

Summary for Policymakers Summaries

Summaries Summary for Policymakers

5

Table of Contents

1. Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6

2. Renewable energy and climate change . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7

3. Renewable energy technologies and markets . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7

4. Integration into present and future energy systems . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 15

5. Renewable energy and sustainable development . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 18

6. Mitigation potentials and costs . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 20

7. Policy, implementation and fi nancing . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 24

8. Advancing knowledge about renewable energy . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 26

6

1. Introduction

The Working Group III Special Report on Renewable Energy Sources and Climate Change Mitigation (SRREN) presents

an assessment of the literature on the scientifi c, technological, environmental, economic and social aspects of the

contribution of six renewable energy (RE) sources to the mitigation of climate change. It is intended to provide policy

relevant information to governments, intergovernmental processes and other interested parties. This Summary for

Policymakers provides an overview of the SRREN, summarizing the essential fi ndings.

The SRREN consists of 11 chapters. Chapter 1 sets the context for RE and climate change; Chapters 2 through 7 provide

information on six RE technologies, and Chapters 8 through 11 address integrative issues (see Figure SPM.1).

2. Bioenergy

3. Direct Solar Energy

4. Geothermal Energy

5. Hydropower

6. Ocean Energy

7. Wind Energy

1. Renewable Energy and Climate Change

8. Integration of Renewable Energy into Present and Future Energy Systems

9. Renewable Energy in the Context of Sustainable Development

10. Mitigation Potential and Costs

11. Policy, Financing and Implementation

Integrative Chapters

Introductory Chapter

Technology Chapters

Special Report on Renewable Energy Sources and Climate Change Mitigation

Figure SPM.1 | Structure of the SRREN. [Figure 1.1, 1.1.2]

References to chapters and sections are indicated with corresponding chapter and section numbers in square brackets. An

explanation of terms, acronyms and chemical symbols used in this SPM can be found in the glossary of the SRREN (Annex I).

Conventions and methodologies for determining costs, primary energy and other topics of analysis can be found in Annex II

and Annex III. This report communicates uncertainty where relevant.

1

1 This report communicates uncertainty, for example, by showing the results of sensitivity analyses and by quantitatively presenting ranges in cost

numbers as well as ranges in the scenario results. This report does not apply formal IPCC uncertainty terminology because at the time of the

approval of this report, IPCC uncertainty guidance was in the process of being revised.

Summary for Policymakers Summaries

7

Summaries Summary for Policymakers

2. Renewable energy and climate change

Demand for energy and associated services, to meet social and economic development and improve human

welfare and health, is increasing. All societies require energy services to meet basic human needs (e.g., lighting,

cooking, space comfort, mobility and communication) and to serve productive processes. [1.1.1, 9.3.2] Since approxi-

mately 1850, global use of fossil fuels (coal, oil and gas) has increased to dominate energy supply, leading to a rapid

growth in carbon dioxide (CO

2

) emissions. [Figure 1.6]

Greenhouse gas (GHG) emissions resulting from the provision of energy services have contributed signifi -

cantly to the historic increase in atmospheric GHG concentrations. The IPCC Fourth Assessment Report (AR4)

concluded that “Most of the observed increase in global average temperature since the mid-20th century is very likely

2

due to the observed increase in anthropogenic greenhouse gas concentrations.”

Recent data confi rm that consumption of fossil fuels accounts for the majority of global anthropogenic GHG

emissions.

3

Emissions continue to grow and CO

2

concentrations had increased to over 390 ppm, or 39% above prein-

dustrial levels, by the end of 2010. [1.1.1, 1.1.3]

There are multiple options for lowering GHG emissions from the energy system while still satisfying the

global demand for energy services. [1.1.3, 10.1] Some of these possible options, such as energy conservation and

effi ciency, fossil fuel switching, RE, nuclear and carbon capture and storage (CCS) were assessed in the AR4. A com-

prehensive evaluation of any portfolio of mitigation options would involve an evaluation of their respective mitigation

potential as well as their contribution to sustainable development and all associated risks and costs. [1.1.6] This report

will concentrate on the role that the deployment of RE technologies can play within such a portfolio of mitigation

options.

As well as having a large potential to mitigate climate change, RE can provide wider benefi ts. RE may, if

implemented properly, contribute to social and economic development, energy access, a secure energy supply, and

reducing negative impacts on the environment and health. [9.2, 9.3]

Under most conditions, increasing the share of RE in the energy mix will require policies to stimulate

changes in the energy system. Deployment of RE technologies has increased rapidly in recent years, and their share

is projected to increase substantially under most ambitious mitigation scenarios [1.1.5, 10.2]. Additional policies would

be required to attract the necessary increases in investment in technologies and infrastructure. [11.4.3, 11.5, 11.6.1,

11.7.5]

3. Renewable energy technologies and markets

RE comprises a heterogeneous class of technologies (Box SPM.1). Various types of RE can supply electricity, ther-

mal energy and mechanical energy, as well as produce fuels that are able to satisfy multiple energy service needs [1.2].

Some RE technologies can be deployed at the point of use (decentralized) in rural and urban environments, whereas

others are primarily deployed within large (centralized) energy networks [1.2, 8.2, 8.3, 9.3.2]. Though a growing

number of RE technologies are technically mature and are being deployed at signifi cant scale, others are in an earlier

phase of technical maturity and commercial deployment or fi ll specialized niche markets [1.2]. The energy output of

2 According to the formal uncertainty language used in the AR4, the term ‘very likely’ refers to a >90% assessed probability of occurrence.

3 The contributions of individual anthropogenic GHGs to total emissions in 2004, reported in AR4, expressed as CO

2

eq were: CO

2

from fossil

fuels (56.6%), CO

2

from deforestation, decay of biomass etc. (17.3%), CO

2

from other (2.8%), methane (14.3%), nitrous oxide (7.9%) and

fl uorinated gases (1.1%) [Figure 1.1b, AR4, WG III, Chapter 1. For further information on sectoral emissions, including forestry, see also Figure

1.3b and associated footnotes.]

8

Summary for Policymakers Summaries

RE technologies can be (i) variable and—to some degree—unpredictable over differing time scales (from minutes to

years), (ii) variable but predictable, (iii) constant, or (iv) controllable. [8.2, 8.3]

Box SPM.1 | Renewable energy sources and technologies considered in this report.

Bioenergy can be produced from a variety of biomass feedstocks, including forest, agricultural and livestock residues; short-rotation

forest plantations; energy crops; the organic component of municipal solid waste; and other organic waste streams. Through a variety

of processes, these feedstocks can be directly used to produce electricity or heat, or can be used to create gaseous, liquid, or solid fuels.

The range of bioenergy technologies is broad and the technical maturity varies substantially. Some examples of commercially available

technologies include small- and large-scale boilers, domestic pellet-based heating systems, and ethanol production from sugar and starch.

Advanced biomass integrated gasifi cation combined-cycle power plants and lignocellulose-based transport fuels are examples of technol-

ogies that are at a pre-commercial stage, while liquid biofuel production from algae and some other biological conversion approaches are

at the research and development (R&D) phase. Bioenergy technologies have applications in centralized and decentralized settings, with

the traditional use of biomass in developing countries being the most widespread current application.

4

Bioenergy typically offers constant

or controllable output. Bioenergy projects usually depend on local and regional fuel supply availability, but recent developments show

that solid biomass and liquid biofuels are increasingly traded internationally. [1.2, 2.1, 2.3, 2.6, 8.2, 8.3]

Direct solar energy technologies harness the energy of solar irradiance to produce electricity using photovoltaics (PV) and concentrat-

ing solar power (CSP), to produce thermal energy (heating or cooling, either through passive or active means), to meet direct lighting

needs and, potentially, to produce fuels that might be used for transport and other purposes. The technology maturity of solar applica-

tions ranges from R&D (e.g., fuels produced from solar energy), to relatively mature (e.g., CSP), to mature (e.g., passive and active solar

heating, and wafer-based silicon PV). Many but not all of the technologies are modular in nature, allowing their use in both centralized

and decentralized energy systems. Solar energy is variable and, to some degree, unpredictable, though the temporal profi le of solar

energy output in some circumstances correlates relatively well with energy demands. Thermal energy storage offers the option to improve

output control for some technologies such as CSP and direct solar heating. [1.2, 3.1, 3.3, 3.5, 3.7, 8.2, 8.3]

Geothermal energy utilizes the accessible thermal energy from the Earth’s interior. Heat is extracted from geothermal reservoirs using

wells or other means. Reservoirs that are naturally suffi ciently hot and permeable are called hydrothermal reservoirs, whereas reservoirs

that are suffi ciently hot but that are improved with hydraulic stimulation are called enhanced geothermal systems (EGS). Once at the sur-

face, fl uids of various temperatures can be used to generate electricity or can be used more directly for applications that require thermal

energy, including district heating or the use of lower-temperature heat from shallow wells for geothermal heat pumps used in heating

or cooling applications. Hydrothermal power plants and thermal applications of geothermal energy are mature technologies, whereas

EGS projects are in the demonstration and pilot phase while also undergoing R&D. When used to generate electricity, geothermal power

plants typically offer constant output. [1.2, 4.1, 4.3, 8.2, 8.3]

Hydropower harnesses the energy of water moving from higher to lower elevations, primarily to generate electricity. Hydropower proj-

ects encompass dam projects with reservoirs, run-of-river and in-stream projects and cover a continuum in project scale. This variety gives

hydropower the ability to meet large centralized urban needs as well as decentralized rural needs. Hydropower technologies are mature.

Hydropower projects exploit a resource that varies temporally. However, the controllable output provided by hydropower facilities that

have reservoirs can be used to meet peak electricity demands and help to balance electricity systems that have large amounts of variable

RE generation. The operation of hydropower reservoirs often refl ects their multiple uses, for example, drinking water, irrigation, fl ood and

drought control, and navigation, as well as energy supply. [1.2, 5.1, 5.3, 5.5, 5.10, 8.2]

4 Traditional biomass is defi ned by the International Energy Agency (IEA) as biomass consumption in the residential sector in developing countries and refers to the

often unsustainable use of wood, charcoal, agricultural residues, and animal dung for cooking and heating. All other biomass use is defi ned as modern [Annex I].

9

Summaries Summary for Policymakers

Ocean energy derives from the potential, kinetic, thermal and chemical energy of seawater, which can be transformed to provide elec-

tricity, thermal energy, or potable water. A wide range of technologies are possible, such as barrages for tidal range, submarine turbines

for tidal and ocean currents, heat exchangers for ocean thermal energy conversion, and a variety of devices to harness the energy of

waves and salinity gradients. Ocean technologies, with the exception of tidal barrages, are at the demonstration and pilot project phases

and many require additional R&D. Some of the technologies have variable energy output profi les with differing levels of predictability

(e.g., wave, tidal range and current), while others may be capable of near-constant or even controllable operation (e.g., ocean thermal

and salinity gradient). [1.2, 6.1, 6.2, 6.3, 6.4, 6.6, 8.2]

Wind energy harnesses the kinetic energy of moving air. The primary application of relevance to climate change mitigation is to produce

electricity from large wind turbines located on land (onshore) or in sea- or freshwater (offshore). Onshore wind energy technologies are

already being manufactured and deployed on a large scale. Offshore wind energy technologies have greater potential for continued tech-

nical advancement. Wind electricity is both variable and, to some degree, unpredictable, but experience and detailed studies from many

regions have shown that the integration of wind energy generally poses no insurmountable technical barriers. [1.2, 7.1, 7.3, 7.5, 7.7, 8.2]

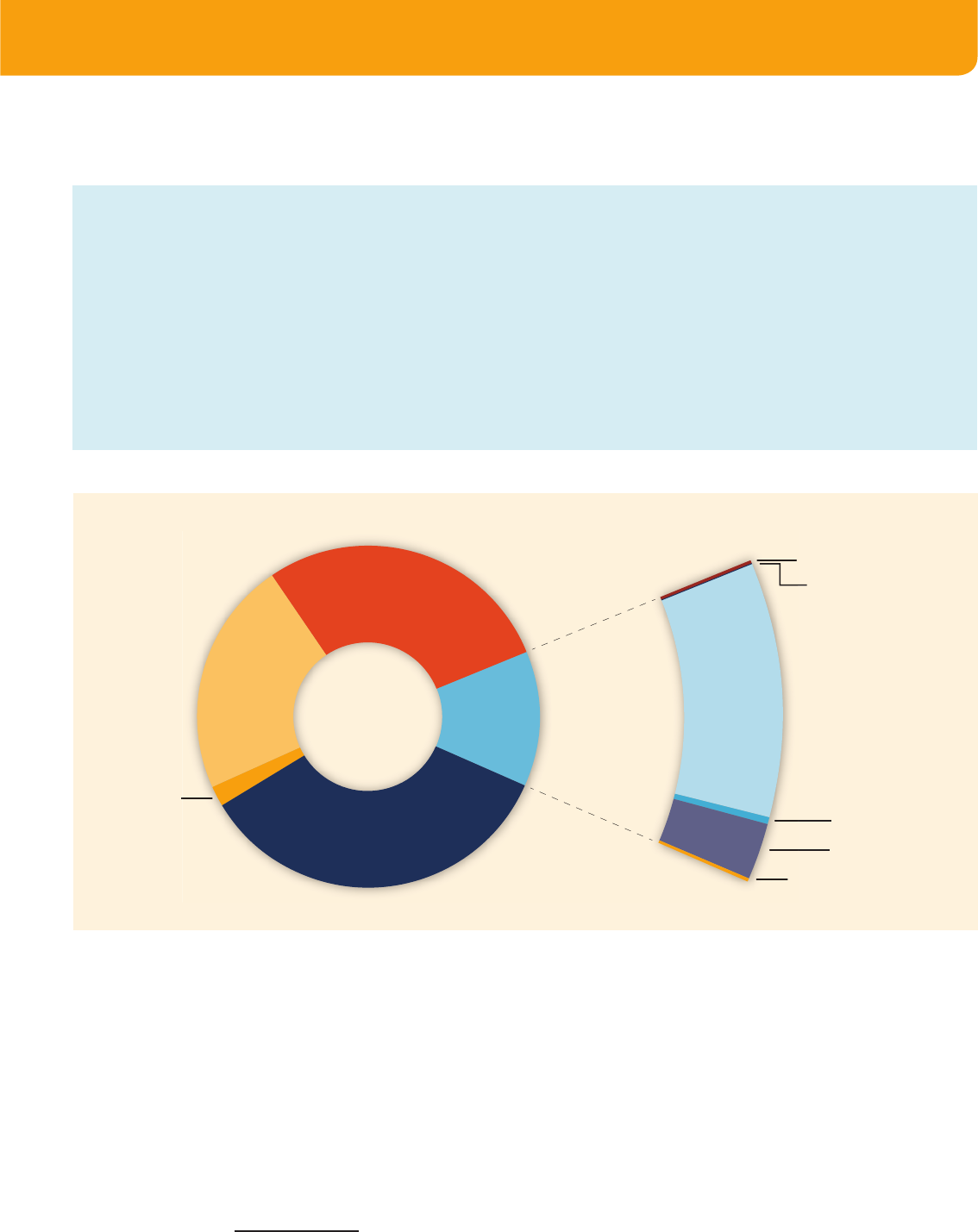

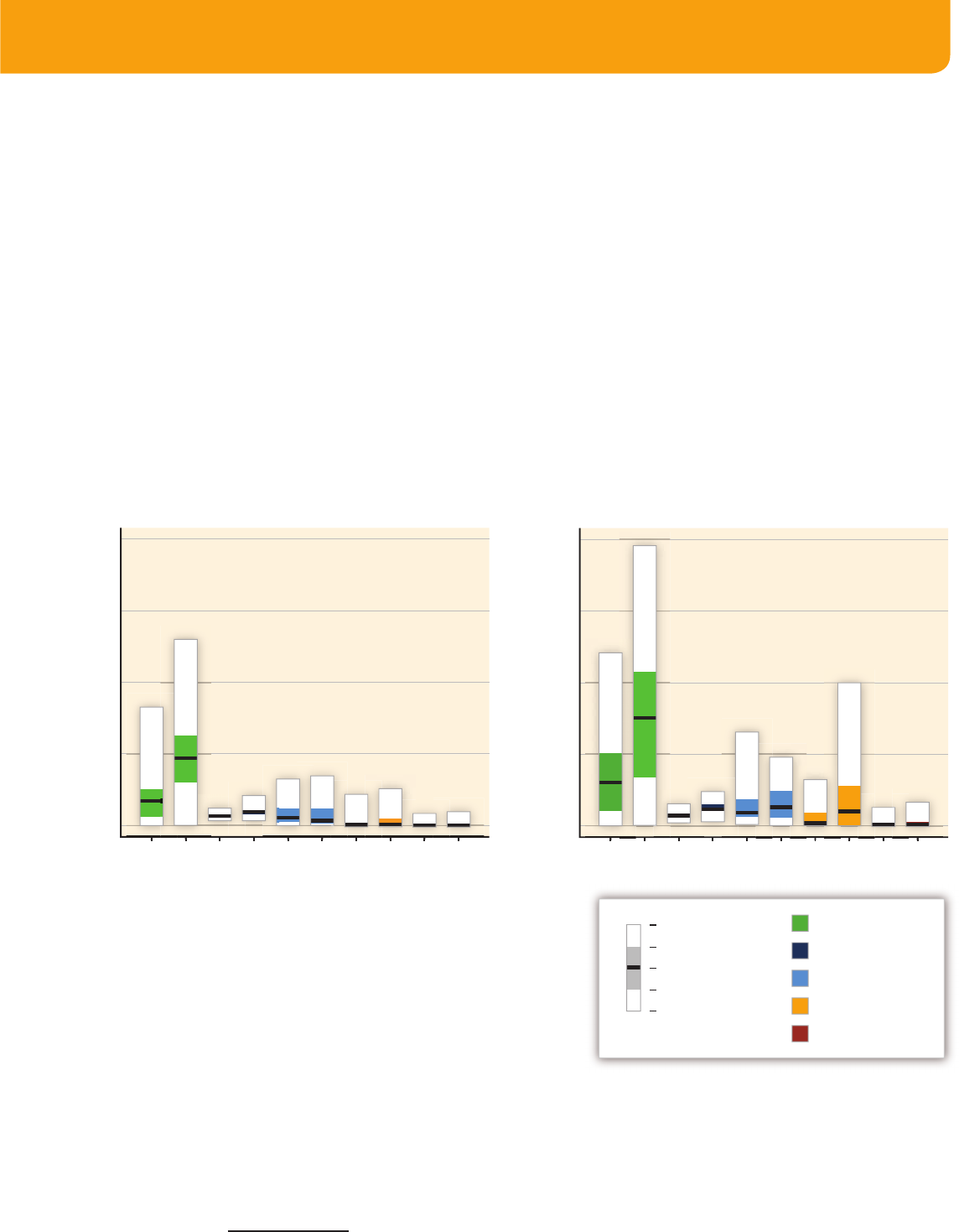

On a global basis, it is estimated that RE accounted for 12.9% of the total 492 Exajoules (EJ)

5

of primary

energy supply in 2008 (Box SPM.2 and Figure SPM.2). The largest RE contributor was biomass (10.2%), with the

majority (roughly 60%) being traditional biomass used in cooking and heating applications in developing countries

but with rapidly increasing use of modern biomass as well.

6

Hydropower represented 2.3%, whereas other RE sources

accounted for 0.4%. [1.1.5] In 2008, RE contributed approximately 19% of global electricity supply (16% hydropower,

3% other RE) and biofuels contributed 2% of global road transport fuel supply. Traditional biomass (17%), modern

biomass (8%), solar thermal and geothermal energy (2%) together fuelled 27% of the total global demand for heat. The

contribution of RE to primary energy supply varies substantially by country and region. [1.1.5, 1.3.1, 8.1]

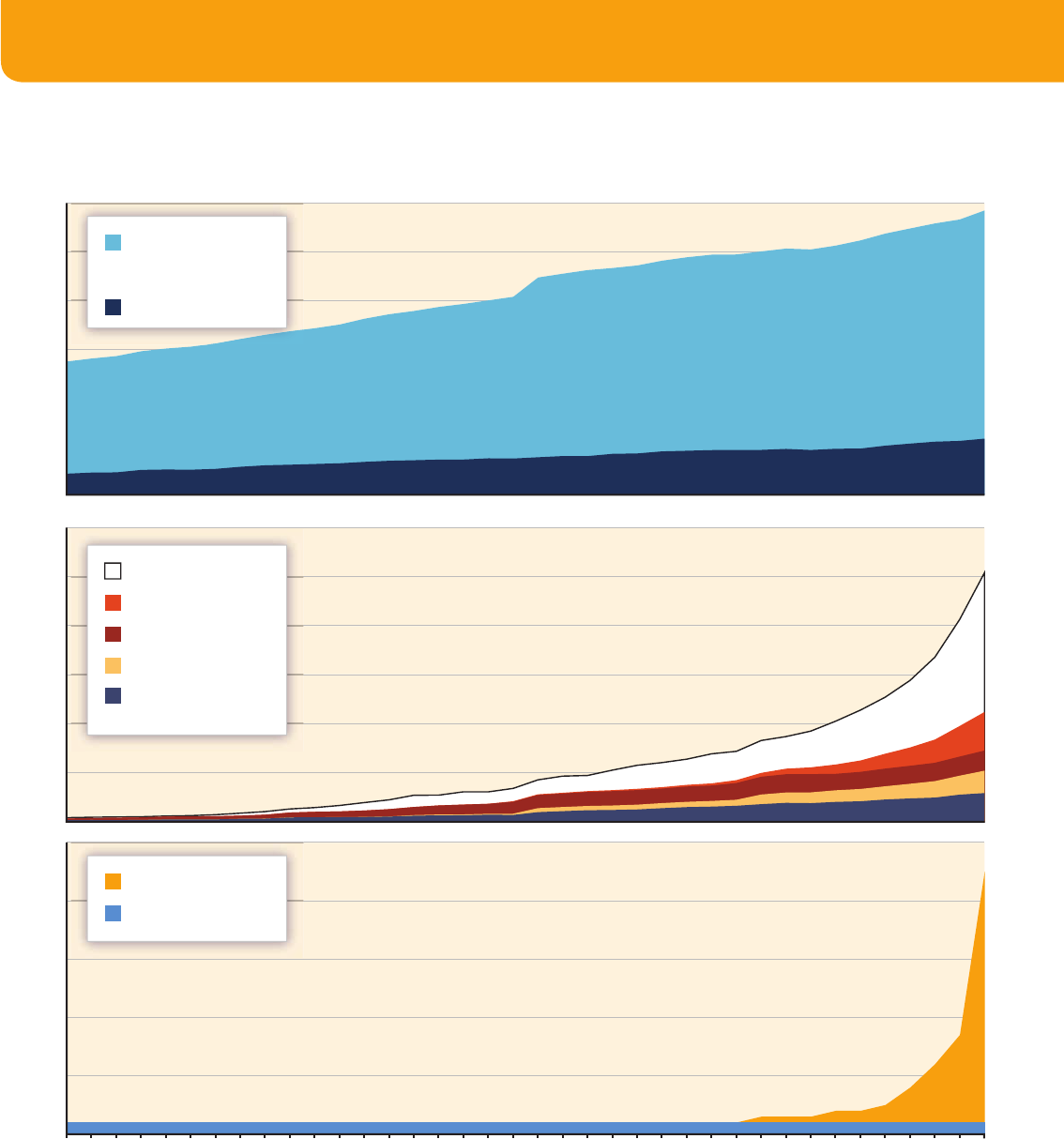

Deployment of RE has been increasing rapidly in recent years (Figure SPM.3). Various types of government poli-

cies, the declining cost of many RE technologies, changes in the prices of fossil fuels, an increase of energy demand and

other factors have encouraged the continuing increase in the use of RE. [1.1.5, 9.3, 10.5, 11.2, 11.3] Despite global

fi nancial challenges, RE capacity continued to grow rapidly in 2009 compared to the cumulative installed capacity from

the previous year, including wind power (32% increase, 38 Gigawatts (GW) added), hydropower (3%, 31 GW added),

grid-connected photovoltaics (53%, 7.5 GW added), geothermal power (4%, 0.4 GW added), and solar hot water/heat-

ing (21%, 31 GW

th

added). Biofuels accounted for 2% of global road transport fuel demand in 2008 and nearly 3% in

2009. The annual production of ethanol increased to 1.6 EJ (76 billion litres) by the end of 2009 and biodiesel to 0.6 EJ

(17 billion litres). [1.1.5, 2.4, 3.4, 4.4, 5.4, 7.4]

Of the approximate 300 GW of new electricity generating capacity added globally over the two-year period from 2008

to 2009, 140 GW came from RE additions. Collectively, developing countries host 53% of global RE electricity genera-

tion capacity [1.1.5]. At the end of 2009, the use of RE in hot water/heating markets included modern biomass (270

GW

th

), solar (180 GW

th

), and geothermal (60 GW

th

). The use of decentralized RE (excluding traditional biomass) in

meeting rural energy needs at the household or village level has also increased, including hydropower stations, various

modern biomass options, PV, wind or hybrid systems that combine multiple technologies. [1.1.5, 2.4, 3.4, 4.4, 5.4]

5 1 Exajoule = 10

18

joules = 23.88 million tonnes of oil equivalent (Mtoe).

6 In addition to this 60% share of traditional biomass, there is biomass use estimated to amount to 20 to 40% not reported in offi cial primary

energy databases, such as dung, unaccounted production of charcoal, illegal logging, fuelwood gathering, and agricultural residue use. [2.1, 2.5]

10

Summary for Policymakers Summaries

The global technical potential

7

of RE sources will not limit continued growth in the use of RE. A wide range

of estimates is provided in the literature, but studies have consistently found that the total global technical potential

for RE is substantially higher than global energy demand (Figure SPM.4) [1.2.2, 10.3, Annex II]. The technical potential

for solar energy is the highest among the RE sources, but substantial technical potential exists for all six RE sources.

Even in regions with relatively low levels of technical potential for any individual RE source, there are typically sig-

nifi cant opportunities for increased deployment compared to current levels. [1.2.2, 2.2, 2.8, 3.2, 4.2, 5.2, 6.2, 6.4, 7.2,

8.2, 8.3, 10.3] In the longer term and at higher deployment levels, however, technical potentials indicate a limit to the

7 Defi nitions of technical potential often vary by study. ‘Technical potential’ is used in the SRREN as the amount of RE output obtainable by

full implementation of demonstrated technologies or practices. No explicit reference to costs, barriers or policies is made. Technical potentials

reported in the literature and assessed in the SRREN, however, may have taken into account practical constraints and when explicitly stated

they are generally indicated in the underlying report. [Annex I]

Figure SPM.2 | Shares of energy sources in total global primary energy supply in 2008 (492 EJ). Modern biomass contributes 38% of the total biomass share. [Figure 1.10, 1.1.5]

Note: Underlying data for fi gure have been converted to the ‘direct equivalent’ method of accounting for primary energy supply. [Box SPM.2, 1.1.9, Annex II.4]

Wind Energy 0.2%

Geothermal Energy 0.1%

Ocean Energy 0.002%

Direct Solar Energy 0.1%

Gas

22.1%

Coal

28.4%

RE

12.9%

Oil

34.6%

Nuclear

Energy 2.0%

Hydropower 2.3%

Bioenergy

10.2%

Box SPM.2 | Accounting for primary energy in the SRREN.

There is no single, unambiguous accounting method for calculating primary energy from non-combustible energy sources such as non-

combustible RE sources and nuclear energy. The SRREN adopts the ‘direct equivalent’ method for accounting for primary energy supply.

In this method, fossil fuels and bioenergy are accounted for based on their heating value while non-combustible energy sources, includ-

ing nuclear energy and all non-combustible RE, are accounted for based on the secondary energy that they produce. This may lead to an

understatement of the contribution of non-combustible RE and nuclear compared to bioenergy and fossil fuels by a factor of roughly 1.2

up to 3. The selection of the accounting method also impacts the relative shares of different individual energy sources. Comparisons in

the data and fi gures presented in the SRREN between fossil fuels and bioenergy on the one hand, and non-combustible RE and nuclear

energy on the other, refl ect this accounting method. [1.1.9, Annex II.4]

11

Summaries Summary for Policymakers

Biofuels (incl. Biogas)

Wind Energy

Geothermal Energy

Solar Thermal Energy

Municipal Solid Waste

(Renewable Share)

Primary Solid Biomass

for Heat and Electricity

Applications

Hydropower

Global Primary Energy Supply [EJ/yr]

0

10

20

30

40

50

60

0

1

2

3

4

5

Solar PV Energy

Ocean Energy

0.00

0.01

0.02

0.03

0.04

0

.

05

2008200620042002200019981996199419921990198819861984198219801978197619741972

Figure SPM.3 | Historical development of global primary energy supply from renewable energy from 1971 to 2008. [Figure 1.12, 1.1.5]

Notes: Technologies are referenced to separate vertical units for display purposes only. Underlying data for fi gure has been converted to the ‘direct equivalent’ method of accounting

for primary energy supply [Box SPM.2, 1.1.9, Annex II.4], except that the energy content of biofuels is reported in secondary energy terms (the primary biomass used to produce the

biofuel would be higher due to conversion losses. [2.3, 2.4])

contribution of some individual RE technologies. Factors such as sustainability concerns [9.3], public acceptance [9.5],

system integration and infrastructure constraints [8.2], or economic factors [10.3] may also limit deployment of RE

technologies.

12

Summary for Policymakers Summaries

Climate change will have impacts on the size and geographic distribution of the technical potential for RE

sources, but research into the magnitude of these possible effects is nascent. Because RE sources are, in many

cases, dependent on the climate, global climate change will affect the RE resource base, though the precise nature and

magnitude of these impacts is uncertain. The future technical potential for bioenergy could be infl uenced by climate

change through impacts on biomass production such as altered soil conditions, precipitation, crop productivity and

other factors. The overall impact of a global mean temperature change of less than 2°C on the technical potential

of bioenergy is expected to be relatively small on a global basis. However, considerable regional differences could

be expected and uncertainties are larger and more diffi cult to assess compared to other RE options due to the large

number of feedback mechanisms involved. [2.2, 2.6] For solar energy, though climate change is expected to infl uence

the distribution and variability of cloud cover, the impact of these changes on overall technical potential is expected

to be small [3.2]. For hydropower the overall impacts on the global technical potential is expected to be slightly posi-

tive. However, results also indicate the possibility of substantial variations across regions and even within countries.

[5.2] Research to date suggests that climate change is not expected to greatly impact the global technical potential for

wind energy development but changes in the regional distribution of the wind energy resource may be expected [7.2].

Climate change is not anticipated to have signifi cant impacts on the size or geographic distribution of geothermal or

ocean energy resources. [4.2, 6.2]

Figure SPM.4 | Ranges of global technical potentials of RE sources derived from studies presented in Chapters 2 through 7. Biomass and solar are shown as primary energy due to

their multiple uses; note that the fi gure is presented in logarithmic scale due to the wide range of assessed data. [Figure 1.17, 1.2.3]

Notes: Technical potentials reported here represent total worldwide potentials for annual RE supply and do not deduct any potential that is already being utilized. Note that RE elec-

tricity sources could also be used for heating applications, whereas biomass and solar resources are reported only in primary energy terms but could be used to meet various energy

service needs. Ranges are based on various methods and apply to different future years; consequently, the resulting ranges are not strictly comparable across technologies. For the

data behind Figure SPM.4 and additional notes that apply, see Chapter 1 Annex, Table A.1.1 (as well as the underlying chapters).

Global Electricity

Demand, 2008: 61 EJ

Global Primary Energy

Supply, 2008: 492 EJ

Global Heat

Demand, 2008: 164 EJ

0

10

100

1,000

10,000

100,000

Global Technical Potential [EJ/yr, log scale]

Direct Solar

Energy

BiomassGeothermal

Energy

Wind

Energy

Ocean

Energy

Primary EnergyHeatElectricity

HydropowerGeothermal

Energy

49837

1575

500

50

312

10

580

85

331

7

52

50

1109

118

Max (in EJ/yr)

Min (in EJ/yr)

Range of Estimates of Global Technical Potentials

Range of Estimates

Summarized in Chapters 2-7

Maximum

Minimum

13

Summaries Summary for Policymakers

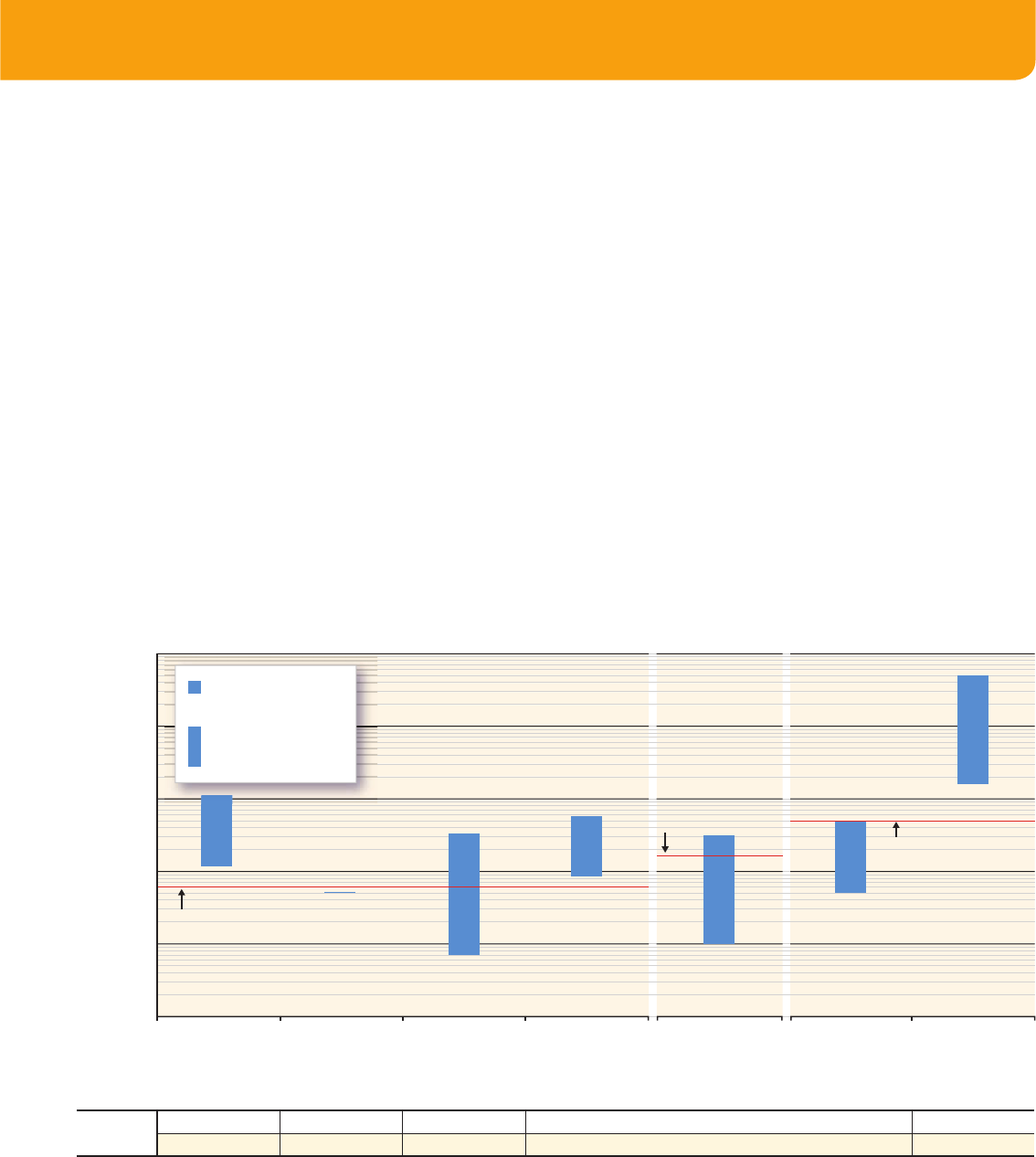

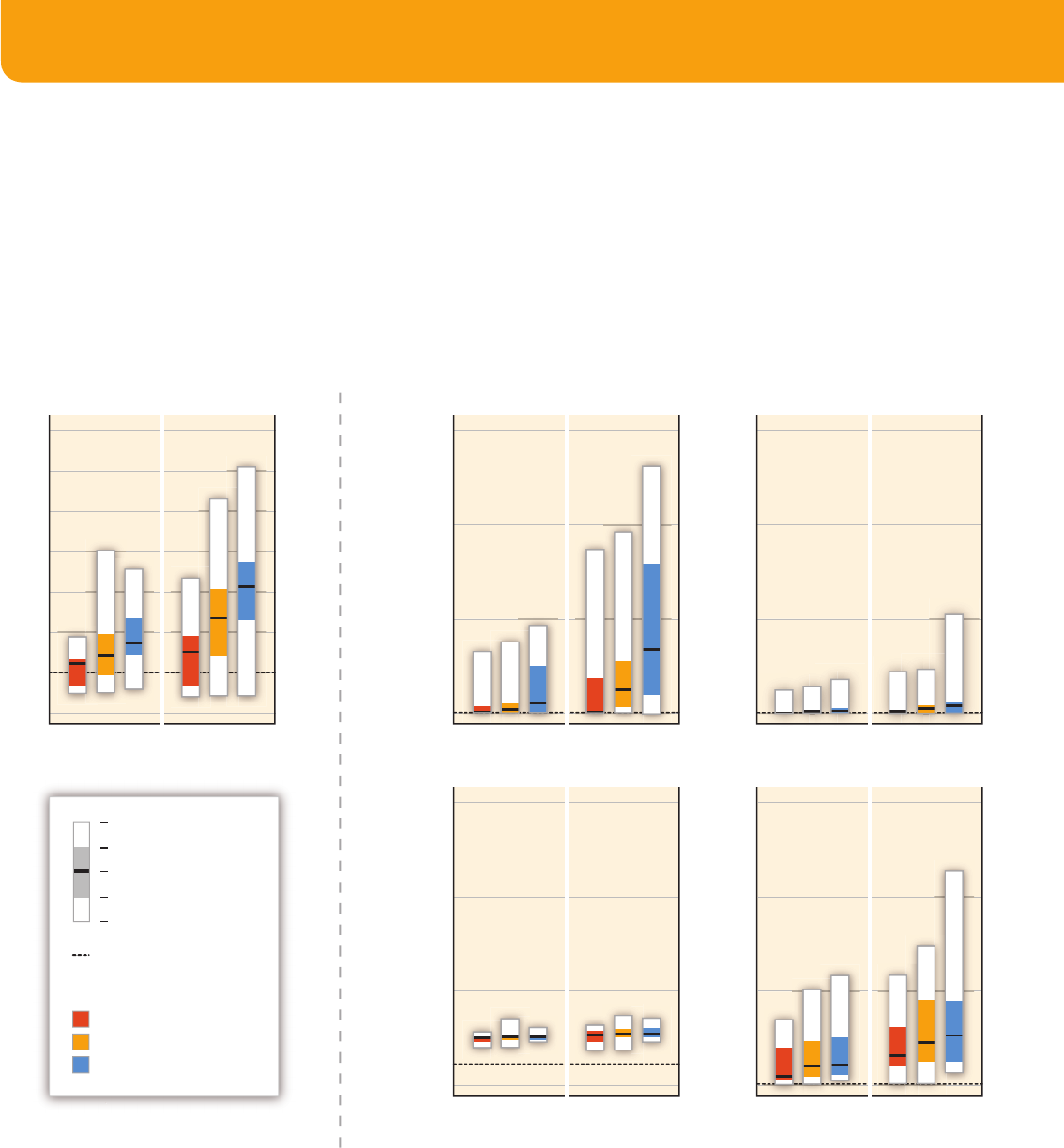

The levelized cost of energy

8

for many RE technologies is currently higher than existing energy prices,

though in various settings RE is already economically competitive. Ranges of recent levelized costs of energy for

selected commercially available RE technologies are wide, depending on a number of factors including, but not limited

to, technology characteristics, regional variations in cost and performance, and differing discount rates (Figure SPM.5).

[1.3.2, 2.3, 2.7, 3.8, 4.8, 5.8, 6.7, 7.8, 10.5, Annex III] Some RE technologies are broadly competitive with existing

market energy prices. Many of the other RE technologies can provide competitive energy services in certain circum-

stances, for example, in regions with favourable resource conditions or that lack the infrastructure for other low-cost

energy supplies. In most regions of the world, policy measures are still required to ensure rapid deployment of many RE

sources. [2.3, 2.7, 3.8, 4.7, 5.8, 6.7, 7.8, 10.5]

Monetizing the external costs of energy supply would improve the relative competitiveness of RE. The same applies if

market prices increase due to other reasons (Figure SPM.5). [10.6] The levelized cost of energy for a technology is not

the sole determinant of its value or economic competitiveness. The attractiveness of a specifi c energy supply option

depends also on broader economic as well as environmental and social aspects, and the contribution that the technol-

ogy provides to meeting specifi c energy services (e.g., peak electricity demands) or imposes in the form of ancillary

costs on the energy system (e.g., the costs of integration). [8.2, 9.3, 10.6]

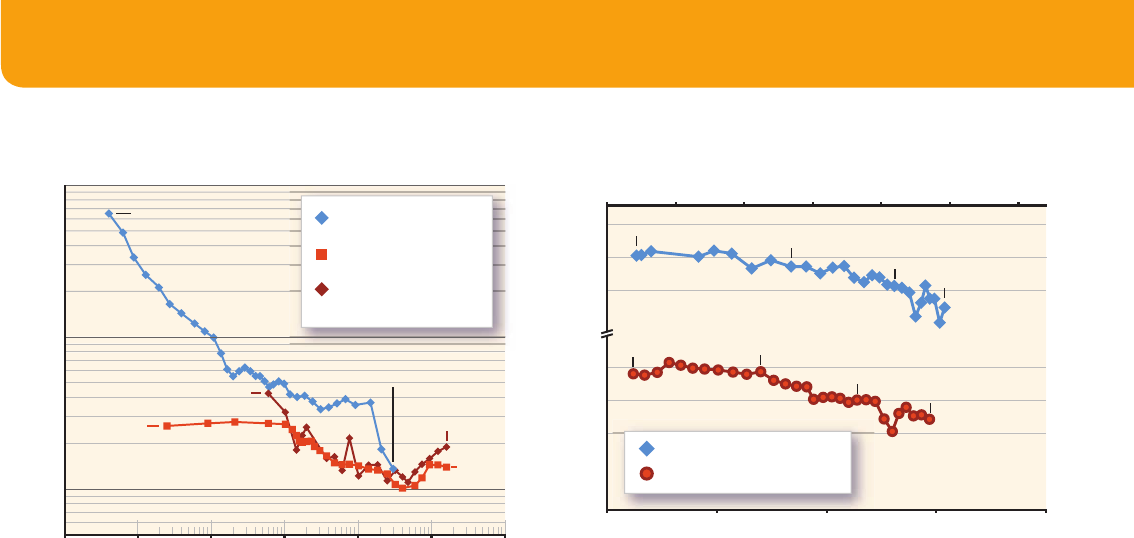

The cost of most RE technologies has declined and additional expected technical advances would result

in further cost reductions. Signifi cant advances in RE technologies and associated long-term cost reductions have

been demonstrated over the last decades, though periods of rising prices have sometimes been experienced (due

to, for example, increasing demand for RE in excess of available supply) (Figure SPM.6). The contribution of differ-

ent drivers (e.g., R&D, economies of scale, deployment-oriented learning, and increased market competition among

RE suppliers) is not always understood in detail. [2.7, 3.8, 7.8, 10.5] Further cost reductions are expected, resulting in

greater potential deployment and consequent climate change mitigation. Examples of important areas of potential

technological advancement include: new and improved feedstock production and supply systems, biofuels produced

via new processes (also called next-generation or advanced biofuels, e.g., lignocellulosic) and advanced biorefi ning

[2.6]; advanced PV and CSP technologies and manufacturing processes [3.7]; enhanced geothermal systems (EGS) [4.6];

multiple emerging ocean technologies [6.6]; and foundation and turbine designs for offshore wind energy [7.7]. Further

cost reductions for hydropower are expected to be less signifi cant than some of the other RE technologies, but R&D

opportunities exist to make hydropower projects technically feasible in a wider range of locations and to improve the

technical performance of new and existing projects. [5.3, 5.7, 5.8]

A variety of technology-specifi c challenges (in addition to cost) may need to be addressed to enable RE

to signifi cantly upscale its contribution to reducing GHG emissions. For the increased and sustainable use of

bioenergy, proper design, implementation and monitoring of sustainability frameworks can minimize negative impacts

and maximize benefi ts with regard to social, economic and environmental issues [SPM.5, 2.2, 2.5, 2.8]. For solar energy,

regulatory and institutional barriers can impede deployment, as can integration and transmission issues [3.9]. For geo-

thermal energy, an important challenge would be to prove that enhanced geothermal systems (EGS) can be deployed

economically, sustainably and widely [4.5, 4.6, 4.7, 4.8]. New hydropower projects can have ecological and social

impacts that are very site specifi c, and increased deployment may require improved sustainability assessment tools, and

regional and multi-party collaborations to address energy and water needs [5.6, 5.9, 5.10]. The deployment of ocean

energy could benefi t from testing centres for demonstration projects, and from dedicated policies and regulations that

encourage early deployment [6.4]. For wind energy, technical and institutional solutions to transmission constraints and

operational integration concerns may be especially important, as might public acceptance issues relating primarily to

landscape impacts. [7.5, 7.6, 7.9]

8 The levelized cost of energy represents the cost of an energy generating system over its lifetime; it is calculated as the per-unit price at which

energy must be generated from a specifi c source over its lifetime to break even. It usually includes all private costs that accrue upstream in the

value chain, but does not include the downstream cost of delivery to the fi nal customer; the cost of integration, or external environmental or

other costs. Subsidies and tax credits are also not included.

14

Summary for Policymakers Summaries

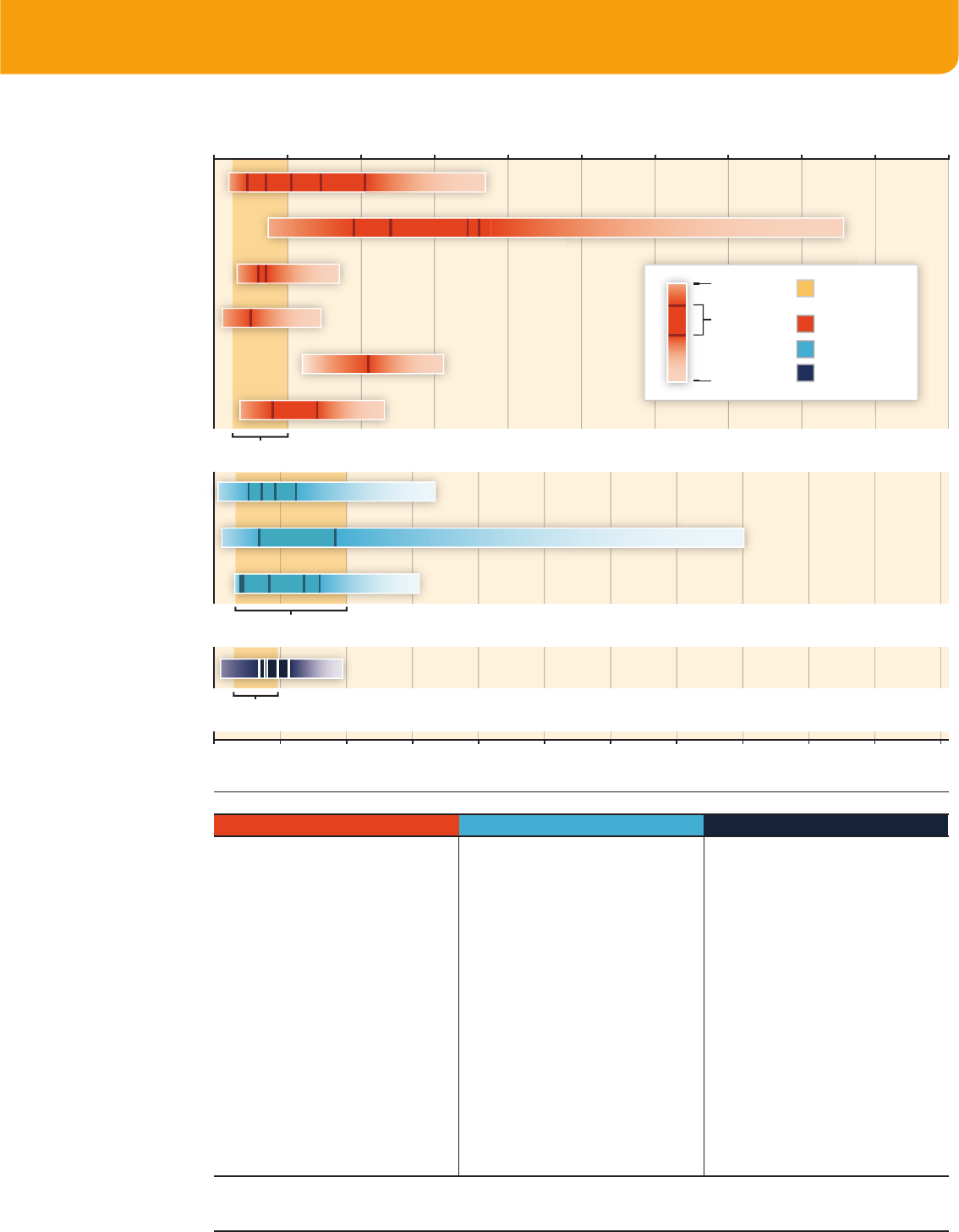

Figure SPM.5 | Range in recent levelized cost of energy for selected commercially available RE technologies in comparison to recent non-renewable energy costs. Technology sub-

categories and discount rates were aggregated for this fi gure. For related fi gures with less or no such aggregation, see [1.3.2, 10.5, Annex III].

Range of Oil and Gas

Based Heating Cost

Range of Non-Renewable

Electricity Cost

Range of Gasoline

and Diesel Cost

[UScent

2005

/kWh]

0 10 20 30 40 50 60 70 80 90 100

[USD

2005

/GJ]

Biofuels

Geothermal Heat

Solar Thermal Heat

Biomass Heat

Wind Electricity

Ocean Electricity

Hydropower

Geothermal Electricity

Solar Electricity

Biomass Electricity

2752502252001751501251007550025

Non-Renewables

Heat

Transport Fuels

Electricity

Lower Bound

Upper Bound

Medium Values

Biofuels:

1. Corn ethanol

2. Soy biodiesel

3. Wheat ethanol

4. Sugarcane ethanol

5. Palm oil biodiese

l

Biomass Heat:

1. Municipal solid waste based CHP

2. Anaerobic digestion based CHP

3. Steam turbine CHP

4. Domestic pellet heating system

Solar Thermal Heat:

1. Domestic hot water systems in China

2. Water and space heating

Geothermal Heat:

1. Greenhouses

2. Uncovered aquaculture ponds

3. District heating

4. Geothermal heat pumps

5. Geothermal building heating

Biomass:

1. Cofiring

2. Small scale combined heat and power, CHP

(Gasification internal combustion engine)

3. Direct dedicated stoker & CHP

4. Small scale CHP (steam turbine)

5. Small scale CHP (organic Rankine cycle)

Solar Electricity:

1. Concentrating solar power

2. Utility-scale PV (1-axis and fixed tilt)

3. Commercial rooftop PV

4. Residential rooftop PV

Geothermal Electricity:

1. Condensing flash plant

2. Binary cycle plant

Hydropower:

1. All types

Ocean Electricity:

1. Tidal barrage

Wind Electricity:

1. Onshore

2. Offshore

Transport FuelsHeatElectricity

Notes: Medium values are shown for the following subcategories, sorted in the order as they appear in the respective ranges (from left to right):

The lower range of the levelized cost of energy for each RE technology is based on a combination of the most favourable input-values, whereas the upper range is based on a

combination of the least favourable input values. Reference ranges in the figure background for non-renewable electricity options are indicative of the levelized cost of centralized

non-renewable electricity generation. Reference ranges for heat are indicative of recent costs for oil and gas based heat supply options. Reference ranges for transport fuels are

based on recent crude oil spot prices of USD 40 to 130/barrel and corresponding diesel and gasoline costs, excluding taxes.

15

Summaries Summary for Policymakers

Figure SPM.6 | Selected experience curves in logarithmic scale for (a) the price of silicon PV modules and onshore wind power plants per unit of capacity; and (b) the cost of

sugarcane-based ethanol production [data from Figure 3.17, 3.8.3, Figure 7.20, 7.8.2, Figure 2.21, 2.7.2].

Notes: Depending on the setting, cost reductions may occur at various geographic scales. The country-level examples provided here derive from the published literature. No global

dataset of wind power plant prices or costs is readily available. Reductions in the cost or price of a technology per unit of capacity understate reductions in the levelized cost of energy

of that technology when performance improvements occur. [7.8.4, 10.5]

Onshore Wind Power Plants

(Denmark)

Onshore Wind Power Plants

(USA)

Produced Silicon PV Modules

(Global)

1

Cumulative Global Capacity [MW]

1

10

100

10 100 1,000 10,000 1,000,000 100,000

Average Price [USD

2005

/W]

1976

[65 USD/W]

2010

[1.4 USD/W]

(a)

0,5

50

5

1981

[2.6 USD/W]

1984

[4.3 USD/W]

2009

[1.4 USD/W]

2009

[1.9 USD/W]

Sugarcane

Ethanol Prod. Cost (excl. Feedstock)

Cumulative Sugarcane Production in Brazil [10

6

Tonnes of Sugarcane]

1,000 2,000 4,000 8,000 16,000

Average Production Cost of Ethanol [USD

2005

/m

3

]

and Sugarcane [USD

2005

/t]

10

20

40

200

400

800

10 20 40 80 160 320 640

Cumulative Ethanol Production in Brazil [10

6

m

3

]

2004

1975

1985

1995

2004

1975

1985

1995

(b)

4. Integration into present and future energy systems

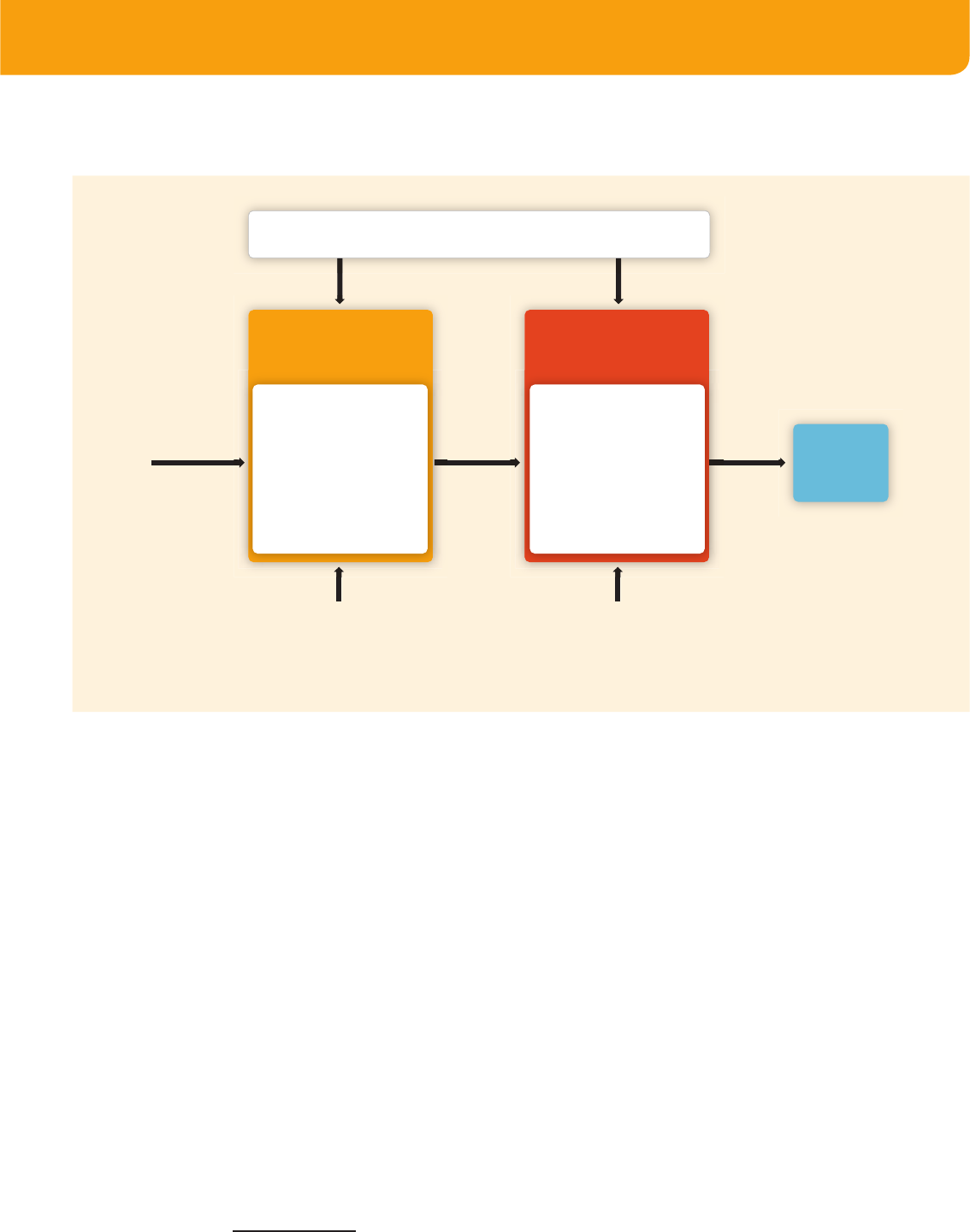

Various RE resources are already being successfully integrated into energy supply systems [8.2] and into

end-use sectors [8.3] (Figure SPM.7).

The characteristics of different RE sources can infl uence the scale of the integration challenge. Some RE

resources are widely distributed geographically. Others, such as large-scale hydropower, can be more centralized but

have integration options constrained by geographic location. Some RE resources are variable with limited predictability.

Some have lower physical energy densities and different technical specifi cations from fossil fuels. Such characteristics

can constrain ease of integration and invoke additional system costs particularly when reaching higher shares of RE.

[8.2]

Integrating RE into most existing energy supply systems and end-use sectors at an accelerated rate—

leading to higher shares of RE—is technologically feasible, though will result in a number of additional

challenges. Increased shares of RE are expected within an overall portfolio of low GHG emission technologies [10.3,

Tables 10.4-10.6]. Whether for electricity, heating, cooling, gaseous fuels or liquid fuels, including integration directly

into end-use sectors, the RE integration challenges are contextual and site specifi c and include the adjustment of exist-

ing energy supply systems. [8.2, 8.3]

The costs and challenges of integrating increasing shares of RE into an existing energy supply system

depend on the current share of RE, the availability and characteristics of RE resources, the system character-

istics, and how the system evolves and develops in the future.

• RE can be integrated into all types of electricity systems, from large inter-connected continental-scale grids [8.2.1]

down to small stand-alone systems and individual buildings [8.2.5]. Relevant system characteristics include the

generation mix and its fl exibility, network infrastructure, energy market designs and institutional rules, demand

location, demand profi les, and control and communication capability. Wind, solar PV energy and CSP without

16

Summary for Policymakers Summaries

storage can be more diffi cult to integrate than dispatchable

9

hydropower, bioenergy, CSP with storage and geother-

mal energy.

As the penetration of variable RE sources increases, maintaining system reliability may become more challenging

and costly. Having a portfolio of complementary RE technologies is one solution to reduce the risks and costs of RE

integration. Other solutions include the development of complementary fl exible generation and the more fl exible

operation of existing schemes; improved short-term forecasting, system operation and planning tools; electricity

demand that can respond in relation to supply availability; energy storage technologies (including storage-based

hydropower); and modifi ed institutional arrangements. Electricity network transmission (including interconnections

between systems) and/or distribution infrastructure may need to be strengthened and extended, partly because of

the geographical distribution and fi xed remote locations of many RE resources. [8.2.1]

• District heating systems can use low-temperature thermal RE inputs such as solar and geothermal heat, or biomass,

including sources with few competing uses such as refuse-derived fuels. District cooling can make use of cold natu-

ral waterways. Thermal storage capability and fl exible cogeneration can overcome supply and demand variability

challenges as well as provide demand response for electricity systems. [8.2.2]

9 Electricity plants that can schedule power generation as and when required are classed as dispatchable [8.2.1.1, Annex I]. Variable RE

technologies are partially dispatchable (i.e., only when the RE resource is available). CSP plants are classifi ed as dispatchable when heat is

stored for use at night or during periods of low sunshine.

Figure SPM.7 | Pathways for RE integration to provide energy services, either into energy supply systems or on-site for use by the end-use sectors. [Figure 8.1, 8.1]

Fossil Fuels

and Nuclear

Energy Efficiency

Measures

Energy Efficiency

and Demand

Response Measures

Renewable Energy Resources

End-Use Sectors

(Section 8.3)

Energy Supply

Systems

(Section 8.2)

Electricity Generation and

Distribution

Heating and Cooling Networks

Gas Grids

Liquid Fuels Distribution

Autonomous Systems

Transport and Vehicles

Buildings and Households

Industry

Agriculture, Forests and

Fisheries

Energy

Carriers

Energy

Services

Energy

Consumers

17

Summaries Summary for Policymakers

• In gas distribution grids, injecting biomethane, or in the future, RE-derived hydrogen and synthetic natural gas, can

be achieved for a range of applications but successful integration requires that appropriate gas quality standards

are met and pipelines upgraded where necessary. [8.2.3]

• Liquid fuel systems can integrate biofuels for transport applications or for cooking and heating applications. Pure

(100%) biofuels, or more usually those blended with petroleum-based fuels, usually need to meet technical stan-

dards consistent with vehicle engine fuel specifi cations. [8.2.4, 8.3.1]

There are multiple pathways for increasing the shares of RE across all end-use sectors. The ease of integra-

tion varies depending on region, characteristics specifi c to the sector and the technology.

• For transport, liquid and gaseous biofuels are already and are expected to continue to be integrated into the fuel

supply systems of a growing number of countries. Integration options may include decentralized on-site or central-

ized production of RE hydrogen for fuel cell vehicles and RE electricity for rail and electric vehicles [8.2.1, 8.2.3]

depending on infrastructure and vehicle technology developments. [8.3.1] Future demand for electric vehicles could

also enhance fl exible electricity generation systems. [8.2.1, 8.3.1]

• In the building sector, RE technologies can be integrated into both new and existing structures to produce electric-

ity, heating and cooling. Supply of surplus energy may be possible, particularly for energy effi cient building designs.

[8.3.2] In developing countries, the integration of RE supply systems is feasible for even modest dwellings. [8.3.2,

9.3.2]

• Agriculture as well as food and fi bre process industries often use biomass to meet direct heat and power demands

on-site. They can also be net exporters of surplus fuels, heat, and electricity to adjacent supply systems. [8.3.3,

8.3.4] Increasing the integration of RE for use by industries is an option in several sub-sectors, for example through

electro-thermal technologies or, in the longer term, by using RE hydrogen. [8.3.3]

The costs associated with RE integration, whether for electricity, heating, cooling, gaseous or liquid fuels,

are contextual, site-specifi c and generally diffi cult to determine. They may include additional costs for network

infrastructure investment, system operation and losses, and other adjustments to the existing energy supply systems as

needed. The available literature on integration costs is sparse and estimates are often lacking or vary widely.

In order to accommodate high RE shares, energy systems will need to evolve and be adapted. [8.2, 8.3]

Long-term integration efforts could include investment in enabling infrastructure; modifi cation of institutional and

governance frameworks; attention to social aspects, markets and planning; and capacity building in anticipation of

RE growth. [8.2, 8.3] Furthermore, integration of less mature technologies, including biofuels produced through new

processes (also called advanced biofuels or next-generation biofuels), fuels generated from solar energy, solar cooling,

ocean energy technologies, fuel cells and electric vehicles, will require continuing investments in research, development

and demonstration (RD&D), capacity building and other supporting measures. [2.6, 3.7, 11.5, 11.6, 11.7]

RE could shape future energy supply and end-use systems, in particular for electricity, which is expected to attain higher

shares of RE earlier than either the heat or transport fuel sectors at the global level [10.3]. Parallel developments in

electric vehicles [8.3.1], increased heating and cooling using electricity (including heat pumps) [8.2.2, 8.3.2, 8.3.3], fl ex-

ible demand response services (including the use of smart meters) [8.2.1], energy storage and other technologies could

be associated with this trend.

As infrastructure and energy systems develop, in spite of the complexities, there are few, if any, funda-

mental technological limits to integrating a portfolio of RE technologies to meet a majority share of total

18

Summary for Policymakers Summaries

energy demand in locations where suitable RE resources exist or can be supplied. However, the actual rate

of integration and the resulting shares of RE will be infl uenced by factors such as costs, policies, environ-

mental issues and social aspects. [8.2, 8.3, 9.3, 9.4, 10.2, 10.5]

5. Renewable energy and sustainable development

Historically, economic development has been strongly correlated with increasing energy use and growth of

GHG emissions, and RE can help decouple that correlation, contributing to sustainable development (SD).

Though the exact contribution of RE to SD has to be evaluated in a country-specifi c context, RE offers the opportunity

to contribute to social and economic development, energy access, secure energy supply, climate change mitigation, and

the reduction of negative environmental and health impacts. [9.2] Providing access to modern energy services would

support the achievement of the Millennium Development Goals. [9.2.2, 9.3.2]

• RE can contribute to social and economic development. Under favorable conditions, cost savings in compari-

son to non-RE use exist, in particular in remote and in poor rural areas lacking centralized energy access. [9.3.1,

9.3.2.] Costs associated with energy imports can often be reduced through the deployment of domestic RE tech-

nologies that are already competitive. [9.3.3] RE can have a positive impact on job creation although the studies

available differ with respect to the magnitude of net employment. [9.3.1]

• RE can help accelerate access to energy, particularly for the 1.4 billion people without access to electric-

ity and the additional 1.3 billion using traditional biomass. Basic levels of access to modern energy services

can provide signifi cant benefi ts to a community or household. In many developing countries, decentralized grids

based on RE and the inclusion of RE in centralized energy grids have expanded and improved energy access. In

addition, non-electrical RE technologies also offer opportunities for modernization of energy services, for example,

using solar energy for water heating and crop drying, biofuels for transportation, biogas and modern biomass for

heating, cooling, cooking and lighting, and wind for water pumping. [9.3.2, 8.1] The number of people without

access to modern energy services is expected to remain unchanged unless relevant domestic policies are imple-

mented, which may be supported or complemented by international assistance as appropriate. [9.3.2, 9.4.2]

• RE options can contribute to a more secure energy supply, although specifi c challenges for integra-

tion must be considered. RE deployment might reduce vulnerability to supply disruption and market volatility if

competition is increased and energy sources are diversifi ed. [9.3.3, 9.4.3] Scenario studies indicate that concerns

regarding secure energy supply could continue in the future without technological improvements within the

transport sector. [2.8, 9.4.1.1, 9.4.3.1, 10.3] The variable output profi les of some RE technologies often necessitate

technical and institutional measures appropriate to local conditions to assure energy supply reliability. [8.2, 9.3.3]

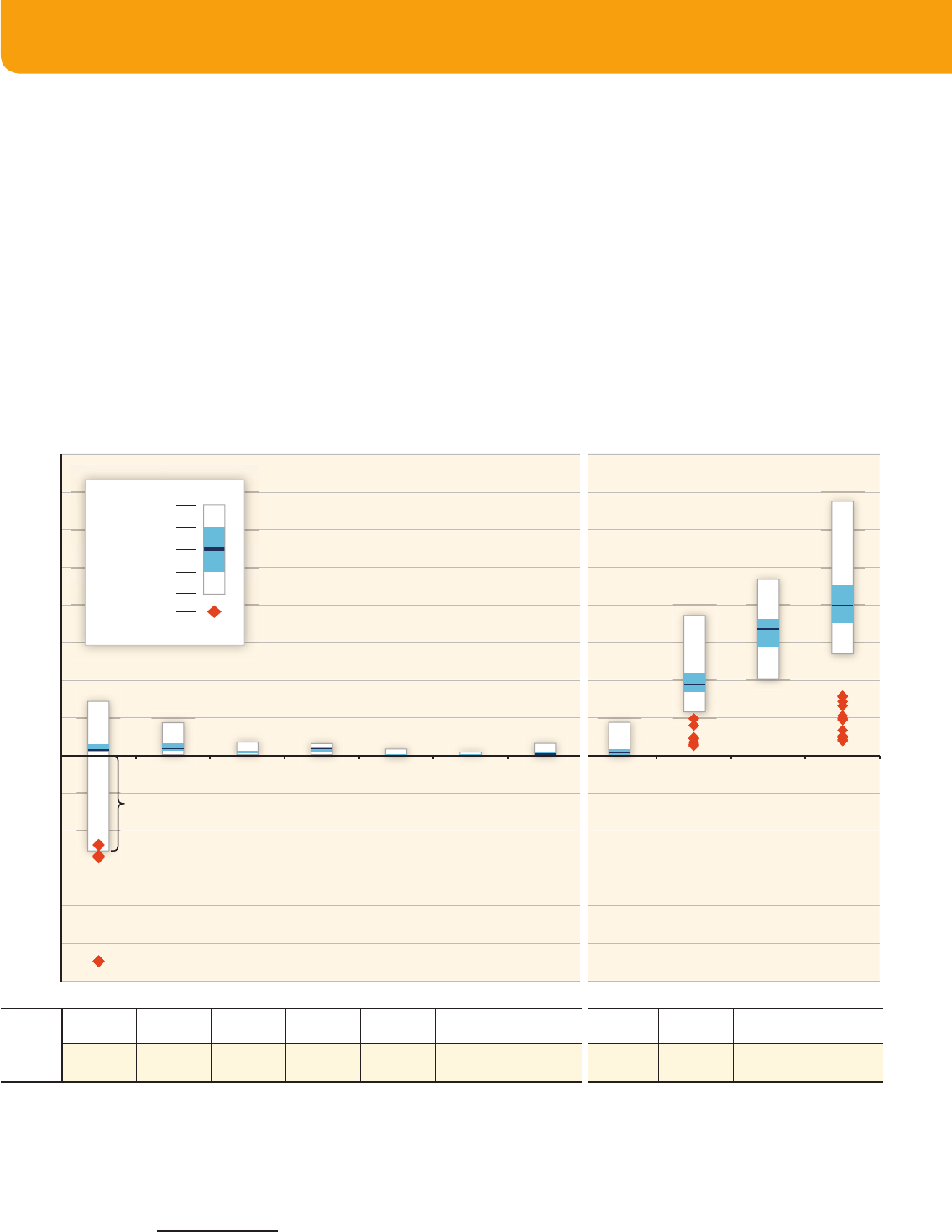

• In addition to reduced GHG emissions, RE technologies can provide other important environmental

benefi ts. Maximizing these benefi ts depends on the specifi c technology, management, and site charac-

teristics associated with each RE project.

• Lifecycle assessments (LCA) for electricity generation indicate that GHG emissions from RE technolo-

gies are, in general, signifi cantly lower than those associated with fossil fuel options, and in a range

of conditions, less than fossil fuels employing CCS. The median values for all RE range from 4 to 46 g

CO

2

eq/kWh while those for fossil fuels range from 469 to 1,001 g CO

2

eq/kWh (excluding land use change emis-

sions) (Figure SPM.8).

• Most current bioenergy systems, including liquid biofuels, result in GHG emission reductions, and

most biofuels produced through new processes (also called advanced biofuels or next-generation

biofuels) could provide higher GHG mitigation. The GHG balance may be affected by land use

19

Summaries Summary for Policymakers

changes and corresponding emissions and removals. Bioenergy can lead to avoided GHG emissions from

residues and wastes in landfi ll disposals and co-products; the combination of bioenergy with CCS may provide

for further reductions (see Figure SPM.8). The GHG implications related to land management and land use

changes in carbon stocks have considerable uncertainties. [2.2, 2.5, 9.3.4.1]

• The sustainability of bioenergy, in particular in terms of lifecycle GHG emissions, is infl uenced by

land and biomass resource management practices. Changes in land and forest use or management that,

according to a considerable number of studies, could be brought about directly or indirectly by biomass produc-

tion for use as fuels, power or heat, can decrease or increase terrestrial carbon stocks. The same studies also

Figure SPM.8 | Estimates of lifecycle GHG emissions (g CO

2

eq/kWh) for broad categories of electricity generation technologies, plus some technologies integrated with CCS. Land use-

related net changes in carbon stocks (mainly applicable to biopower and hydropower from reservoirs) and land management impacts are excluded; negative estimates

10

for biopower

are based on assumptions about avoided emissions from residues and wastes in landfi ll disposals and co-products. References and methods for the review are reported in Annex II. The

number of estimates is greater than the number of references because many studies considered multiple scenarios. Numbers reported in parentheses pertain to additional references

and estimates that evaluated technologies with CCS. Distributional information relates to estimates currently available in LCA literature, not necessarily to underlying theoretical or

practical extrema, or the true central tendency when considering all deployment conditions. [Figure 9.8, 9.3.4.1]

10 ‘Negative estimates’ within the terminology of lifecycle assessments presented in the SRREN refer to avoided emissions. Unlike the case of bioen-

ergy combined with CCS, avoided emissions do not remove GHGs from the atmosphere.

Maximum

75

th

Percentile

Median

25

th

Percentile

Minimum

Single Estimates

with CCS

Electricity Generation Technologies Powered by Renewable Resources

Biopower

Photovoltaics

Concentrating Solar Power

Coal

Oil

Natural Gas

Geothermal Energy

Hydropower

Nuclear Energy

Ocean Energy

Wind Energy

-1,250

-1,500

-1,000

750

250

-250

-750

-500

0

500

1,750

1,250

1,000

1,500

2,000

Lifecycle Greenhouse Gas Emissions [g CO

2

eq / kWh]

Electricity Generation Technologies

Powered by Non-Renewable Resources

Avoided Emissions, no Removal of GHGs from the Atmosphere

*

*

169(+12)

50(+10)

24

10

83(+7)

36(+4)

125

32

126

49

10

5

28

11

8

6

42

13

124

26

222(+4)

52(+0)

Count of

Estimates

Count of

References

20

Summary for Policymakers Summaries

show that indirect changes in terrestrial carbon stocks have considerable uncertainties, are not directly observa-

ble, are complex to model and are diffi cult to attribute to a single cause. Proper governance of land use, zoning,

and choice of biomass production systems are key considerations for policy makers. [2.4.5, 2.5.1, 9.3.4, 9.4.4]

Policies are in place that aim to ensure that the benefi ts from bioenergy, such as rural development, overall

improvement of agricultural management and the contribution to climate change mitigation, are realized; their

effectiveness has not been assessed. [2.2, 2.5, 2.8]

• RE technologies, in particular non-combustion based options, can offer benefi ts with respect to air

pollution and related health concerns. [9.3.4.3, 9.4.4.1] Improving traditional biomass use can signifi cantly

reduce local and indoor air pollution (alongside GHG emissions, deforestation and forest degradation) and

lower associated health impacts, particularly for women and children in developing countries. [2.5.4, 9.3.4.4]

• Water availability could infl uence choice of RE technology. Conventional water-cooled thermal power

plants may be especially vulnerable to conditions of water scarcity and climate change. In areas where water

scarcity is already a concern, non-thermal RE technologies or thermal RE technologies using dry cooling can pro-

vide energy services without additional stress on water resources. Hydropower and some bioenergy systems are

dependent on water availability, and can either increase competition or mitigate water scarcity. Many impacts

can be mitigated by siting considerations and integrated planning. [2.5.5.1, 5.10, 9.3.4.4]

• Site-specifi c conditions will determine the degree to which RE technologies impact biodiversity.

RE-specifi c impacts on biodiversity may be positive or negative. [2.5, 3.6, 4.5, 5.6, 6.5, , 9.3.4.6]

• RE technologies have low fatality rates. Accident risks of RE technologies are not negligible, but their often

decentralized structure strongly limits the potential for disastrous consequences in terms of fatalities. However,

dams associated with some hydropower projects may create a specifi c risk depending on site-specifi c factors.

[9.3.4.7]

6. Mitigation potentials and costs

A signifi cant increase in the deployment of RE by 2030, 2050 and beyond is indicated in the majority of

the 164 scenarios reviewed in this Special Report.

11

In 2008, total RE production was roughly 64 EJ/yr (12.9% of

total primary energy supply) with more than 30 EJ/yr of this being traditional biomass. More than 50% of the scenarios

project levels of RE deployment in 2050 of more than 173 EJ/yr reaching up to over 400 EJ/yr in some cases (Figure

SPM.9). Given that traditional biomass use decreases in most scenarios, a corresponding increase in the production

level of RE (excluding traditional biomass) anywhere from roughly three-fold to more than ten-fold is projected. The

global primary energy supply share of RE differs substantially among the scenarios. More than half of the scenarios

show a contribution from RE in excess of a 17% share of primary energy supply in 2030 rising to more than 27% in

2050. The scenarios with the highest RE shares reach approximately 43% in 2030 and 77% in 2050. [10.2, 10.3]

RE can be expected to expand even under baseline scenarios. Most baseline scenarios show RE deployments

signifi cantly above the 2008 level of 64 EJ/yr and up to 120 EJ/yr by 2030. By 2050, many baseline scenarios reach

RE deployment levels of more than 100 EJ/yr and in some cases up to about 250 EJ/yr (Figure SPM.9). These baseline

deployment levels result from a range of assumptions, including, for example, continued demand growth for energy

services throughout the century, the ability of RE to contribute to increased energy access and the limited long-term

11 For this purpose a review of 164 global scenarios from 16 different large-scale integrated models was conducted. Although the set of scenarios

allows for a meaningful assessment of uncertainty, the reviewed 164 scenarios do not represent a fully random sample suitable for rigorous

statistical analysis and do not represent always the full RE portfolio (e.g., so far ocean energy is only considered in a few scenarios) [10.2.2]. For

more specifi c analysis, a subset of 4 illustrative scenarios from the set of 164 was used. They represent a span from a baseline scenario without

specifi c mitigation targets to three scenarios representing different CO

2

stabilization levels. [10.3]

21

Summaries Summary for Policymakers

availability of fossil resources. Other assumptions (e.g., improved costs and performance of RE technologies) render RE

technologies increasingly economically competitive in many applications even in the absence of climate policy. [10.2]

RE deployment signifi cantly increases in scenarios with low GHG stabilization concentrations. Low GHG stabi-

lization scenarios lead on average to higher RE deployment compared to the baseline. However, for any given long-term

GHG concentration goal, the scenarios exhibit a wide range of RE deployment levels (Figure SPM.9). In scenarios that

stabilize the atmospheric CO

2

concentrations at a level of less than 440 ppm, the median RE deployment level in 2050

is 248 EJ/yr (139 in 2030), with the highest levels reaching 428 EJ/yr by 2050 (252 in 2030). [10.2]

Many combinations of low-carbon energy supply options and energy effi ciency improvements can con-

tribute to given low GHG concentration levels, with RE becoming the dominant low-carbon energy supply

option by 2050 in the majority of scenarios. This wide range of results originates in assumptions about factors such

as developments in RE technologies (including bioenergy with CCS) and their associated resource bases and costs; the

comparative attractiveness of other mitigation options (e.g., end-use energy effi ciency, nuclear energy, fossil energy

with CCS); patterns of consumption and production; fundamental drivers of energy services demand (including future

population and economic growth); the ability to integrate variable RE sources into power grids; fossil fuel resources;

specifi c policy approaches to mitigation; and emissions trajectories towards long-term concentration levels. [10.2]

Figure SPM.9 | Global RE primary energy supply (direct equivalent) from 164 long-term scenarios versus fossil and industrial CO

2

emissions in 2030 and 2050. Colour coding is based

on categories of atmospheric CO

2

concentration stabilization levels that are defi ned consistently with those in the AR4. The panels to the right of the scatterplots show the deployment

levels of RE in each of the atmospheric CO

2

concentration categories. The thick black line corresponds to the median, the coloured box corresponds to the inter-quartile range (25th to

75th percentile) and the ends of the white surrounding bars correspond to the total range across all reviewed scenarios. The grey crossed lines show the relationship in 2007. [Figure

10.2, 10.2.2.2]

Notes: For data reporting reasons only 161 scenarios are included in the 2030 results shown here, as opposed to the full set of 164 scenarios. RE deployment levels below those of

today are a result of model output and differences in the reporting of traditional biomass. For details on the use of the ‘direct equivalent’ method of accounting for primary energy

supply and the implied care needed in the interpretation of scenario results, see Box SPM.2. Note that categories V and above are not included and category IV is extended to 600

ppm from 570 ppm, because all stabilization scenarios lie below 600 ppm CO

2

in 2100 and because the lowest baseline scenarios reach concentration levels of slightly more than

600 ppm by 2100.

CO

2

Concentration Levels

Category I (<400 ppm)

Category II (400-440 ppm)

Category III (440-485 ppm)

Category IV (485-600 ppm)

Baselines

20 40 60 80020 40 600

2030

0 100 200 300

400

0 100 200 300

400

N=161

2050

N=164

Renewable Primary Energy Supply [EJ/yr]

CO

2

Emissions from Fossil Fuels

and Industrial Processes [Gt CO

2

/yr]

CO

2

Emissions from Fossil Fuels

and Industrial Processes [Gt CO

2

/yr]

Category I

Category II

Category III

Category IV

Baselines

Category I

Category II

Category III

Category IV

Baselines

Maximum

75th

Median

25th

Minimum

22

Summary for Policymakers Summaries

The scenario review in this Special Report indicates that RE has a large potential to mitigate GHG emis-

sions. Four illustrative scenarios span a range of global cumulative CO

2

savings between 2010 and 2050, from about

220 to 560 Gt CO

2

compared to about 1,530Gt cumulative fossil and industrial CO

2

emissions in the IEA World Energy

Outlook 2009 Reference Scenario during the same period. The precise attribution of mitigation potentials to RE depends

on the role scenarios attribute to specifi c mitigation technologies, on complex system behaviours and, in particular, on

the energy sources that RE displaces. Therefore, attribution of precise mitigation potentials to RE should be viewed with

appropriate caution. [10.2, 10.3, 10.4]

Scenarios generally indicate that growth in RE will be widespread around the world. Although the precise

distribution of RE deployment among regions varies substantially across scenarios, the scenarios are largely consistent

in indicating widespread growth in RE deployment around the globe. In addition, the total RE deployment is higher over

the long term in the group of non-Annex I countries

12

than in the group of Annex I countries in most scenarios (Figure

SPM.10). [10.2, 10.3]

12 The terms ‘Annex I’ and ‘non-Annex I’ are categories of countries that derive from the United Nations Framework Convention on Climate

Change (UNFCCC).

Figure SPM.10 | Global RE primary energy supply (direct equivalent) by source in the group of Annex I (AI) and the group of Non-Annex I (NAI) countries in 164 long-term scenarios

by 2030 and 2050. The thick black line corresponds to the median, the coloured box corresponds to the inter-quartile range (25th to 75th percentile) and the ends of the white

surrounding bars correspond to the total range across all reviewed scenarios. [Figure 10.8, 10.2.2.5]

Notes: For details on the use of the ‘direct equivalent’ method of accounting for primary energy supply and the implied care needed in the interpretation of scenario results, see Box

SPM.2. More specifi cally, the ranges of secondary energy provided from bioenergy, wind energy and direct solar energy can be considered of comparable magnitude in their higher

penetration scenarios in 2050. Ocean energy is not presented here as only very few scenarios consider this RE technology.

2030

AI NAI AI NAI AI NAI AI NAI AI NAI

[EJ/yr]

0

50

100

150

200

2050

[EJ/yr]

0

50

100

150

200

AI NAI AI NAI AI NAI AI NAI AI NAI

Bioenergy

Hydropower

Wind Energy

Direct Solar Energy

Geothermal Energy

Maximum

75th

Median

25th

Minimum

23

Summaries Summary for Policymakers

Scenarios do not indicate an obvious single dominant RE technology at a global level; in addition, the

global overall technical potentials do not constrain the future contribution of RE. Although the contribution of

RE technologies varies across scenarios, modern biomass, wind and direct solar commonly make up the largest contri-

butions of RE technologies to the energy system by 2050 (Figure SPM.11). All scenarios assessed confi rm that technical

potentials will not be the limiting factors for the expansion of RE at a global scale. Despite signifi cant technological and

regional differences, in the four illustrative scenarios less than 2.5% of the global available technical RE potential is

used. [10.2, 10.3]

Wind Energy

20502030

Primary Energy Supply [EJ/yr]

0

50

150

100

Direct Solar Energy

20502030

Hydropower

20502030

Geothermal Energy

20502030

20502030

Bioenergy

CO

2

Concentration Levels

Baselines

Cat. III + IV (440 - 600 ppm)

Cat. I + II (<440 ppm)

Primary Energy Supply is Accounted for Based on Secondary Energy ProducedBioenergy Supply is Accounted for Prior to Conversion

300

Primary Energy Supply [EJ/yr]

0

50

150

100

Primary Energy Supply [EJ/yr]

0

50

150

100

Primary Energy Supply [EJ/yr]

0

50

150

100

200

250

350

Primary Energy Supply [EJ/yr]

0

50

150

100

Deployment Level 2008

Maximum

75th

Median

25th

Minimum

Figure SPM.11 | Global primary energy supply (direct equivalent) of bioenergy, wind, direct solar, hydro, and geothermal energy in 164 long-term scenarios in 2030 and 2050,

and grouped by different categories of atmospheric CO

2

concentration level that are defi ned consistently with those in the AR4. The thick black line corresponds to the median, the

coloured box corresponds to the inter-quartile range (25th to 75th percentile) and the ends of the white surrounding bars correspond to the total range across all reviewed scenarios.

[Excerpt from Figure 10.9, 10.2.2.5]

Notes: For details on the use of the ‘direct equivalent’ method of accounting for primary energy supply and the implied care needed in the interpretation of scenario results, see Box

SPM.2. More specifi cally, the ranges of secondary energy provided from bioenergy, wind energy and direct solar energy can be considered of comparable magnitude in their higher

penetration scenarios in 2050. Ocean energy is not presented here as only very few scenarios consider this RE technology. Note that categories V and above are not included and

category IV is extended to 600 ppm from 570 ppm, because all stabilization scenarios lie below 600 ppm CO

2

in 2100 and because the lowest baselines scenarios reach concentra-

tion levels of slightly more than 600 ppm by 2100.

24

Summary for Policymakers Summaries

Individual studies indicate that if RE deployment is limited, mitigation costs increase and low GHG concen-

tration stabilizations may not be achieved. A number of studies have pursued scenario sensitivities that assume

constraints on the deployment of individual mitigation options, including RE as well as nuclear and fossil energy with

CCS. There is little agreement on the precise magnitude of the cost increase. [10.2]

A transition to a low-GHG economy with higher shares of RE would imply increasing investments in technol-

ogies and infrastructure. The four illustrative scenarios analyzed in detail in the SRREN estimate global cumulative RE

investments (in the power generation sector only) ranging fromUSD

2005

1,360 to 5,100 billion for the decade 2011to

2020, and from USD

2005

1,490 to 7,180 billion for the decade 2021 to 2030. The lower values refer to the IEA World

Energy Outlook 2009 Reference Scenario and the higher ones to a scenario that seeks to stabilize atmospheric CO

2

(only) concentration at 450 ppm. The annual averages of these investment needs are all smaller than 1% of the world’s

gross domestic product (GDP). Beyond differences in the design of the models used to investigate these scenarios,

the range can be explained mainly by differences in GHG concentrations assessed and constraints imposed on the set

of admissible mitigation technologies. Increasing the installed capacity of RE power plants will reduce the amount of

fossil and nuclear fuels that otherwise would be needed in order to meet a given electricity demand. In addition to

investment, operation and maintenance (O&M) and (where applicable) feedstock costs related to RE power plants, any

assessment of the overall economic burden that is associated with their application will have to consider avoided fuel

and substituted investment costs as well. Even without taking the avoided costs into account, the lower range of the

RE power investments discussed above is lower than the respective investments reported for 2009. The higher values of

the annual averages of the RE power sector investment approximately correspond to a fi ve-fold increase in the current

global investments in this fi eld. [10.5, 11.2.2]

7. Policy, implementation and fi nancing

An increasing number and variety of RE policies—motivated by many factors—have driven escalated

growth of RE technologies in recent years. [1.4, 11.2, 11.5, 11.6] Government policies play a crucial role in acceler-

ating the deployment of RE technologies. Energy access and social and economic development have been the primary

drivers in most developing countries whereas secure energy supply and environmental concerns have been most

important in developed countries [9.3, 11.3]. The focus of policies is broadening from a concentration primarily on RE

electricity to include RE heating and cooling and transportation. [11.2, 11.5]

RE-specifi c policies for research, development, demonstration and deployment help to level the playing fi eld for RE.

Policies include regulations such as feed-in-tariffs, quotas, priority grid access, building mandates, biofuel blending

requirements, and bioenergy sustainability criteria. [2.4.5.2, 2.ES, TS.2.8.1] Other policy categories are fi scal incentives

such as tax policies and direct government payments such as rebates and grants; and public fi nance mechanisms such

as loans and guarantees. Wider policies aimed at reducing GHG emissions such as carbon pricing mechanisms may also

support RE.

Policies can be sector specifi c, can be implemented at the local, state/provincial, national and in some cases regional

level, and can be complemented by bilateral, regional and international cooperation. [11.5]

Policies have promoted an increase in RE capacity installations by helping to overcome various barriers. [1.4,

11.1, 11.4, 11.5, 11.6] Barriers to RE deployment include:

• Institutional and policy barriers related to existing industry, infrastructure and regulation of the energy system;

• Market failures, including non-internalized environmental and health costs, where applicable;

25

Summaries Summary for Policymakers

• Lack of general information and access to data relevant to the deployment of RE, and lack of technical and knowl-

edge capacity; and

• Barriers related to societal and personal values and affecting the perception and acceptance of RE technologies.

[1.4, 9.5.1, 9.5.2.1]

Public R&D investments in RE technologies are most effective when complemented by other policy instru-

ments, particularly deployment policies that simultaneously enhance demand for new technologies. Together,

R&D and deployment policies create a positive feedback cycle, inducing private sector investment. Enacting deployment

policies early in the development of a given technology can accelerate learning by inducing private R&D, which in turn

further reduces costs and provides additional incentives for using the technology. [11.5.2]

Some policies have been shown to be effective and effi cient in rapidly increasing RE deployment. However,

there is no one-size-fi ts-all policy. Experience shows that different policies or combinations of policies can be more

effective and effi cient depending on factors such as the level of technological maturity, affordable capital, ease of inte-

gration into the existing system and the local and national RE resource base. [11.5]

• Several studies have concluded that some feed in tariffs have been effective and effi cient at promoting RE elec-

tricity, mainly due to the combination of long-term fi xed price or premium payments, network connections, and

guaranteed purchase of all RE electricity generated. Quota policies can be effective and effi cient if designed to

reduce risk; for example, with long-term contracts. [11.5.4]

• An increasing number of governments are adopting fi scal incentives for RE heating and cooling. Obligations to

use RE heat are gaining attention for their potential to encourage growth independent of public fi nancial support.

[11.5.5]

• In the transportation sector, RE fuel mandates or blending requirements are key drivers in the development of most

modern biofuel industries. Other policies include direct government payments or tax reductions. Policies have infl u-

enced the development of an international biofuel trade. [11.5.6]

The fl exibility to adjust as technologies, markets and other factors evolve is important. The details of design and imple-

mentation are critical in determining the effectiveness and effi ciency of a policy. [11.5]. Policy frameworks that are

transparent and sustained can reduce investment risks and facilitate deployment of RE and the evolution of low-cost

applications. [11.5, 11.6]

‘Enabling’ policies support RE development and deployment. A favourable, or enabling, environment for RE

can be created by addressing the possible interactions of a given policy with other RE policies as well as with energy

and non-energy policies (e.g., those targeting agriculture, transportation, water management and urban planning); by