xxi

Technical Summary

Summary for Policymakers

1

SPM

Drafting Authors:

Ottmar Edenhofer (Germany), Ramón Pichs-Madruga (Cuba), Youba Sokona (Mali), Shardul

Agrawala (France), Igor Alexeyevich Bashmakov (Russia), Gabriel Blanco (Argentina), John

Broome (UK), Thomas Bruckner (Germany), Steffen Brunner (Germany), Mercedes Bustamante

(Brazil), Leon Clarke (USA), Felix Creutzig (Germany), Shobhakar Dhakal (Nepal / Thailand), Navroz

K. Dubash (India), Patrick Eickemeier (Germany), Ellie Farahani (Canada), Manfred Fischedick

(Germany), Marc Fleurbaey (France), Reyer Gerlagh (Netherlands), Luis Gómez-Echeverri

(Colombia / Austria), Sujata Gupta (India / Philippines), Jochen Harnisch (Germany), Kejun Jiang

(China), Susanne Kadner (Germany), Sivan Kartha (USA), Stephan Klasen (Germany), Charles

Kolstad (USA), Volker Krey (Austria / Germany), Howard Kunreuther (USA), Oswaldo Lucon

(Brazil), Omar Masera (México), Jan Minx (Germany), Yacob Mulugetta (Ethiopia / UK), Anthony

Patt (Austria / Switzerland), Nijavalli H. Ravindranath (India), Keywan Riahi (Austria), Joyashree

Roy (India), Roberto Schaeffer (Brazil), Steffen Schlömer (Germany), Karen Seto (USA), Kristin

Seyboth (USA), Ralph Sims (New Zealand), Jim Skea (UK), Pete Smith (UK), Eswaran Somanathan

(India), Robert Stavins (USA), Christoph von Stechow (Germany), Thomas Sterner (Sweden), Taishi

Sugiyama (Japan), Sangwon Suh (Republic of Korea / USA), Kevin Chika Urama (Nigeria / UK / Kenya),

Diana Ürge-Vorsatz (Hungary), David G. Victor (USA), Dadi Zhou (China), Ji Zou (China), Timm

Zwickel (Germany)

Draft Contributing Authors

Giovanni Baiocchi (UK / Italy), Helena Chum (Brazil / USA), Jan Fuglestvedt (Norway), Helmut

Haberl (Austria), Edgar Hertwich (Austria / Norway), Elmar Kriegler (Germany), Joeri Rogelj

(Switzerland / Belgium), H.-Holger Rogner (Germany), Michiel Schaeffer (Netherlands), StevenJ.

Smith (USA), Detlef van Vuuren (Netherlands), Ryan Wiser (USA)

This Summary for Policymakers should be cited as:

IPCC, 2014: Summary for Policymakers. In: Climate Change 2014: Mitigation of Climate Change. Contribution of Work-

ing Group III to the Fifth Assessment Report of the Intergovernmental Panel on Climate Change [Edenhofer, O., R.

Pichs-Madruga, Y. Sokona, E. Farahani, S. Kadner, K. Seyboth, A. Adler, I. Baum, S. Brunner, P. Eickemeier, B. Kriemann, J.

Savolainen, S. Schlömer, C. von Stechow, T. Zwickel and J.C. Minx (eds.)]. Cambridge University Press, Cambridge, United

Kingdom and New York, NY, USA.

Summary

for Policymakers

SPM

3

SPM

Summary for Policymakers

SPMSPM

Table of Contents

SPM.1 Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4

SPM.2 Approaches to climate change mitigation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4

SPM.3 Trends in stocks and flows of greenhouse gases and their drivers . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6

SPM.4 Mitigation pathways and measures in the context of sustainable development . . . . . . . . . . . . . . . . . . 10

SPM.4.1 Long-term mitigation pathways . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .10

SPM.4.2 Sectoral and cross-sectoral mitigation pathways and measures . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .17

SPM.4.2.1 Cross-sectoral mitigation pathways and measures . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .17

SPM.4.2.2 Energy supply . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 20

SPM.4.2.3 Energy end-use sectors . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .21

SPM.4.2.4 Agriculture, Forestry and Other Land Use (AFOLU) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .24

SPM.4.2.5 Human settlements, infrastructure and spatial planning . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 25

SPM.5 Mitigation policies and institutions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .26

SPM.5.1 Sectoral and national policies . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .26

SPM.5.2 International cooperation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .30

4

SPM

Summary for PolicymakersSummary for Policymakers

SPM

Introduction

The Working Group III contribution to the IPCC’s Fifth Assessment Report (AR5) assesses literature on the scientific,

technological, environmental, economic and social aspects of mitigation of climate change. It builds upon the Working

Group III contribution to the IPCC’s Fourth Assessment Report (AR4), the Special Report on Renewable Energy Sources

and Climate Change Mitigation (SRREN) and previous reports and incorporates subsequent new findings and research.

The report also assesses mitigation options at different levels of governance and in different economic sectors, and the

societal implications of different mitigation policies, but does not recommend any particular option for mitigation.

This Summary for Policymakers (SPM) follows the structure of the Working Group III report. The narrative is supported

by a series of highlighted conclusions which, taken together, provide a concise summary. The basis for the SPM can be

found in the chapter sections of the underlying report and in the Technical Summary (TS). References to these are given

in square brackets.

The degree of certainty in findings in this assessment, as in the reports of all three Working Groups, is based on the

author teams’ evaluations of underlying scientific understanding and is expressed as a qualitative level of confidence

(from very low to very high) and, when possible, probabilistically with a quantified likelihood (from exceptionally unlikely

to virtually certain). Confidence in the validity of a finding is based on the type, amount, quality, and consistency of

evidence (e. g., data, mechanistic understanding, theory, models, expert judgment) and the degree of agreement.

1

Probabilistic estimates of quantified measures of uncertainty in a finding are based on statistical analysis of observations

or model results, or both, and expert judgment.

2

Where appropriate, findings are also formulated as statements of fact

without using uncertainty qualifiers. Within paragraphs of this summary, the confidence, evidence, and agreement terms

given for a bolded finding apply to subsequent statements in the paragraph, unless additional terms are provided.

Approaches to climate change mitigation

Mitigation is a human intervention to reduce the sources or enhance the sinks of greenhouse gases. Mitiga-

tion, together with adaptation to climate change, contributes to the objective expressed in Article 2 of the United Nations

Framework Convention on Climate Change (UNFCCC):

The ultimate objective of this Convention and any related legal instruments that the Conference of the Parties may

adopt is to achieve, in accordance with the relevant provisions of the Convention, stabilization of greenhouse gas

concentrations in the atmosphere at a level that would prevent dangerous anthropogenic interference with the

climate system. Such a level should be achieved within a time frame sufficient to allow ecosystems to adapt natu-

rally to climate change, to ensure that food production is not threatened and to enable economic development to

proceed in a sustainable manner.

Climate policies can be informed by the findings of science, and systematic methods from other disciplines. [1.2, 2.4, 2.5,

Box 3.1]

1

The following summary terms are used to describe the available evidence: limited, medium, or robust; and for the degree of agreement: low,

medium, or high. A level of confidence is expressed using five qualifiers: very low, low, medium, high, and very high, and typeset in italics, e. g.,

medium confidence. For a given evidence and agreement statement, different confidence levels can be assigned, but increasing levels of evidence

and degrees of agreement are correlated with increasing confidence. For more details, please refer to the guidance note for Lead Authors of the

IPCC Fifth Assessment Report on consistent treatment of uncertainties.

2

The following terms have been used to indicate the assessed likelihood of an outcome or a result: virtually certain 99 – 100 % probability, very

likely 90 – 100 %, likely 66 – 100 %, about as likely as not 33 – 66 %, unlikely 0 – 33 %, very unlikely 0 – 10 %, exceptionally unlikely 0 – 1 %. Addi-

tional terms (more likely than not > 50 – 100 %, and more unlikely than likely 0 – < 50 %) may also be used when appropriate. Assessed likelihood

is typeset in italics, e. g., very likely.

SPM.1

SPM.2

5

SPM

Summary for Policymakers

Sustainable development and equity provide a basis for assessing climate policies and highlight the need for

addressing the risks of climate change.

3

Limiting the effects of climate change is necessary to achieve sustainable

development and equity, including poverty eradication. At the same time, some mitigation efforts could undermine action

on the right to promote sustainable development, and on the achievement of poverty eradication and equity. Conse-

quently, a comprehensive assessment of climate policies involves going beyond a focus on mitigation and adaptation

policies alone to examine development pathways more broadly, along with their determinants. [4.2, 4.3, 4.4, 4.5, 4.6, 4.8]

Effective mitigation will not be achieved if individual agents advance their own interests independently.

Climate change has the characteristics of a collective action problem at the global scale, because most greenhouse

gases (GHGs) accumulate over time and mix globally, and emissions by any agent (e. g., individual, community, company,

country) affect other agents.

4

International cooperation is therefore required to effectively mitigate GHG emissions and

address other climate change issues [1.2.4, 2.6.4, 3.2, 4.2, 13.2, 13.3]. Furthermore, research and development in support

of mitigation creates knowledge spillovers. International cooperation can play a constructive role in the development, dif-

fusion and transfer of knowledge and environmentally sound technologies [1.4.4, 3.11.6, 11.8, 13.9, 14.4.3].

Issues of equity, justice, and fairness arise with respect to mitigation and adaptation.

5

Countries’ past and

future contributions to the accumulation of GHGs in the atmosphere are different, and countries also face varying chal-

lenges and circumstances, and have different capacities to address mitigation and adaptation. The evidence suggests that

outcomes seen as equitable can lead to more effective cooperation. [3.10, 4.2.2, 4.6.2]

Many areas of climate policy-making involve value judgements and ethical considerations. These areas range

from the question of how much mitigation is needed to prevent dangerous interference with the climate system to

choices among specific policies for mitigation or adaptation [3.1, 3.2]. Social, economic and ethical analyses may be

used to inform value judgements and may take into account values of various sorts, including human wellbeing, cultural

values and non-human values [3.4, 3.10].

Among other methods, economic evaluation is commonly used to inform climate policy design. Practical tools

for economic assessment include cost-benefit analysis, cost-effectiveness analysis, multi-criteria analysis and expected

utility theory [2.5]. The limitations of these tools are well-documented [3.5]. Ethical theories based on social welfare

functions imply that distributional weights, which take account of the different value of money to different people, should

be applied to monetary measures of benefits and harms [3.6.1, Box TS.2]. Whereas distributional weighting has not

frequently been applied for comparing the effects of climate policies on different people at a single time, it is standard

practice, in the form of discounting, for comparing the effects at different times [3.6.2].

Climate policy intersects with other societal goals creating the possibility of co-benefits or adverse side-

effects. These intersections, if well-managed, can strengthen the basis for undertaking climate action. Mitiga-

tion and adaptation can positively or negatively influence the achievement of other societal goals, such as those related

to human health, food security, biodiversity, local environmental quality, energy access, livelihoods, and equitable sus-

tainable development; and vice versa, policies toward other societal goals can influence the achievement of mitigation

and adaptation objectives [4.2, 4.3, 4.4, 4.5, 4.6, 4.8]. These influences can be substantial, although sometimes difficult

to quantify, especially in welfare terms [3.6.3]. This multi-objective perspective is important in part because it helps to

identify areas where support for policies that advance multiple goals will be robust [1.2.1, 4.2, 4.8, 6.6.1].

3

See WGII AR5 SPM.

4

In the social sciences this is referred to as a ‘global commons problem‘. As this expression is used in the social sciences, it has no specific implica-

tions for legal arrangements or for particular criteria regarding effort-sharing.

5

See FAQ 3.2 for clarification of these concepts. The philosophical literature on justice and other literature can illuminate these issues [3.2, 3.3, 4.6.2].

SPM

6

SPM

Summary for Policymakers

Climate policy may be informed by a consideration of a diverse array of risks and uncertainties, some of

which are difficult to measure, notably events that are of low probability but which would have a significant

impact if they occur. Since AR4, the scientific literature has examined risks related to climate change, adaptation,

and mitigation strategies. Accurately estimating the benefits of mitigation takes into account the full range of possible

impacts of climate change, including those with high consequences but a low probability of occurrence. The benefits of

mitigation may otherwise be underestimated (high confidence) [2.5, 2.6, Box 3.9]. The choice of mitigation actions is also

influenced by uncertainties in many socio-economic variables, including the rate of economic growth and the evolution

of technology (high confidence) [2.6, 6.3].

The design of climate policy is influenced by how individuals and organizations perceive risks and uncertain-

ties and take them into account. People often utilize simplified decision rules such as a preference for the status quo.

Individuals and organizations differ in their degree of risk aversion and the relative importance placed on near-term

versus long-term ramifications of specific actions [2.4]. With the help of formal methods, policy design can be improved

by taking into account risks and uncertainties in natural, socio-economic, and technological systems as well as decision

processes, perceptions, values and wealth [2.5].

Trends in stocks and flows of greenhouse gases

and their drivers

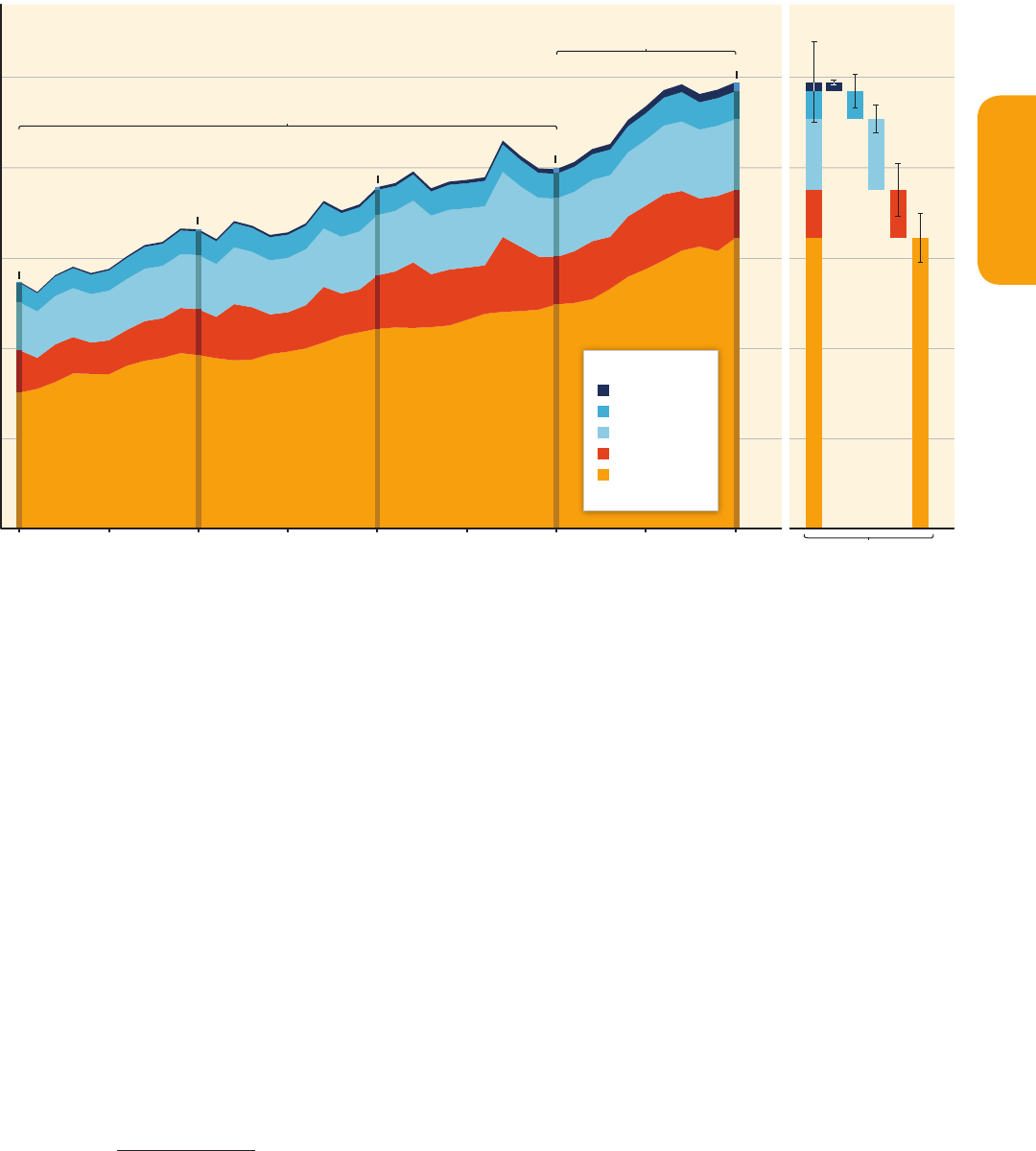

Total anthropogenic GHG emissions have continued to increase over 1970 to 2010 with larger absolute decadal

increases toward the end of this period (high confidence). Despite a growing number of climate change mitigation poli-

cies, annual GHG emissions grew on average by 1.0 gigatonne carbon dioxide equivalent (GtCO

2

eq) (2.2 %) per year from

2000 to 2010 compared to 0.4 GtCO

2

eq (1.3 %) per year from 1970 to 2000 (Figure SPM.1).

6,7

Total anthropogenic GHG

emissions were the highest in human history from 2000 to 2010 and reached 49 (±4.5) GtCO

2

eq / yr in 2010. The global

economic crisis 2007 / 2008 only temporarily reduced emissions. [1.3, 5.2, 13.3, 15.2.2, Box TS.5, Figure 15.1]

CO

2

emissions from fossil fuel combustion and industrial processes contributed about 78 % of the total GHG

emission increase from 1970 to 2010, with a similar percentage contribution for the period 2000 – 2010

(high confidence). Fossil fuel-related CO

2

emissions reached 32 (±2.7) GtCO

2

/ yr, in 2010, and grew further by about

3 % between 2010 and 2011 and by about 1 – 2 % between 2011 and 2012. Of the 49 (±4.5) GtCO

2

eq / yr in total

anthropogenic GHG emissions in 2010, CO

2

remains the major anthropogenic GHG accounting for 76 % (38 ± 3.8

GtCO

2

eq / yr) of total anthropogenic GHG emissions in 2010. 16 % (7.8 ± 1.6 GtCO

2

eq / yr) come from methane (CH

4

), 6.2 %

(3.1 ± 1.9 GtCO

2

eq / yr) from nitrous oxide (N

2

O), and 2.0 % (1.0 ± 0.2 GtCO

2

eq / yr) from fluorinated gases ( FigureSPM.1).

Annually, since 1970, about 25 % of anthropogenic GHG emissions have been in the form of non-CO

2

gases.

8

[1.2, 5.2]

6

Throughout the SPM, emissions of GHGs are weighed by Global Warming Potentials with a 100-year time horizon (GWP

100

) from the IPCC Second

Assessment Report. All metrics have limitations and uncertainties in assessing consequences of different emissions. [3.9.6, Box TS.5,

Annex II.9, WGI SPM]

7

In this SPM, uncertainty in historic GHG emission data is reported using 90 % uncertainty intervals unless otherwise stated. GHG emission levels

are rounded to two significant digits throughout this document; as a consequence, small differences in sums due to rounding may occur.

8

In this report, data on non-CO

2

GHGs, including fluorinated gases, are taken from the EDGAR database (Annex II.9), which covers substances

included in the Kyoto Protocol in its first commitment period.

SPM.3

7

SPM

Summary for Policymakers

About half of cumulative anthropogenic CO

2

emissions between 1750 and 2010 have occurred in the last 40

years (high confidence). In 1970, cumulative CO

2

emissions from fossil fuel combustion, cement production and flaring

since 1750 were 420 ± 35 GtCO

2

; in 2010, that cumulative total had tripled to 1300 ± 110 GtCO

2

. Cumulative CO

2

emissions

from Forestry and Other Land Use (FOLU)

9

since 1750 increased from 490 ± 180 GtCO

2

in 1970 to 680 ± 300 GtCO

2

in 2010.

[5.2]

Annual anthropogenic GHG emissions have increased by 10 GtCO

2

eq between 2000 and 2010, with this

increase directly coming from energy supply (47 %), industry (30 %), transport (11 %) and buildings (3 %)

sectors (medium confidence). Accounting for indirect emissions raises the contributions of the buildings and

industry sectors (high confidence). Since 2000, GHG emissions have been growing in all sectors, except AFOLU. Of the

49 (±4.5) GtCO

2

eq emissions in 2010, 35 % (17 GtCO

2

eq) of GHG emissions were released in the energy supply sector,

9

Forestry and Other Land Use (FOLU)—also referred to as LULUCF (Land Use, Land-Use Change, and Forestry)—is the subset of Agriculture,

Forestry and Other Land Use (AFOLU) emissions and removals of GHGs related to direct human-induced land use, land-use change and forestry

activities excluding agricultural emissions and removals (see WGIII AR5 Glossary).

Figure SPM.1 | Total annual anthropogenic GHG emissions (GtCO

2

eq / yr) by groups of gases 1970 – 2010: CO

2

from fossil fuel combustion and industrial processes; CO

2

from

Forestry and Other Land Use (FOLU); methane (CH

4

); nitrous oxide (N

2

O); fluorinated gases

8

covered under the Kyoto Protocol (F-gases). At the right side of the figure GHG emis-

sions in 2010 are shown again broken down into these components with the associated uncertainties (90 % confidence interval) indicated by the error bars. Total anthropogenic

GHG emissions uncertainties are derived from the individual gas estimates as described in Chapter 5 [5.2.3.6]. Global CO

2

emissions from fossil fuel combustion are known within

8 % uncertainty (90 % confidence interval). CO

2

emissions from FOLU have very large uncertainties attached in the order of ± 50 %. Uncertainty for global emissions of CH

4

, N

2

O

and the F-gases has been estimated as 20 %, 60 % and 20 %, respectively. 2010 was the most recent year for which emission statistics on all gases as well as assessment of

uncertainties were essentially complete at the time of data cut-off for this report. Emissions are converted into CO

2

-equivalents based on GWP

100

6

from the IPCC Second Assessment

Report. The emission data from FOLU represents land-based CO

2

emissions from forest fires, peat fires and peat decay that approximate to net CO

2

flux from FOLU as described in

Chapter 11 of this report. Average annual growth rate over different periods is highlighted with the brackets. [Figure 1.3, Figure TS.1]

27 Gt

33 Gt

55%

17%

19%

7.9%

0.44%

58%

15%

18%

7.9%

0.67%

62%

13%

16%

6.9%

1.3%

38 Gt

40 Gt

59%

16%

18%

7.4%

0.81%

49 Gt

65%

11%

16%

6.2%

2.0%

2005

Gas

CO

2

Fossil Fuel and

Industrial Processes

CO

2

FOLU

CH

4

N

2

O

F-Gases

GHG Emissions [GtCO

2

eq/yr]

0

10

20

30

40

50

2010200520001995199019851980

19751970

+2.2%/yr

2000 – 2010

+1.3%/yr

1970 – 2000

2010

Total Annual Anthropogenic GHG Emissions by Groups of Gases 1970 – 2010

8

SPM

Summary for Policymakers

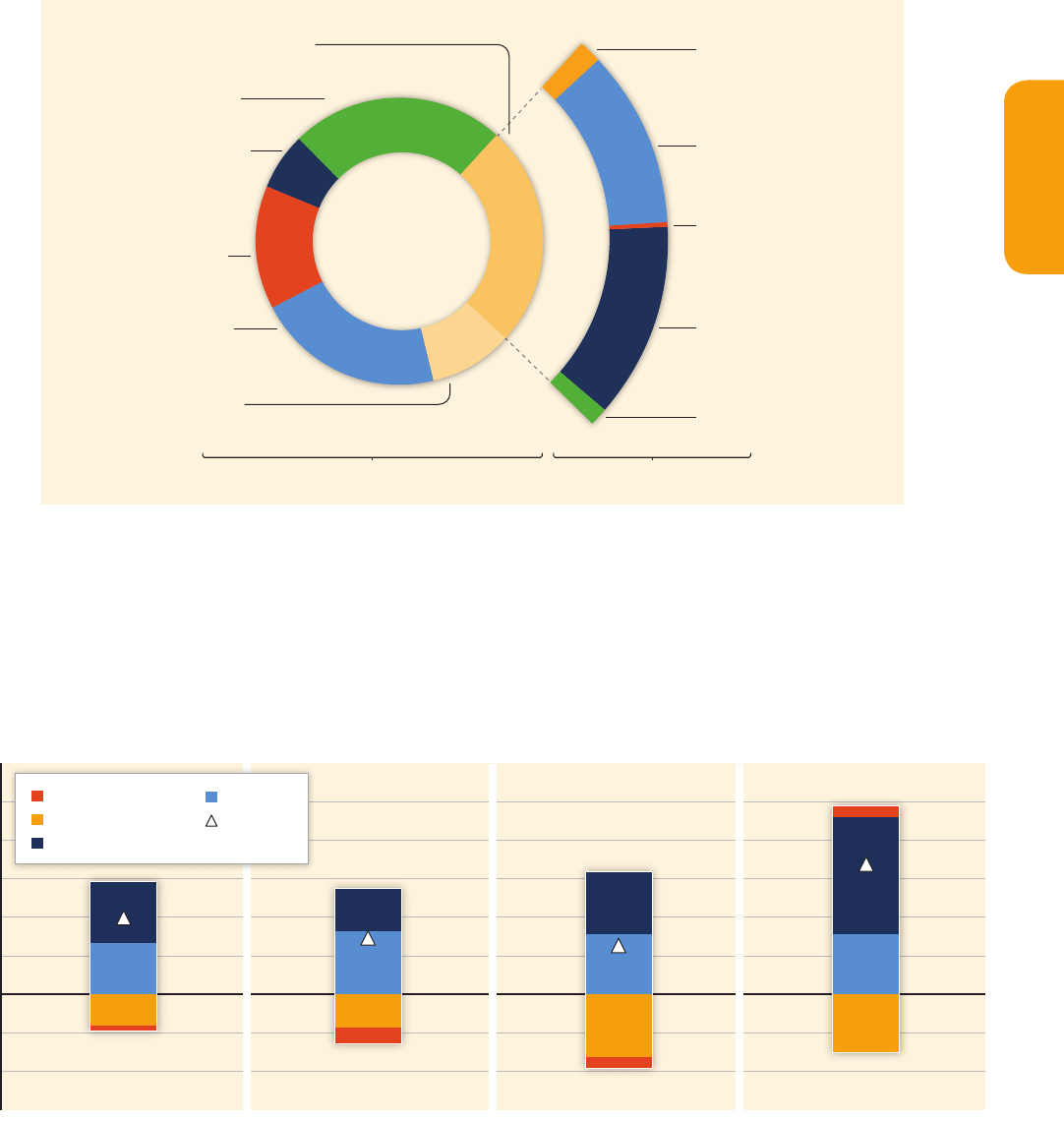

24 % (12 GtCO

2

eq, net emissions) in AFOLU, 21 % (10 GtCO

2

eq) in industry, 14 % (7.0 GtCO

2

eq) in transport and 6.4 %

(3.2 GtCO

2

eq) in buildings. When emissions from electricity and heat production are attributed to the sectors that use

the final energy (i. e. indirect emissions), the shares of the industry and buildings sectors in global GHG emissions are

increased to 31 % and 19 %

7

, respectively (Figure SPM.2). [7.3, 8.2, 9.2, 10.3, 11.2]

Globally, economic and population growth continue to be the most important drivers of increases in CO

2

emissions from fossil fuel combustion. The contribution of population growth between 2000 and 2010

remained roughly identical to the previous three decades, while the contribution of economic growth has

risen sharply (high confidence). Between 2000 and 2010, both drivers outpaced emission reductions from improve-

ments in energy intensity (Figure SPM.3). Increased use of coal relative to other energy sources has reversed the

long-standing trend of gradual decarbonization of the world’s energy supply. [1.3, 5.3, 7.2, 14.3, TS.2.2]

Without additional efforts to reduce GHG emissions beyond those in place today, emissions growth is

expected to persist driven by growth in global population and economic activities. Baseline scenarios, those

without additional mitigation, result in global mean surface temperature increases in 2100 from 3.7 °C to

4.8 °C compared to pre-industrial levels

10

(range based on median climate response; the range is 2.5 °C to

7.8 °C when including climate uncertainty, see Table SPM.1)

11

(high confidence). The emission scenarios collected for

this assessment represent full radiative forcing including GHGs, tropospheric ozone, aerosols and albedo change. Baseline

scenarios (scenarios without explicit additional efforts to constrain emissions) exceed 450 parts per million (ppm) CO

2

eq

by 2030 and reach CO

2

eq concentration levels between 750 and more than 1300 ppm CO

2

eq by 2100. This is similar to

the range in atmospheric concentration levels between the RCP 6.0 and RCP 8.5 pathways in 2100.

12

For comparison, the

CO

2

eq concentration in 2011 is estimated to be 430 ppm (uncertainty range 340 – 520 ppm).

13

[6.3, Box TS.6; WGI Figure

SPM.5, WGI 8.5, WGI 12.3]

10

Based on the longest global surface temperature dataset available, the observed change between the average of the period 1850 – 1900 and of

the AR5 reference period (1986 – 2005) is 0.61 °C (5 – 95 % confidence interval: 0.55 – 0.67 °C) [WGI SPM.E], which is used here as an approxi-

mation of the change in global mean surface temperature since pre-industrial times, referred to as the period before 1750.

11

The climate uncertainty reflects the 5th to 95th percentile of climate model calculations described in Table SPM.1.

12

For the purpose of this assessment, roughly 300 baseline scenarios and 900 mitigation scenarios were collected through an open call from

integrated modelling teams around the world. These scenarios are complementary to the Representative Concentration Pathways (RCPs, see

WGIII

AR5 Glossary). The RCPs are identified by their approximate total radiative forcing in year 2100 relative to 1750: 2.6 Watts per square meter

(

W /

m

2

) for RCP2.6, 4.5 W / m

2

for RCP4.5, 6.0 W / m

2

for RCP6.0, and 8.5 W /

m

2

for RCP8.5. The scenarios collected for this assessment span a

slightly broader range of concentrations in the year 2100 than the four RCPs.

13

This is based on the assessment of total anthropogenic radiative forcing for 2011 relative to 1750 in WGI, i. e. 2.3 W /

m

2

, uncertainty range 1.1 to

3.3 W /

m

2

. [WGI Figure SPM.5, WGI 8.5, WGI 12.3]

Figure SPM.2 | Total anthropogenic GHG emissions (GtCO

2

eq / yr) by economic sectors. Inner circle shows direct GHG emission shares (in % of total anthropogenic GHG emissions)

of five economic sectors in 2010. Pull-out shows how indirect CO

2

emission shares (in % of total anthropogenic GHG emissions) from electricity and heat production are attributed

to sectors of final energy use. ‘Other Energy’ refers to all GHG emission sources in the energy sector as defined in Annex II other than electricity and heat production [A.II.9.1]. The

emissions data from Agriculture, Forestry and Other Land Use (AFOLU) includes land-based CO

2

emissions from forest fires, peat fires and peat decay that approximate to net CO

2

flux from the Forestry and Other Land Use (FOLU) sub-sector as described in Chapter 11 of this report. Emissions are converted into CO

2

-equivalents based on GWP

100

6

from the

IPCC Second Assessment Report. Sector definitions are provided in Annex II.9. [Figure 1.3a, Figure TS.3 upper panel]

Greenhouse Gas Emissions by Economic Sectors

Indirect CO

2

Emissions

Direct Emissions

Buildings

6.4%

Transport

14%

Industry

21%

Other

Energy

9.6%

Electricity

and Heat Production

25%

49 Gt CO

2

eq

(2010)

AFOLU

24%

Buildings

12%

Transport

0.3%

Industry

11%

Energy

1.4%

AFOLU

0.87%

Figure SPM.3 | Decomposition of the change in total annual CO

2

emissions from fossil fuel combustion by decade and four driving factors: population, income (GDP) per capita,

energy intensity of GDP and carbon intensity of energy. The bar segments show the changes associated with each factor alone, holding the respective other factors constant. Total

emissions changes are indicated by a triangle. The change in emissions over each decade is measured in gigatonnes of CO

2

per year [GtCO

2

/ yr]; income is converted into common

units using purchasing power parities. [Figure 1.7]

1970-1980 1980-1990 1990-2000 2000-2010

-6

-4

-2

0

2

4

6

8

10

12

Change in Annual CO

2

Emissions by Decade [GtCO

2

/yr]

CarbonIntensity of Energy

EnergyIntensity of GDP

GDPperCapita

Population

TotalChange

6.8

2.5

2.9

4.0

Decomposition of the Change in Total Annual CO

2

Emissions from Fossil Fuel Combustion by Decade

9

SPM

Summary for Policymakers

24 % (12 GtCO

2

eq, net emissions) in AFOLU, 21 % (10 GtCO

2

eq) in industry, 14 % (7.0 GtCO

2

eq) in transport and 6.4 %

(3.2 GtCO

2

eq) in buildings. When emissions from electricity and heat production are attributed to the sectors that use

the final energy (i. e. indirect emissions), the shares of the industry and buildings sectors in global GHG emissions are

increased to 31 % and 19 %

7

, respectively (Figure SPM.2). [7.3, 8.2, 9.2, 10.3, 11.2]

Globally, economic and population growth continue to be the most important drivers of increases in CO

2

emissions from fossil fuel combustion. The contribution of population growth between 2000 and 2010

remained roughly identical to the previous three decades, while the contribution of economic growth has

risen sharply (high confidence). Between 2000 and 2010, both drivers outpaced emission reductions from improve-

ments in energy intensity (Figure SPM.3). Increased use of coal relative to other energy sources has reversed the

long-standing trend of gradual decarbonization of the world’s energy supply. [1.3, 5.3, 7.2, 14.3, TS.2.2]

Without additional efforts to reduce GHG emissions beyond those in place today, emissions growth is

expected to persist driven by growth in global population and economic activities. Baseline scenarios, those

without additional mitigation, result in global mean surface temperature increases in 2100 from 3.7 °C to

4.8 °C compared to pre-industrial levels

10

(range based on median climate response; the range is 2.5 °C to

7.8 °C when including climate uncertainty, see Table SPM.1)

11

(high confidence). The emission scenarios collected for

this assessment represent full radiative forcing including GHGs, tropospheric ozone, aerosols and albedo change. Baseline

scenarios (scenarios without explicit additional efforts to constrain emissions) exceed 450 parts per million (ppm) CO

2

eq

by 2030 and reach CO

2

eq concentration levels between 750 and more than 1300 ppm CO

2

eq by 2100. This is similar to

the range in atmospheric concentration levels between the RCP 6.0 and RCP 8.5 pathways in 2100.

12

For comparison, the

CO

2

eq concentration in 2011 is estimated to be 430 ppm (uncertainty range 340 – 520 ppm).

13

[6.3, Box TS.6; WGI Figure

SPM.5, WGI 8.5, WGI 12.3]

10

Based on the longest global surface temperature dataset available, the observed change between the average of the period 1850 – 1900 and of

the AR5 reference period (1986 – 2005) is 0.61 °C (5 – 95 % confidence interval: 0.55 – 0.67 °C) [WGI SPM.E], which is used here as an approxi-

mation of the change in global mean surface temperature since pre-industrial times, referred to as the period before 1750.

11

The climate uncertainty reflects the 5th to 95th percentile of climate model calculations described in Table SPM.1.

12

For the purpose of this assessment, roughly 300 baseline scenarios and 900 mitigation scenarios were collected through an open call from

integrated modelling teams around the world. These scenarios are complementary to the Representative Concentration Pathways (RCPs, see

WGIII

AR5 Glossary). The RCPs are identified by their approximate total radiative forcing in year 2100 relative to 1750: 2.6 Watts per square meter

(

W /

m

2

) for RCP2.6, 4.5 W / m

2

for RCP4.5, 6.0 W / m

2

for RCP6.0, and 8.5 W /

m

2

for RCP8.5. The scenarios collected for this assessment span a

slightly broader range of concentrations in the year 2100 than the four RCPs.

13

This is based on the assessment of total anthropogenic radiative forcing for 2011 relative to 1750 in WGI, i. e. 2.3 W /

m

2

, uncertainty range 1.1 to

3.3 W /

m

2

. [WGI Figure SPM.5, WGI 8.5, WGI 12.3]

Figure SPM.2 | Total anthropogenic GHG emissions (GtCO

2

eq / yr) by economic sectors. Inner circle shows direct GHG emission shares (in % of total anthropogenic GHG emissions)

of five economic sectors in 2010. Pull-out shows how indirect CO

2

emission shares (in % of total anthropogenic GHG emissions) from electricity and heat production are attributed

to sectors of final energy use. ‘Other Energy’ refers to all GHG emission sources in the energy sector as defined in Annex II other than electricity and heat production [A.II.9.1]. The

emissions data from Agriculture, Forestry and Other Land Use (AFOLU) includes land-based CO

2

emissions from forest fires, peat fires and peat decay that approximate to net CO

2

flux from the Forestry and Other Land Use (FOLU) sub-sector as described in Chapter 11 of this report. Emissions are converted into CO

2

-equivalents based on GWP

100

6

from the

IPCC Second Assessment Report. Sector definitions are provided in Annex II.9. [Figure 1.3a, Figure TS.3 upper panel]

Greenhouse Gas Emissions by Economic Sectors

Indirect CO

2

Emissions

Direct Emissions

Buildings

6.4%

Transport

14%

Industry

21%

Other

Energy

9.6%

Electricity

and Heat Production

25%

49 Gt CO

2

eq

(2010)

AFOLU

24%

Buildings

12%

Transport

0.3%

Industry

11%

Energy

1.4%

AFOLU

0.87%

Figure SPM.3 | Decomposition of the change in total annual CO

2

emissions from fossil fuel combustion by decade and four driving factors: population, income (GDP) per capita,

energy intensity of GDP and carbon intensity of energy. The bar segments show the changes associated with each factor alone, holding the respective other factors constant. Total

emissions changes are indicated by a triangle. The change in emissions over each decade is measured in gigatonnes of CO

2

per year [GtCO

2

/ yr]; income is converted into common

units using purchasing power parities. [Figure 1.7]

1970-1980 1980-1990 1990-2000 2000-2010

-6

-4

-2

0

2

4

6

8

10

12

Change in Annual CO

2

Emissions by Decade [GtCO

2

/yr]

CarbonIntensity of Energy

EnergyIntensity of GDP

GDPperCapita

Population

TotalChange

6.8

2.5

2.9

4.0

Decomposition of the Change in Total Annual CO

2

Emissions from Fossil Fuel Combustion by Decade

10

SPM

Summary for Policymakers

Mitigation pathways and measures in the context

of sustainable development

Long-term mitigation pathways

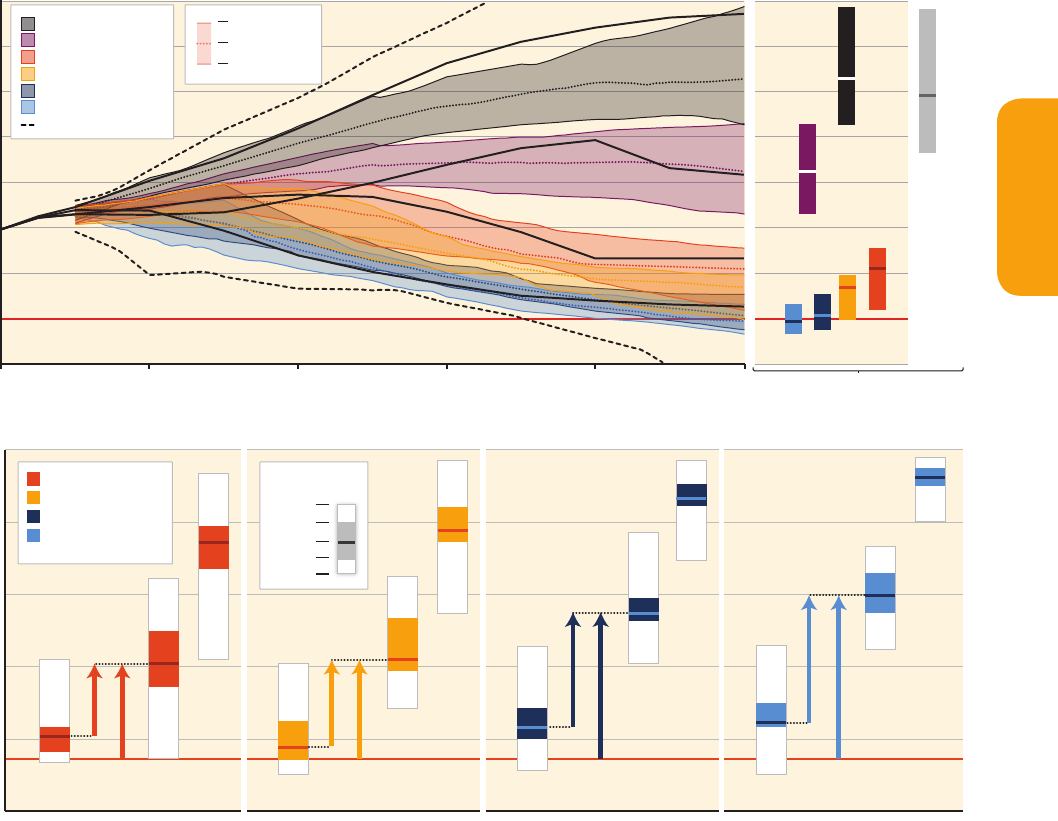

There are multiple scenarios with a range of technological and behavioral options, with different characteristics

and implications for sustainable development, that are consistent with different levels of mitigation. For this

assessment, about 900 mitigation scenarios have been collected in a database based on published integrated models.

14

This

range spans atmospheric concentration levels in 2100 from 430 ppm CO

2

eq to above 720 ppm CO

2

eq, which is comparable

to the 2100 forcing levels between RCP 2.6 and RCP 6.0. Scenarios outside this range were also assessed including some

scenarios with concentrations in 2100 below 430 ppm CO

2

eq (for a discussion of these scenarios see below). The mitigation

scenarios involve a wide range of technological, socioeconomic, and institutional trajectories, but uncertainties and model

limitations exist and developments outside this range are possible (Figure SPM.4, upper panel).

[6.1, 6.2, 6.3, TS.3.1, Box TS.6]

Mitigation scenarios in which it is likely that the temperature change caused by anthropogenic GHG emis-

sions can be kept to less than 2 °C relative to pre-industrial levels are characterized by atmospheric concen-

trations in 2100 of about 450 ppm CO

2

eq (high confidence). Mitigation scenarios reaching concentration levels of

about 500 ppm CO

2

eq by 2100 are more likely than not to limit temperature change to less than 2 °C relative to

pre-industrial levels, unless they temporarily ‘overshoot’ concentration levels of roughly 530 ppm CO

2

eq before 2100, in

which case they are about as likely as not to achieve that goal.

15

Scenarios that reach 530 to 650 ppm CO

2

eq concentra-

tions by 2100 are more unlikely than likely to keep temperature change below 2 °C relative to pre-industrial levels.

Scenarios that exceed about 650 ppm CO

2

eq by 2100 are unlikely to limit temperature change to below 2 °C relative to

pre-industrial levels. Mitigation scenarios in which temperature increase is more likely than not to be less than 1.5 °C

relative to pre-industrial levels by 2100 are characterized by concentrations in 2100 of below 430 ppm CO

2

eq. Tempera-

ture peaks during the century and then declines in these scenarios. Probability statements regarding other levels of

temperature change can be made with reference to Table SPM.1. [6.3, Box TS.6]

Scenarios reaching atmospheric concentration levels of about 450 ppm CO

2

eq by 2100 (consistent with a

likely chance to keep temperature change below 2 °C relative to pre-industrial levels) include substantial cuts

in anthropogenic GHG emissions by mid-century through large-scale changes in energy systems and poten-

tially land use (high confidence). Scenarios reaching these concentrations by 2100 are characterized by lower global

GHG emissions in 2050 than in 2010, 40 % to 70 % lower globally,

16

and emissions levels near zero GtCO

2

eq or below in

14

The long-term scenarios assessed in WGIII were generated primarily by large-scale, integrated models that project many key characteristics of

mitigation pathways to mid-century and beyond. These models link many important human systems (e. g., energy, agriculture and land use,

economy) with physical processes associated with climate change (e. g., the carbon cycle). The models approximate cost-effective solutions that

minimize the aggregate economic costs of achieving mitigation outcomes, unless they are specifically constrained to behave otherwise. They are

simplified, stylized representations of highly-complex, real-world processes, and the scenarios they produce are based on uncertain projections

about key events and drivers over often century-long timescales. Simplifications and differences in assumptions are the reason why output gen-

erated from different models, or versions of the same model, can differ, and projections from all models can differ considerably from the reality

that unfolds. [Box TS.7, 6.2]

15

Mitigation scenarios, including those reaching 2100 concentrations as high as or higher than about 550 ppm CO

2

eq, can temporarily ‘overshoot’

atmospheric CO

2

eq concentration levels before descending to lower levels later. Such concentration overshoot involves less mitigation in the near

term with more rapid and deeper emissions reductions in the long run. Overshoot increases the probability of exceeding any given temperature

goal. [6.3, Table SPM.1]

16

This range differs from the range provided for a similar concentration category in AR4 (50 % – 85 % lower than 2000 for CO

2

only). Reasons for

this difference include that this report has assessed a substantially larger number of scenarios than in AR4 and looks at all GHGs. In addition, a

large proportion of the new scenarios include Carbon Dioxide Removal (CDR) technologies (see below). Other factors include the use of 2100

concentration levels instead of stabilization levels and the shift in reference year from 2000 to 2010. Scenarios with higher emissions in 2050 are

characterized by a greater reliance on CDR technologies beyond mid-century.

SPM.4

SPM.4.1

Figure SPM.4 | Pathways of global GHG emissions (GtCO

2

eq / yr) in baseline and mitigation scenarios for different long-term concentration levels (upper panel) [Figure 6.7] and

associated upscaling requirements of low-carbon energy (% of primary energy) for 2030, 2050 and 2100 compared to 2010 levels in mitigation scenarios (lower panel) [Figure

7.16]. The lower panel excludes scenarios with limited technology availability and exogenous carbon price trajectories. For definitions of CO

2

-equivalent emissions and CO

2

-equiva-

lent concentrations see the WGIII

AR5

Glossary.

21002000 2020 2040 2060 2080 2100

-20

0

20

40

60

80

100

120

140

Baseline

RCP8.5

RCP6.0

RCP4.5

RCP2.6

Associated Upscaling of Low-Carbon Energy Supply

0

20

40

60

80

100

2030 2050 2100 2030 2050 2100 2030 2050 2100 2030 2050 2100

Low-Carbon Energy Share of Primary Energy [%]

Annual GHG Emissions [GtCO

2

eq/yr]

> 1000

720 - 1000

580 - 720

530 - 580

480 - 530

430 - 480

Full AR5 Database Range

ppm CO

2

eq

ppm CO

2

eq

ppm CO

2

eq

ppm CO

2

eq

ppm CO

2

eq

ppm CO

2

eq

GHG Emission Pathways 2000-2100: All AR5 Scenarios

90

th

Percentile

Median

10

th

Percentile

580 - 720

530 - 580

480 - 530

430 - 480

ppm CO

2

eq

ppm CO

2

eq

ppm CO

2

eq

ppm CO

2

eq

Min

75

th

Max

Median

25

th

Percentile

+180%

+185%

+275%

+310%

+95%

+135%

+135%

+145%

2010

11

SPM

Summary for Policymakers

Mitigation pathways and measures in the context

of sustainable development

Long-term mitigation pathways

There are multiple scenarios with a range of technological and behavioral options, with different characteristics

and implications for sustainable development, that are consistent with different levels of mitigation. For this

assessment, about 900 mitigation scenarios have been collected in a database based on published integrated models.

14

This

range spans atmospheric concentration levels in 2100 from 430 ppm CO

2

eq to above 720 ppm CO

2

eq, which is comparable

to the 2100 forcing levels between RCP 2.6 and RCP 6.0. Scenarios outside this range were also assessed including some

scenarios with concentrations in 2100 below 430 ppm CO

2

eq (for a discussion of these scenarios see below). The mitigation

scenarios involve a wide range of technological, socioeconomic, and institutional trajectories, but uncertainties and model

limitations exist and developments outside this range are possible (Figure SPM.4, upper panel).

[6.1, 6.2, 6.3, TS.3.1, Box TS.6]

Mitigation scenarios in which it is likely that the temperature change caused by anthropogenic GHG emis-

sions can be kept to less than 2 °C relative to pre-industrial levels are characterized by atmospheric concen-

trations in 2100 of about 450 ppm CO

2

eq (high confidence). Mitigation scenarios reaching concentration levels of

about 500 ppm CO

2

eq by 2100 are more likely than not to limit temperature change to less than 2 °C relative to

pre-industrial levels, unless they temporarily ‘overshoot’ concentration levels of roughly 530 ppm CO

2

eq before 2100, in

which case they are about as likely as not to achieve that goal.

15

Scenarios that reach 530 to 650 ppm CO

2

eq concentra-

tions by 2100 are more unlikely than likely to keep temperature change below 2 °C relative to pre-industrial levels.

Scenarios that exceed about 650 ppm CO

2

eq by 2100 are unlikely to limit temperature change to below 2 °C relative to

pre-industrial levels. Mitigation scenarios in which temperature increase is more likely than not to be less than 1.5 °C

relative to pre-industrial levels by 2100 are characterized by concentrations in 2100 of below 430 ppm CO

2

eq. Tempera-

ture peaks during the century and then declines in these scenarios. Probability statements regarding other levels of

temperature change can be made with reference to Table SPM.1. [6.3, Box TS.6]

Scenarios reaching atmospheric concentration levels of about 450 ppm CO

2

eq by 2100 (consistent with a

likely chance to keep temperature change below 2 °C relative to pre-industrial levels) include substantial cuts

in anthropogenic GHG emissions by mid-century through large-scale changes in energy systems and poten-

tially land use (high confidence). Scenarios reaching these concentrations by 2100 are characterized by lower global

GHG emissions in 2050 than in 2010, 40 % to 70 % lower globally,

16

and emissions levels near zero GtCO

2

eq or below in

14

The long-term scenarios assessed in WGIII were generated primarily by large-scale, integrated models that project many key characteristics of

mitigation pathways to mid-century and beyond. These models link many important human systems (e. g., energy, agriculture and land use,

economy) with physical processes associated with climate change (e. g., the carbon cycle). The models approximate cost-effective solutions that

minimize the aggregate economic costs of achieving mitigation outcomes, unless they are specifically constrained to behave otherwise. They are

simplified, stylized representations of highly-complex, real-world processes, and the scenarios they produce are based on uncertain projections

about key events and drivers over often century-long timescales. Simplifications and differences in assumptions are the reason why output gen-

erated from different models, or versions of the same model, can differ, and projections from all models can differ considerably from the reality

that unfolds. [Box TS.7, 6.2]

15

Mitigation scenarios, including those reaching 2100 concentrations as high as or higher than about 550 ppm CO

2

eq, can temporarily ‘overshoot’

atmospheric CO

2

eq concentration levels before descending to lower levels later. Such concentration overshoot involves less mitigation in the near

term with more rapid and deeper emissions reductions in the long run. Overshoot increases the probability of exceeding any given temperature

goal. [6.3, Table SPM.1]

16

This range differs from the range provided for a similar concentration category in AR4 (50 % – 85 % lower than 2000 for CO

2

only). Reasons for

this difference include that this report has assessed a substantially larger number of scenarios than in AR4 and looks at all GHGs. In addition, a

large proportion of the new scenarios include Carbon Dioxide Removal (CDR) technologies (see below). Other factors include the use of 2100

concentration levels instead of stabilization levels and the shift in reference year from 2000 to 2010. Scenarios with higher emissions in 2050 are

characterized by a greater reliance on CDR technologies beyond mid-century.

SPM.4

SPM.4.1

Figure SPM.4 | Pathways of global GHG emissions (GtCO

2

eq / yr) in baseline and mitigation scenarios for different long-term concentration levels (upper panel) [Figure 6.7] and

associated upscaling requirements of low-carbon energy (% of primary energy) for 2030, 2050 and 2100 compared to 2010 levels in mitigation scenarios (lower panel) [Figure

7.16]. The lower panel excludes scenarios with limited technology availability and exogenous carbon price trajectories. For definitions of CO

2

-equivalent emissions and CO

2

-equiva-

lent concentrations see the WGIII

AR5

Glossary.

21002000 2020 2040 2060 2080 2100

-20

0

20

40

60

80

100

120

140

Baseline

RCP8.5

RCP6.0

RCP4.5

RCP2.6

Associated Upscaling of Low-Carbon Energy Supply

0

20

40

60

80

100

2030 2050 2100 2030 2050 2100 2030 2050 2100 2030 2050 2100

Low-Carbon Energy Share of Primary Energy [%]

Annual GHG Emissions [GtCO

2

eq/yr]

> 1000

720 - 1000

580 - 720

530 - 580

480 - 530

430 - 480

Full AR5 Database Range

ppm CO

2

eq

ppm CO

2

eq

ppm CO

2

eq

ppm CO

2

eq

ppm CO

2

eq

ppm CO

2

eq

GHG Emission Pathways 2000-2100: All AR5 Scenarios

90

th

Percentile

Median

10

th

Percentile

580 - 720

530 - 580

480 - 530

430 - 480

ppm CO

2

eq

ppm CO

2

eq

ppm CO

2

eq

ppm CO

2

eq

Min

75

th

Max

Median

25

th

Percentile

+180%

+185%

+275%

+310%

+95%

+135%

+135%

+145%

2010

12

SPM

Summary for Policymakers

2100. In scenarios reaching about 500 ppm CO

2

eq by 2100, 2050 emissions levels are 25 % to 55 % lower than in 2010

globally. In scenarios reaching about 550 ppm CO

2

eq, emissions in 2050 are from 5 % above 2010 levels to 45 % below

2010 levels globally (Table SPM.1). At the global level, scenarios reaching about 450 ppm CO

2

eq are also characterized

by more rapid improvements in energy efficiency and a tripling to nearly a quadrupling of the share of zero- and low-

carbon energy supply from renewables, nuclear energy and fossil energy with carbon dioxide capture and storage (CCS),

or bioenergy with CCS (BECCS) by the year 2050 (Figure SPM.4, lower panel). These scenarios describe a wide range of

changes in land use, reflecting different assumptions about the scale of bioenergy production, afforestation, and reduced

deforestation. All of these emissions, energy, and land-use changes vary across regions.

17

Scenarios reaching higher

concentrations include similar changes, but on a slower timescale. On the other hand, scenarios reaching lower concen-

trations require these changes on a faster timescale. [6.3, 7.11]

Mitigation scenarios reaching about 450 ppm CO

2

eq in 2100 typically involve temporary overshoot of

atmospheric concentrations, as do many scenarios reaching about 500 ppm to about 550 ppm CO

2

eq in 2100.

Depending on the level of the overshoot, overshoot scenarios typically rely on the availability and wide-

spread deployment of BECCS and afforestation in the second half of the century. The availability and scale of

these and other Carbon Dioxide Removal (CDR) technologies and methods are uncertain and CDR technolo-

gies and methods are, to varying degrees, associated with challenges and risks (high confidence) (see Section

SPM.4.2).

18

CDR is also prevalent in many scenarios without overshoot to compensate for residual emissions from sectors

where mitigation is more expensive. There is uncertainty about the potential for large-scale deployment of BECCS, large-

scale afforestation, and other CDR technologies and methods. [2.6, 6.3, 6.9.1, Figure 6.7, 7.11, 11.13]

Estimated global GHG emissions levels in 2020 based on the Cancún Pledges are not consistent with cost-

effective long-term mitigation trajectories that are at least about as likely as not to limit temperature

change to 2 °C relative to pre-industrial levels (2100 concentrations of about 450 to about 500 ppm CO

2

eq),

but they do not preclude the option to meet that goal (high confidence). Meeting this goal would require further

substantial reductions beyond 2020. The Cancún Pledges are broadly consistent with cost-effective scenarios that are

likely to keep temperature change below 3 °C relative to preindustrial levels. [6.4, 13.13, Figure TS.11]

Delaying mitigation efforts beyond those in place today through 2030 is estimated to substantially increase

the difficulty of the transition to low longer-term emissions levels and narrow the range of options consis-

tent with maintaining temperature change below 2 °C relative to pre-industrial levels (high confidence). Cost-

effective mitigation scenarios that make it at least about as likely as not that temperature change will remain below 2 °C

relative to pre-industrial levels (2100 concentrations of about 450 to about 500 ppm CO

2

eq) are typically characterized

by annual GHG emissions in 2030 of roughly between 30 GtCO

2

eq and 50 GtCO

2

eq (Figure SPM.5, left panel). Scenarios

with annual GHG emissions above 55 GtCO

2

eq in 2030 are characterized by substantially higher rates of emissions

reductions from 2030 to 2050 (Figure SPM.5, middle panel); much more rapid scale-up of low-carbon energy over this

period (FigureSPM.5, right panel); a larger reliance on CDR technologies in the long-term; and higher transitional and

long-term economic impacts (Table SPM.2, orange segment). Due to these increased mitigation challenges, many models

with annual 2030 GHG emissions higher than 55 GtCO

2

eq could not produce scenarios reaching atmospheric concentra-

tion levels that make it about as likely as not that temperature change will remain below 2 °C relative to pre-industrial

levels. [6.4, 7.11, Figures TS.11, TS.13]

17

At the national level, change is considered most effective when it reflects country and local visions and approaches to achieving sustainable

development according to national circumstances and priorities. [6.4, 11.8.4, WGII SPM]

18

According to WGI, CDR methods have biogeochemical and technological limitations to their potential on the global scale. There is insufficient

knowledge to quantify how much CO

2

emissions could be partially offset by CDR on a century timescale. CDR methods carry side-effects and

long-term consequences on a global scale. [WGI SPM.E.8]

13

SPM

Summary for Policymakers

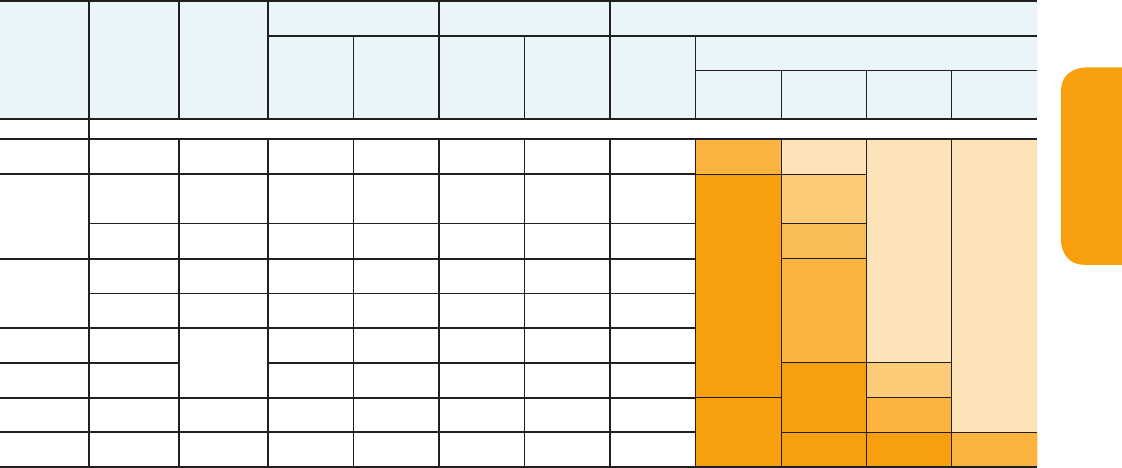

Table SPM.1 | Key characteristics of the scenarios collected and assessed for WGIII AR5. For all parameters, the 10th to 90th percentile of the scenarios is shown.

1, 2

[Table 6.3]

CO

2

eq

Concentrations

in 2100 [ppm

CO

2

eq]

Category label

(concentration

range)

9

Subcategories

Relative

position of

the RCPs

5

Cumulative CO

2

emissions

3

[GtCO

2

]

Change in CO

2

eq emissions

compared to 2010 in [%]

4

Temperature change (relative to 1850 – 1900)

5, 6

2011 – 2050 2011 – 2100 2050 2100

2100

Temperature

change [°C]

7

Likelihood of staying below temperature

level over the 21st century

8

1.5 °C 2.0 °C 3.0 °C 4.0 °C

< 430 Only a limited number of individual model studies have explored levels below 430 ppm CO

2

eq

450

(430 – 480)

Total range

1, 10

RCP2.6 550 – 1300 630 – 1180 − 72 to − 41 − 118 to − 78

1.5 – 1.7

(1.0 – 2.8)

More unlikely

than likely

Likely

Likely

Likely

500

(480 – 530)

No overshoot of

530 ppm CO

2

eq

860 – 1180 960 – 1430 − 57 to − 42 − 107 to − 73

1.7 – 1.9

(1.2 – 2.9)

Unlikely

More likely

than not

Overshoot of

530 ppm CO

2

eq

1130 – 1530 990 – 1550 − 55 to − 25 − 114 to − 90

1.8 – 2.0

(1.2 – 3.3)

About as

likely as not

550

(530 – 580)

No overshoot of

580 ppm CO

2

eq

1070 – 1460 1240 – 2240 − 47 to − 19 − 81 to − 59

2.0 – 2.2

(1.4 – 3.6)

More unlikely

than likely

12

Overshoot of

580 ppm CO

2

eq

1420 – 1750 1170 – 2100 − 16 to 7 − 183 to − 86

2.1 – 2.3

(1.4 – 3.6)

(580 – 650) Total range

RCP4.5

1260 – 1640 1870 – 2440 − 38 to 24 − 134 to − 50

2.3 – 2.6

(1.5 – 4.2)

(650 – 720) Total range 1310 – 1750 2570 – 3340 − 11 to 17 − 54 to − 21

2.6 – 2.9

(1.8 – 4.5)

Unlikely

More likely

than not

(720 – 1000) Total range RCP6.0 1570 – 1940 3620 – 4990 18 to 54 − 7 to 72

3.1 – 3.7

(2.1 – 5.8)

Unlikely

11

More unlikely

than likely

> 1000 Total range RCP8.5 1840 – 2310 5350 – 7010 52 to 95 74 to 178

4.1 – 4.8

(2.8 – 7.8)

Unlikely

11

Unlikely

More unlikely

than likely

1

The ‘total range’ for the 430 – 480 ppm CO

2

eq scenarios corresponds to the range of the 10th – 90th percentile of the subcategory of these scenarios shown in Table 6.3.

2

Baseline scenarios (see SPM.3) fall into the > 1000 and 720 – 1000 ppm CO

2

eq categories. The latter category also includes mitigation scenarios. The baseline scenarios in the latter

category reach a temperature change of 2.5 – 5.8 °C above preindustrial in 2100. Together with the baseline scenarios in the > 1000 ppm CO

2

eq category, this leads to an overall 2100

temperature range of 2.5 – 7.8 °C (range based on median climate response: 3.7 – 4.8 °C) for baseline scenarios across both concentration categories.

3

For comparison of the cumulative CO

2

emissions estimates assessed here with those presented in WGI, an amount of 515 [445 – 585] GtC (1890 [1630 – 2150] GtCO

2

), was

already emitted by 2011 since 1870 [Section WGI 12.5]. Note that cumulative emissions are presented here for different periods of time (2011 – 2050 and 2011 – 2100) while

cumulative emissions in WGI are presented as total compatible emissions for the RCPs (2012 – 2100) or for total compatible emissions for remaining below a given tempera-

ture target with a given likelihood [WGI Table SPM.3, WGI SPM.E.8].

4

The global 2010 emissions are 31 % above the 1990 emissions (consistent with the historic GHG emission estimates presented in this report). CO

2

eq emissions include the

basket of Kyoto gases (CO

2

, CH

4

, N

2

O as well as F-gases).

5

The assessment in WGIII involves a large number of scenarios published in the scientific literature and is thus not limited to the RCPs. To evaluate the CO

2

eq concentration

and climate implications of these scenarios, the MAGICC model was used in a probabilistic mode (see AnnexII). For a comparison between MAGICC model results and

the outcomes of the models used in WGI, see Sections WGI 12.4.1.2 and WGI 12.4.8 and 6.3.2.6. Reasons for differences with WGI SPM Table.2 include the difference in

reference year (1986 – 2005 vs. 1850 – 1900 here), difference in reporting year (2081 – 2100 vs 2100 here), set-up of simulation (CMIP5 concentration driven versus MAGICC

emission-driven here), and the wider set of scenarios (RCPs versus the full set of scenarios in the WGIII AR5 scenario database here).

6

Temperature change is reported for the year 2100, which is not directly comparable to the equilibrium warming reported in WGIII AR4 [Table 3.5, Chapter 3]. For the 2100

temperature estimates, the transient climate response (TCR) is the most relevant system property. The assumed 90 % range of the TCR for MAGICC is 1.2 – 2.6 °C (median

1.8 °C). This compares to the 90 % range of TCR between 1.2 – 2.4 °C for CMIP5 [WGI 9.7] and an assessed likely range of 1 – 2.5 °C from multiple lines of evidence reported

in the WGI AR5 [Box 12.2 in Section 12.5].

7

Temperature change in 2100 is provided for a median estimate of the MAGICC calculations, which illustrates differences between the emissions pathways of the scenarios

in each category. The range of temperature change in the parentheses includes in addition the carbon cycle and climate system uncertainties as represented by the MAGICC

model [see 6.3.2.6 for further details]. The temperature data compared to the 1850 – 1900 reference year was calculated by taking all projected warming relative to

1986 – 2005, and adding 0.61 °C for 1986 – 2005 compared to 1850 – 1900, based on HadCRUT4 [see WGI Table SPM.2].

8

The assessment in this table is based on the probabilities calculated for the full ensemble of scenarios in WGIII using MAGICC and the assessment in WGI of the uncertainty

of the temperature projections not covered by climate models. The statements are therefore consistent with the statements in WGI, which are based on the CMIP5 runs of the

RCPs and the assessed uncertainties. Hence, the likelihood statements reflect different lines of evidence from both WGs. This WGI method was also applied for scenarios with

intermediate concentration levels where no CMIP5 runs are available. The likelihood statements are indicative only [6.3], and follow broadly the terms used by the WGI SPM

for temperature projections: likely 66 – 100 %, more likely than not > 50 – 100 %, about as likely as not 33 – 66 %, and unlikely 0 – 33 %. In addition the term more unlikely

than likely 0–< 50 % is used.

9

The CO

2

-equivalent concentration includes the forcing of all GHGs including halogenated gases and tropospheric ozone, as well as aerosols and albedo change (calculated on

the basis of the total forcing from a simple carbon cycle / climate model, MAGICC).

10

T he vast majority of scenarios in this category overshoot the category boundary of 480 ppm CO

2

eq concentrations.

11

For scenarios in this category no CMIP5 run [WGI Chapter 12, Table 12.3] as well as no MAGICC realization [6.3] stays below the respective temperature level. Still, an

unlikely assignment is given to reflect uncertainties that might not be reflected by the current climate models.

12

Scenarios in the 580 – 650 ppm CO

2

eq category include both overshoot scenarios and scenarios that do not exceed the concentration level at the high end of the category

(like RCP4.5). The latter type of scenarios, in general, have an assessed probability of more unlikely than likely to stay below the 2 °C temperature level, while the former are

mostly assessed to have an unlikely probability of staying below this level.

14

SPM

Summary for Policymakers

Estimates of the aggregate economic costs of mitigation vary widely and are highly sensitive to model design

and assumptions as well as the specification of scenarios, including the characterization of technologies and

the timing of mitigation (high confidence). Scenarios in which all countries of the world begin mitigation immediately,

there is a single global carbon price, and all key technologies are available, have been used as a cost-effective benchmark

for estimating macroeconomic mitigation costs (Table SPM.2, yellow segments). Under these assumptions, mitigation

scenarios that reach atmospheric concentrations of about 450 ppm CO

2

eq by 2100 entail losses in global consumption—

not including benefits of reduced climate change as well as co-benefits and adverse side-effects of mitigation

19

—of 1 % to

4 % (median: 1.7 %) in 2030, 2 % to 6 % (median: 3.4 %) in 2050, and 3 % to 11 % (median: 4.8 %) in 2100 relative to

consumption in baseline scenarios that grows anywhere from 300 % to more than 900 % over the century. These numbers

19

The total economic effect at different temperature levels would include mitigation costs, co-benefits of mitigation, adverse side-effects of mitiga-

tion, adaptation costs and climate damages. Mitigation cost and climate damage estimates at any given temperature level cannot be compared

to evaluate the costs and benefits of mitigation. Rather, the consideration of economic costs and benefits of mitigation should include the reduc-

tion of climate damages relative to the case of unabated climate change.

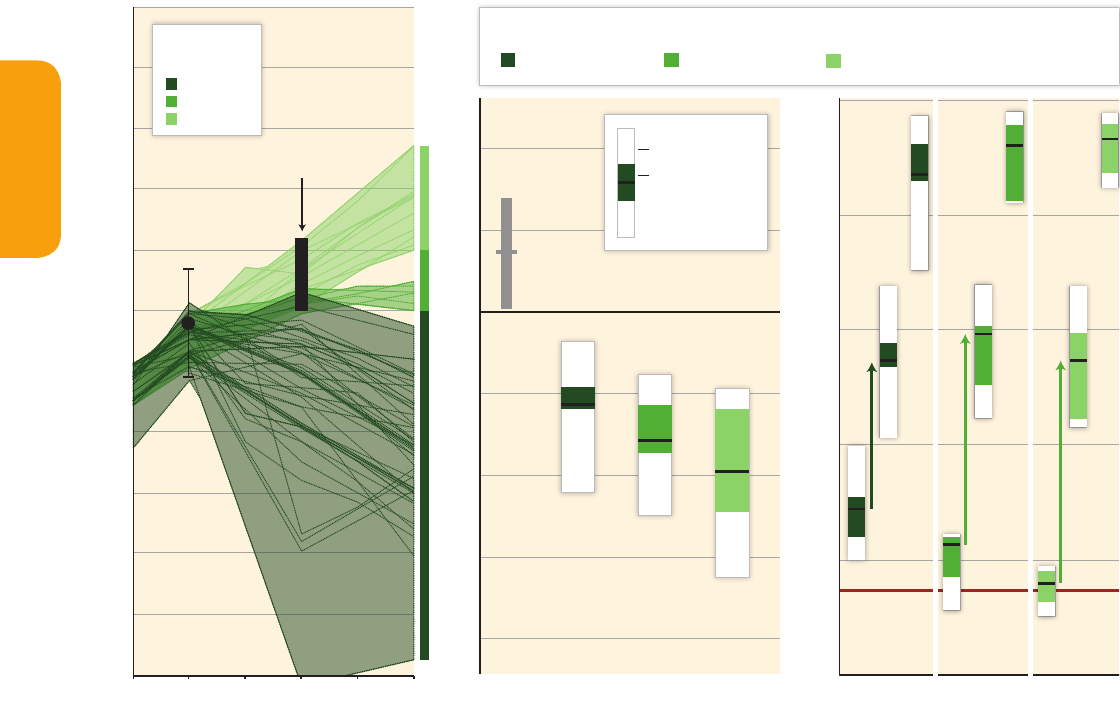

Figure SPM.5 | The implications of different 2030 GHG emissions levels (left panel) for the rate of CO

2

emissions reductions from 2030 to 2050 (middle panel) and low-carbon

energy upscaling from 2030 to 2050 and 2100 (right panel) in mitigation scenarios reaching about 450 to about 500 (430 – 530) ppm CO

2

eq concentrations by 2100. The scenarios

are grouped according to different emissions levels by 2030 (coloured in different shades of green). The left panel shows the pathways of GHG emissions (GtCO

2

eq / yr) leading to

these 2030 levels. The black bar shows the estimated uncertainty range of GHG emissions implied by the Cancún Pledges. The middle panel denotes the average annual CO

2

emis-

sions reduction rates for the period 2030 – 2050. It compares the median and interquartile range across scenarios from recent intermodel comparisons with explicit 2030 interim

goals to the range of scenarios in the Scenario Database for WGIII AR5. Annual rates of historical emissions change between 1900 – 2010 (sustained over a period of 20 years) and

average annual emissions change between 2000 – 2010 are shown in grey. The arrows in the right panel show the magnitude of zero and low-carbon energy supply up-scaling

from 2030 to 2050 subject to different 2030 GHG emissions levels. Zero- and low-carbon energy supply includes renewables, nuclear energy, fossil energy with carbon dioxide cap-

ture and storage (CCS), and bioenergy with CCS (BECCS). Note: Only scenarios that apply the full, unconstrained mitigation technology portfolio of the underlying models (default

technology assumption) are shown. Scenarios with large net negative global emissions (> 20 GtCO

2

/ yr), scenarios with exogenous carbon price assumptions, and scenarios with

2010 emissions significantly outside the historical range are excluded. The right-hand panel includes only 68 scenarios, because three of the 71 scenarios shown in the figure do not

report some subcategories for primary energy that are required to calculate the share of zero- and low-carbon energy. [Figures 6.32 and 7.16; 13.13.1.3]

+90%

+160%

+240%

2010

0

20

40

60

80

100

2030 2050 2100 2030 2050 2100 2030 2050

2100

Implications of Different 2030 GHG

Emissions Levels for Low-Carbon Energy

Upscaling

Zero- and Low-Carbon Energy Share of Primary Energy [%]

GHG Emissions Pathways to 2030 Implications of Different 2030 GHG Emissions

Levels for the Rate of Annual Average CO

2

Emissions Reductions from 2030 to 2050

Annual Rate of Change in CO

2

Emissions (2030 – 2050) [%/yr]

-12

-9

-6

-3

0

3

6

History

1900 – 2010

2000 – 2010

AR5 Scenario Range

Interquartile Range

and Median of Model

Comparisons with

2030 Targets

Annual GHG Emissions [GtCO

2

eq/yr]

<50 GtCO

2

eq

Annual GHG Emissions in 2030

50 – 5 5 GtCO

2

eq

>55 GtCO

2

eq

n=68n=71

Cancún

Pledges

<50 GtCO

2

eq

Annual

GHG Emissions

in 2030

50 – 55 GtCO

2

eq

>55 GtCO

2

eq

2005 2010 2015 2020 2025 2030

20

25

30

35

40

45

50

55

70

75

60

65

n=71

15

SPM

Summary for Policymakers

Estimates of the aggregate economic costs of mitigation vary widely and are highly sensitive to model design

and assumptions as well as the specification of scenarios, including the characterization of technologies and

the timing of mitigation (high confidence). Scenarios in which all countries of the world begin mitigation immediately,

there is a single global carbon price, and all key technologies are available, have been used as a cost-effective benchmark

for estimating macroeconomic mitigation costs (Table SPM.2, yellow segments). Under these assumptions, mitigation

scenarios that reach atmospheric concentrations of about 450 ppm CO

2

eq by 2100 entail losses in global consumption—

not including benefits of reduced climate change as well as co-benefits and adverse side-effects of mitigation

19

—of 1 % to

4 % (median: 1.7 %) in 2030, 2 % to 6 % (median: 3.4 %) in 2050, and 3 % to 11 % (median: 4.8 %) in 2100 relative to

consumption in baseline scenarios that grows anywhere from 300 % to more than 900 % over the century. These numbers

19

The total economic effect at different temperature levels would include mitigation costs, co-benefits of mitigation, adverse side-effects of mitiga-

tion, adaptation costs and climate damages. Mitigation cost and climate damage estimates at any given temperature level cannot be compared

to evaluate the costs and benefits of mitigation. Rather, the consideration of economic costs and benefits of mitigation should include the reduc-

tion of climate damages relative to the case of unabated climate change.

Figure SPM.5 | The implications of different 2030 GHG emissions levels (left panel) for the rate of CO

2

emissions reductions from 2030 to 2050 (middle panel) and low-carbon

energy upscaling from 2030 to 2050 and 2100 (right panel) in mitigation scenarios reaching about 450 to about 500 (430 – 530) ppm CO

2

eq concentrations by 2100. The scenarios

are grouped according to different emissions levels by 2030 (coloured in different shades of green). The left panel shows the pathways of GHG emissions (GtCO

2

eq / yr) leading to

these 2030 levels. The black bar shows the estimated uncertainty range of GHG emissions implied by the Cancún Pledges. The middle panel denotes the average annual CO

2

emis-

sions reduction rates for the period 2030 – 2050. It compares the median and interquartile range across scenarios from recent intermodel comparisons with explicit 2030 interim

goals to the range of scenarios in the Scenario Database for WGIII AR5. Annual rates of historical emissions change between 1900 – 2010 (sustained over a period of 20 years) and

average annual emissions change between 2000 – 2010 are shown in grey. The arrows in the right panel show the magnitude of zero and low-carbon energy supply up-scaling

from 2030 to 2050 subject to different 2030 GHG emissions levels. Zero- and low-carbon energy supply includes renewables, nuclear energy, fossil energy with carbon dioxide cap-

ture and storage (CCS), and bioenergy with CCS (BECCS). Note: Only scenarios that apply the full, unconstrained mitigation technology portfolio of the underlying models (default

technology assumption) are shown. Scenarios with large net negative global emissions (> 20 GtCO

2

/ yr), scenarios with exogenous carbon price assumptions, and scenarios with

2010 emissions significantly outside the historical range are excluded. The right-hand panel includes only 68 scenarios, because three of the 71 scenarios shown in the figure do not

report some subcategories for primary energy that are required to calculate the share of zero- and low-carbon energy. [Figures 6.32 and 7.16; 13.13.1.3]

+90%

+160%

+240%

2010

0

20

40

60

80

100

2030 2050 2100 2030 2050 2100 2030 2050 2100

Implications of Different 2030 GHG

Emissions Levels for Low-Carbon Energy

Upscaling

Zero- and Low-Carbon Energy Share of Primary Energy [%]

GHG Emissions Pathways to 2030 Implications of Different 2030 GHG Emissions

Levels for the Rate of Annual Average CO

2

Emissions Reductions from 2030 to 2050

Annual Rate of Change in CO

2

Emissions (2030 – 2050) [%/yr]

-12

-9

-6

-3

0

3

6

History

1900 – 2010

2000 – 2010

AR5 Scenario Range

Interquartile Range

and Median of Model

Comparisons with

2030 Targets

Annual GHG Emissions [GtCO

2

eq/yr]

<50 GtCO

2

eq

Annual GHG Emissions in 2030

50 – 5 5 GtCO

2

eq

>55 GtCO

2

eq

n=68n=71

Cancún

Pledges

<50 GtCO

2

eq

Annual

GHG Emissions

in 2030

50 – 55 GtCO

2

eq

>55 GtCO

2

eq

2005 2010 2015 2020 2025 2030

20

25

30

35

40

45

50

55

70

75

60

65

n=71

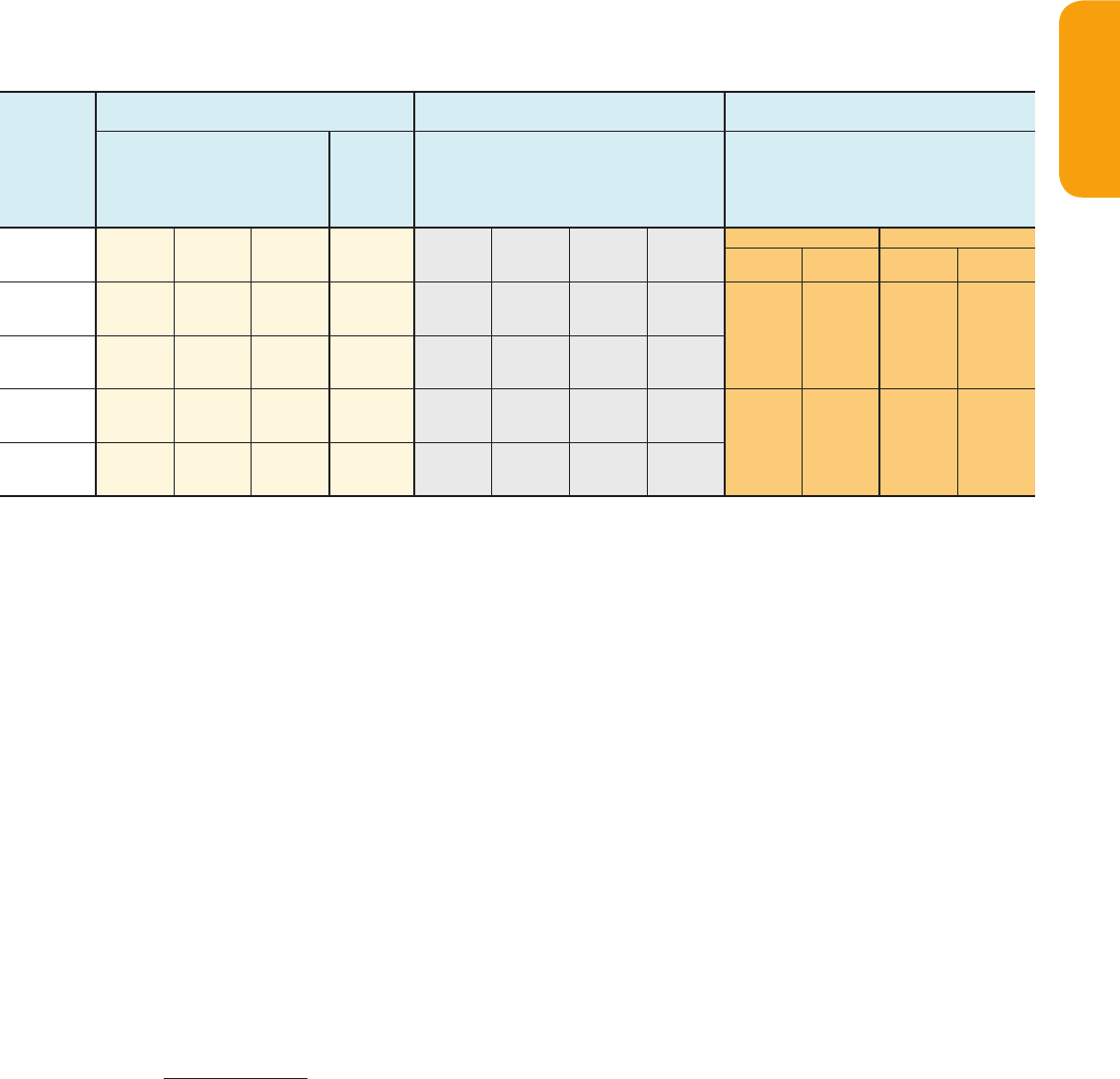

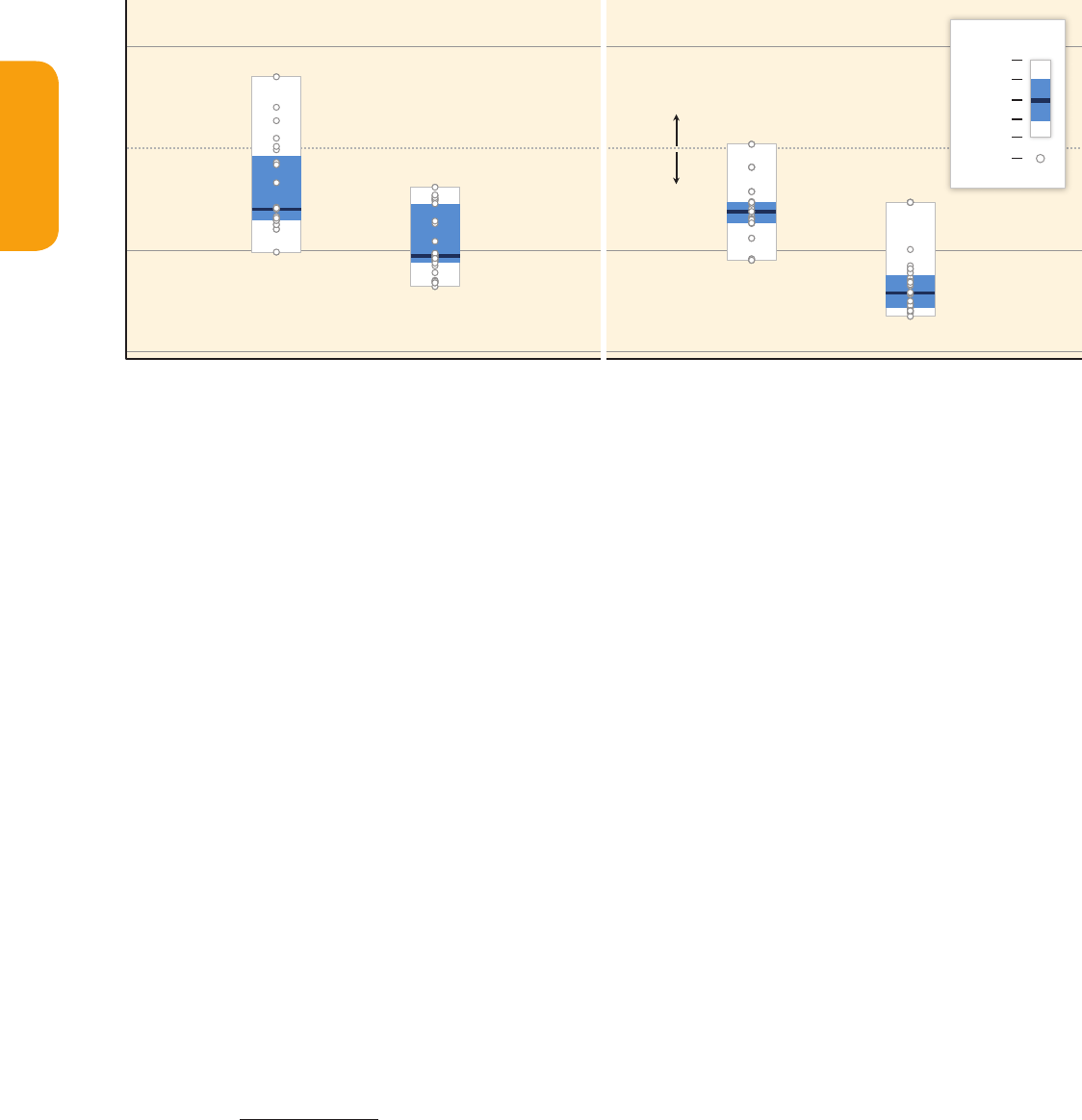

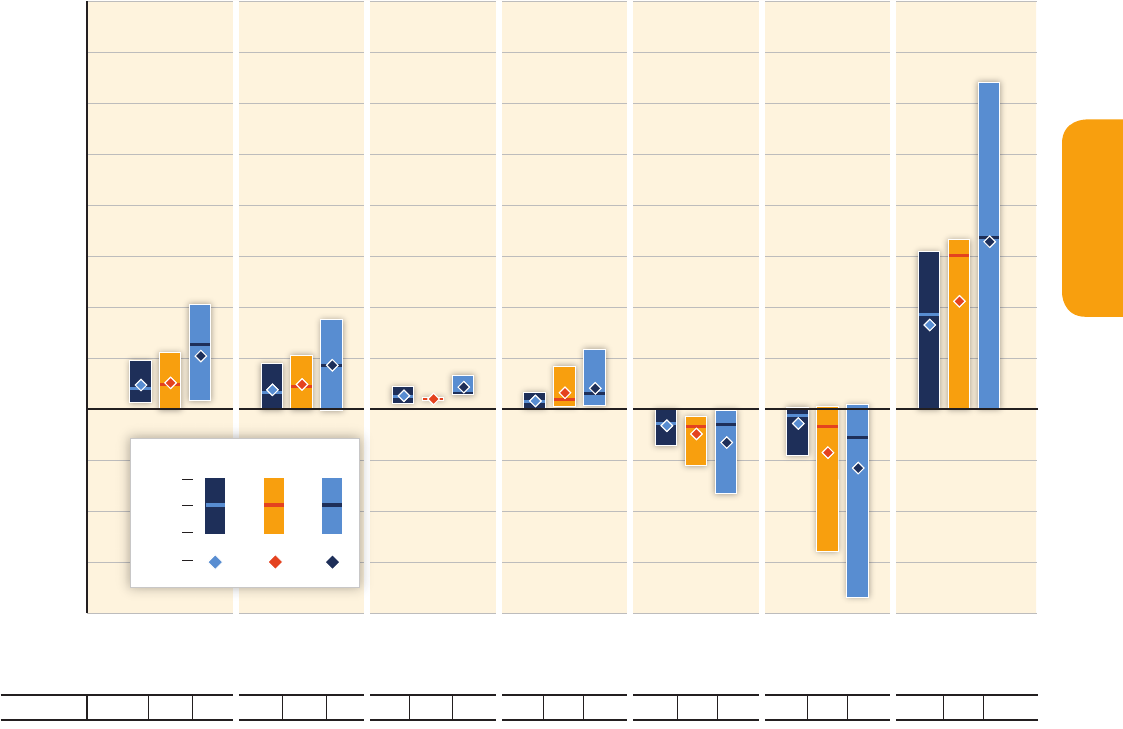

Table SPM.2 | Global mitigation costs in cost-effective scenarios

1

and estimated cost increases due to assumed limited availability of specific technologies and delayed additional

mitigation. Cost estimates shown in this table do not consider the benefits of reduced climate change as well as co-benefits and adverse side-effects of mitigation. The yellow col-

umns show consumption losses in the years 2030, 2050, and 2100 and annualized consumption growth reductions over the century in cost-effective scenarios relative to a baseline

development without climate policy. The grey columns show the percentage increase in discounted costs

2

over the century, relative to cost-effective scenarios, in scenarios in which

technology is constrained relative to default technology assumptions.

3

The orange columns show the increase in mitigation costs over the periods 2030 – 2050 and 2050 – 2100,

relative to scenarios with immediate mitigation, due to delayed additional mitigation through 2030.

4

These scenarios with delayed additional mitigation are grouped by emission

levels of less or more than 55 GtCO

2

eq in 2030, and two concentration ranges in 2100 (430 – 530 ppm CO

2

eq and 530 – 650 ppm CO

2

eq). In all figures, the median of the scenario

set is shown without parentheses, the range between the 16th and 84th percentile of the scenario set is shown in the parentheses, and the number of scenarios in the set is shown

in square brackets.

5

[Figures TS.12, TS.13, 6.21, 6.24, 6.25, Annex II.10]

Consumption losses in cost-effective scenarios

1

Increase in total discounted mitigation costs in

scenarios with limited availability of technologies

Increase in medium- and long-term mitigation costs

due to delayed additional mitigation until 2030

[% reduction in consumption

relative to baseline]