1207

16

Cross-cutting Investment

and Finance Issues

Coordinating Lead Authors:

Sujata Gupta (India / Philippines), Jochen Harnisch (Germany)

Lead Authors:

Dipal Chandra Barua (Bangladesh), Lloyd Chingambo (Zambia), Paul Frankel (USA), Raúl Jorge

Garrido Vázquez (Cuba), Luis Gómez-Echeverri (Austria / Colombia), Erik Haites (Canada), Yongfu

Huang (Finland / China), Raymond Kopp (USA), Benoit Lefèvre (France / USA), Haroldo de Oliveira

Machado-Filho (Brazil), Emanuele Massetti (Italy)

Contributing Authors:

Katrin Enting (Germany), Martin Stadelmann (Switzerland), Murray Ward (New Zealand / Canada),

Silvia Kreibiehl (Germany)

Review Editors:

Carlo Carraro (Italy), Mohammed Said Karrouk (Morocco), Ignacio Pérez-Arriaga (Spain)

Chapter Science Assistant:

Katrin Enting (Germany)

This chapter should be cited as:

Gupta S., J. Harnisch, D. C. Barua, L. Chingambo, P. Frankel, R. J. Garrido Vázquez, L. Gómez-Echeverri, E. Haites, Y. Huang,

R. Kopp, B. Lefèvre, H. Machado-Filho, and E. Massetti, 2014: Cross-cutting Investment and Finance Issues. In: Climate

Change 2014: Mitigation of Climate Change. Contribution of Working Group III to the Fifth Assessment Report of the Inter-

governmental Panel on Climate Change [Edenhofer, O., R. Pichs-Madruga, Y. Sokona, E. Farahani, S. Kadner, K. Seyboth, A.

Adler, I. Baum, S. Brunner, P. Eickemeier, B. Kriemann, J. Savolainen, S. Schlömer, C. von Stechow, T. Zwickel and J.C. Minx

(eds.)]. Cambridge University Press, Cambridge, United Kingdom and New York, NY, USA.

12081208

Cross-cutting Investment and Finance Issues

16

Chapter 16

Contents

Executive Summary � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � 1210

16�1 Introduction � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � 1211

16�2 Scale of financing at national, regional, and international level in the short-, mid-, and long-

term

� � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � 1213

16�2�1 Current financial flows and sources

� � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � 1213

16.2.1.1 Estimates of current climate finance

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1214

16.2.1.2 Current sources of climate finance

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1216

16.2.1.3 Recent developments

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1217

16�2�2 Future low-carbon investment

� � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � 1217

16.2.2.1 Investment needs

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1217

16.2.2.2 Incremental costs

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1221

16�2�3 Raising public funding by developed countries for climate finance in developing countries

� � � � � � � � � � � � 1221

16�3 Enabling environments � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � 1223

16�4 Financing low-carbon investments, opportunities, and key drivers � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � 1223

16�4�1 Capital managers and investment decisions

� � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � 1223

16�4�2 Challenges for low-carbon investment

� � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � 1224

16�4�3 Financial instruments

� � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � 1226

16.4.3.1 Reducing investment risks

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1226

16.4.3.2 Reducing cost of and facilitating access to capital

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1227

16.4.3.3 Enhancing cash flow

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1228

16�5 Institutional arrangements for mitigation financing � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � 1228

16�5�1 International arrangements

� � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � 1228

16�5�2 National and sub-national arrangements

� � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � 1229

16�5�3 Performance in a complex institutional landscape

� � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � 1230

16�6 Synergies and tradeoffs between financing mitigation and adaptation � � � � � � � � � � � � � � � � � � � � � � � � � � 1231

16�6�1 Optimal balance between mitigation and adaptation and time dimension

� � � � � � � � � � � � � � � � � � � � � � � � � � � � � � 1231

12091209

Cross-cutting Investment and Finance Issues

16

Chapter 16

16�6�2 Integrated financing approaches � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � 1232

16�7 Financing developed countries’ mitigation activities � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � 1233

16�8 Financing mitigation activities in and for developing countries including for technology deve-

lopment, transfer, and diffusion

� � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � 1234

16�9 Gaps in knowledge and data � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � 1237

16�10 Frequently Asked Questions � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � 1238

References � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � 1239

12101210

Cross-cutting Investment and Finance Issues

16

Chapter 16

Executive Summary

For the first time, an assessment report by the Intergovernmental Panel

on Climate Change (IPCC) contains a chapter dedicated to investment

and finance. These are the chapter’s key findings:

Scientific literature on investment and finance to address cli-

mate change is still very limited and knowledge gaps are sub-

stantial; there are no agreed definitions for climate investment

and climate finance� Quantitative data are limited, relate to different

concepts, and are incomplete. Accounting systems are highly imperfect.

Estimates are available for current total climate finance, total climate

finance provided to developing countries, public climate finance pro-

vided to developing countries, and climate finance under the United

Nations Framework Convention on Climate Change (UNFCCC), as well

as future incremental investment and incremental cost for mitigation

measures. Climate finance relates both to adaptation and mitigation,

while under the scope of this chapter, estimates of future investment

needs are presented only for mitigation. [Section16.1]

Total climate finance for mitigation and adaptation is estimated

at 343 to 385 billion USD (2010 / 11 / 12 USD) per year using a

mix of 2010, 2011, and 2012 data, almost evenly being invested

in developed and developing countries (medium confidence). The

figures reflect the total financial flow for the underlying investments,

not the incremental investment, i. e., the portion attributed to the emis-

sion reductions. Around 95 % of reported total climate finance is for

mitigation (medium confidence). [16.2.1.1]

The total climate finance currently flowing to developing

countries is estimated to be between 39 to 120 billion USD

per year using a mix of 2009, 2010, 2011, and 2012 data

(2009 / 2010 / 2011 / 2012 USD) (medium confidence). This range

covers public and private flows for mitigation and adaptation. Public

climate finance is estimated at 35 – 49 billion USD (2011 / 2012 USD)

(medium confidence). Most public climate finance provided to devel-

oping countries flows through bilateral and multilateral institutions,

usually as concessional loans and grants. Climate finance under the

UNFCCC is funding provided to developing countries by AnnexII Par-

ties. The climate finance reported by AnnexII Parties averaged nearly

10 billion USD per year from 2005 to 2010 (2005 – 2010 USD) (medium

confidence). Between 2010 and 2012, the ‘fast-start finance’ (FSF) pro-

vided by some developed countries amounted to over 10 billion USD

per year (2010 / 2011 / 2012 USD) (medium confidence). Estimates of

international private climate finance flowing to developing countries

range from 10 to 72 billion USD (2009 / 2010 USD) per year, including

foreign direct investment as equity and loans in the range of 10 to

37 billion USD (2010 USD and 2008 USD) per year over the period of

2008 – 2011 (medium confidence). [16.2.1.1]

Emission patterns that limit temperature increase from pre-

industrial level to no more than 2 °C require considerably differ-

ent patterns of investment� A limited number of studies have exam-

ined the investment needs to transform the economy to limit warming

to 2 °C. Information is largely restricted to energy use with global total

annual investment in the energy sector at about 1200 billion USD. In

the results for these scenarios, which are consistent to keeping carbon

dioxide equivalent (CO

2

eq) concentration in the interval 430 – 530 ppm

until 2100, annual investment in fossil-fired power plants without car-

bon dioxide capture and storage (CCS) would decline by 30 (median:

– 20 % compared to 2010) (2 to 166) billion USD during the period

2010 – 2029, compared to the reference scenarios (limited evidence,

medium agreement). Investment in low-emissions generation tech-

nologies (renewable, nuclear, and electricity generation with CCS)

would increase by 147 (median: +100 % compared to 2010) (31 to

360) billion USD per year during the same period (limited evidence,

medium agreement) in combination with an increase by 336 (1 to 641)

billion USD in energy-efficiency investments in the building, trans-

port, and industry sector (limited evidence, medium agreement), fre-

quently involving modernization of existing equipment. Higher energy

efficiency and the shift to low-emission energy sources contribute to

a reduction in the demand for fossil fuels, thus causing a decline in

investment in fossil fuel extraction, transformation, and transportation.

Scenarios suggest that the average annual reduction of investment in

fossil fuel extraction in 2010 – 2029 would be 116 (– 8 to 369) billion

USD (limited evidence, medium agreement). Such ‘spillover’ effects

could yield adverse effects on economies, especially of countries that

rely heavily on exports of fossil fuels. Model results suggest that defor-

estation could be reduced against current deforestation trends by 50 %

with an investment of 21 to 35 billion USD per year (low confidence).

Information on investment needs in other sectors in addition to energy

efficiency, e. g., to abate process or non-CO

2

emissions is virtually

unavailable. [16.2.2]

Resources to address climate change need to be scaled up con-

siderably over the next few decades both in developed and

developing countries (medium evidence, high agreement). Increased

financial support by developed countries for mitigation (and adapta-

tion) measures in developing countries will be needed to stimulate the

increased investment. Developed countries have committed to a goal

of jointly mobilizing 100 billion USD per year by 2020 in the context

of meaningful mitigation action and transparency on implementation.

The funding could come from a variety of sources — public and private,

bilateral and multilateral, including alternative sources of finance.

Studies of how 100 billion USD per year could be mobilized by 2020

conclude that it is challenging but feasible. [16.2]

Public revenues can be raised by collecting carbon taxes and

by auctioning carbon allowances (high confidence). Putting a

price on greenhouse gas (GHG) emissions, through a carbon tax or

emissions trading, alters the rate of return on high- and low-carbon

investments. It makes low-emission technologies attract more invest-

ment and at the same time it raises a considerable amount of revenue

that can be used for a variety of purposes, including climate finance.

These carbon-related sources are already sizeable in some countries

12111211

Cross-cutting Investment and Finance Issues

16

Chapter 16

[16.2.1.2]. The consideration of alternative sources of public revenue

like taxes on international bunker fuels has the potential to generate

significant funds but is still in its infancy. Reducing fossil fuel subsi-

dies would lower emissions and release public funds for other pur-

poses [16.2.3].

Within appropriate enabling environments, the private sec-

tor, along with the public sector, can play an important role in

financing mitigation (medium evidence, high agreement). Its con-

tribution is estimated at 267 billion USD per year in 2010 and 2011

(2010 / 2011 USD) and at 224 billion USD (2011 / 2012 USD) per year

in 2011 and 2012 on average, which represents around 74 % and

62 % of overall climate finance, respectively (limited evidence, medium

agreement) [16.2.1]. In a range of countries, a large share of private

sector climate investment relies on low-interest and long-term loans

as well as risk guarantees provided by public sector institutions to

cover the incremental costs and risks of many mitigation investments.

In many countries, therefore, the role of the public sector is crucial in

helping these private investments happen. The quality of a country’s

enabling environment — including the effectiveness of its institutions,

regulations and guidelines regarding the private sector, security of

property rights, credibility of policies and other factors — has a sub-

stantial impact on whether private firms invest in new technologies

and infrastructures. Those same broader factors will probably have a

big impact on whether and where investment occurs in response to

mitigation policies [16.3]. By the end of 2012, the 20 largest emitting

developed and developing countries with lower risk country grades

for private sector investments covered 70 % of global energy-related

CO

2

emissions (low confidence). This makes them attractive for inter-

national private sector investment in low-carbon technologies. In many

other countries, including most least developed countries, low-carbon

investment will often have to rely mainly on domestic sources or inter-

national public finance [16.4.2].

A main barrier to the deployment of low-carbon technolo-

gies is a low risk-adjusted rate of return on investment vis-

à-vis high-carbon alternatives often resulting in higher cost

of capital (medium evidence, high agreement). This is true in both

developed and developing countries. Dedicated financial instruments

to address these barriers exist and include inter alia credit insurance

to decrease risk, renewable energy premiums to increase return, and

concessional finance to decrease the cost of capital. Governments can

also alter the relative rates of return of low-carbon investments in

different ways and help to provide an enabling environment. [16.3,

16.4]

Appropriate governance and institutional arrangements at the

national, regional, and international level need to be in place

for efficient, effective, and sustainable financing of mitigation

measures (high confidence). They are essential to ensure that financ-

ing to mitigate and adapt to climate change responds to national

needs and priorities and that national and international activities are

linked and do not contradict each other. An enabling environment at

the national level ensures efficient implementation of funds and risk

reduction using international resources, national funds, as well as

national development and financial institutions. [16.5]

Important synergies and tradeoffs between financing mitiga-

tion and adaptation exist (medium confidence). Available estimates

show that adaptation projects get only a minor fraction of interna-

tional climate finance. Current analyses do not provide conclusive

results on the most efficient temporal distribution of funding on adap-

tation vis-à-vis mitigation. While the uncertainties about specific path-

ways and relationships remain, and although there are different con-

siderations on its optimal balance, there is a general agreement that

funding for both mitigation and adaptation is needed. Moreover, there

is an increasing interest in promoting integrated financing approaches,

addressing both adaptation and mitigation activities in different sec-

tors and at different levels. [16.6]

Increasing access to modern energy services for meeting basic

cooking and lighting needs could yield substantial improve-

ments in human welfare at relatively low cost (medium confi-

dence). Shifting the large populations that rely on traditional solid fuels

(such as unprocessed biomass, charcoal, and coal) to modern energy

systems and expanding electricity supply for basic human needs could

yield substantial improvements in human welfare for a relatively low

cost; 72 – 95 billion USD per year until 2030 to achieve nearly universal

access. [16.8]

16.1 Introduction

This is the first time an assessment report by the Intergovernmen-

tal Panel on Climate Change (IPCC) contains a chapter dedicated to

investment and finance to address climate change. This reflects the

growing awareness of the relevance of these issues for the design of

efficient and effective climate policies.

The assessment of this topic is complicated by the absence of agreed

definitions, sparse data from disparate sources, and limited peer-

reviewed literature. Equity, burden sharing, and gender consider-

ations related to climate change are discussed in other chapters, inter

alia Sections 3.3 and 4.6.2. This chapter does not include a separate

discussion of these considerations in relation to climate finance.

There is no agreed definition of climate finance (Haites, 2011; Stadel-

mann etal., 2011b; Buchner etal., 2011; Forstater and Rank, 2012).

The term ‘climate finance’ is applied both to the financial resources

devoted to addressing climate change globally and to financial flows

to developing countries to assist them in addressing climate change.

The literature includes multiple concepts within each of these broad

categories (Box 1.1). The specific mitigation and adaptation measures

whose costs qualify as ‘climate finance’ also are not agreed. The mea-

12121212

Cross-cutting Investment and Finance Issues

16

Chapter 16

Box 16�1 | Different concepts, different numbers

Different concepts of climate finance are found in the literature.

The corresponding values differ significantly.

Financial resources devoted to addressing climate change

globally:

Total climate finance includes all financial flows whose expected

effect is to reduce net GHG emissions and / or to enhance resilience

to the impacts of climate variability and the projected climate

change. This covers private and public funds, domestic and inter-

national flows, expenditures for mitigation and adaptation to cur-

rent climate variability as well as future climate change. It covers

the full value of the financial flow rather than the share associated

with the climate change benefit; e. g., the entire investment in a

wind turbine rather than the portion attributed to the emission

reductions. The estimate by Buchner etal. (2012, 2013b) of current

climate finance of 343 to 385 billion USD (2010 / 2011 / 2012 USD)

per year using a mix of 2010, 2011, and 2012 data, corresponds

roughly to this concept.

The incremental investment is the extra capital required for

the initial investment for a mitigation or adaptation project in

comparison to a reference project. For example, the investment in

wind turbines less the investment that would have been required

for the coal or natural gas-generating unit displaced. Since the

value depends on the unknown investment in a hypothetical

alternative, the incremental investment is uncertain. Incremen-

tal investment for mitigation and adaptation measures is not

regularly estimated and reported, but estimates are available

from models. It can be positive or negative. Many agriculture and

reducing emissions from deforestation and forest degradation

(REDD+) mitigation options that involve ongoing expenditures

for labour and other operating costs rather than investments are

excluded.

The incremental costs reflect the cost of capital of the incremental

investment and the change of operating and maintenance costs

for a mitigation or adaptation project in comparison to a reference

project. It can be calculated as the difference of the net present

values of the two projects. Many mitigation measures — such as

energy efficiency, renewables, and nuclear — have a higher capi-

tal cost and lower operating costs than the measures displaced.

Frequently the incremental costs are lower than the incremental

investment. Values depend on the incremental investment as well

as projected operating costs, including fossil fuel prices, and the

discount rate. Models can estimate the incremental costs of energy

supply and demand but data are not immediately available and

aggregate estimates cannot be provided. Estimates are available

for single-mitigation options (see, e. g., Chapter7).

The macroeconomic costs of mitigation policy are the reductions

of aggregate consumption or gross domestic product induced by

the reallocation of investments and expenditures induced by cli-

mate policy. These costs do not account for the benefit of reduc-

ing anthropogenic climate change and should thus be assessed

against the economic benefit of avoided climate change impacts.

Models have traditionally provided estimates of the macroeco-

nomic costs of climate policy (see Chapter 6).

Financial flows to developing countries to assist them in

addressing climate change:

The total climate finance flowing to developing countries is the

amount of the total climate finance invested in developing coun-

tries that comes from developed countries. This covers private and

public funds for mitigation and adaptation. Estimates from a few

studies suggest the current flow is between 39 and 120 billion USD

per year (2009 – 2012 USD).

Public climate finance provided to developing countries is the

finance provided by developed countries’ governments and bilat-

eral institutions as well as multilateral institutions for mitigation

and adaptation activities in developing countries. Most of the

funds provided are concessional loans and grants. Estimates sug-

gest that public climate finance flows to developing countries were

at 35 to 49 billion USD per year in 2011 and 2012 (2011 / 2012

USD).

Private climate finance flowing to developing countries is finance

and investment by private actors in / from developed countries

for activities in developing countries whose expected effect is to

reduce net GHG emissions and / or to enhance resilience to the

impacts of climate variability and the projected climate change.

Under the United Nations Framework Convention on Climate

Change (UNFCCC), climate finance is not well-defined. Annex II

Parties provide and mobilize funding for climate related activities

in developing countries. Most of the funds provided are conces-

sional loans and grants. The climate finance provided to devel-

oping countries reported by AnnexII Parties averaged nearly 10

billion USD per year from 2005 to 2010 (2005 – 2010 USD). In addi-

tion, some developed countries promised FSF amounting to over

10 billion USD per year between 2010 and 2012 (2010 / 2011 / 2012

USD).

12131213

Cross-cutting Investment and Finance Issues

16

Chapter 16

sures included vary across studies and often are determined by the

data available

1

.

The rest of the chapter is structured as follows: Section 16.2 reviews

estimates of current climate finance corresponding to the different

concepts in Box 1, projections of global incremental investment and

incremental costs for energy-related mitigation measures to 2030,

and options for raising public funds for climate finance. Enabling fac-

tors that influence the ability to efficiently generate and implement

climate finance are discussed in Section 16.3. Section 16.4 considers

opportunities and key drivers for low-carbon investments. Institutional

arrangements for mitigation finance are addressed in Section 16.5.

Synergies and tradeoffs between financing mitigation and adapta-

tion are discussed in Section 16.6. The chapter concludes with sections

devoted to financing mitigation activities in developed (Section16.7)

and developing countries (Section 16.8) and a review of important

gaps of knowledge (Section 16.9).

1

Most of the financial flow data in this chapter originate from 2010, 2011, and 2012

and were published in USD. The exchange rates used by each source to convert

other currencies to USD are not specified in the published sources. In these cases,

the published USD figure has been maintained and the base year is similar to the

year the commitment / investment / flow was announced / reported. If no base year is

indicated, as for most monetary values in Section 16.2.2, the base year is 2010.

16.2 Scale of financing at

national, regional, and

international level in the

short-, mid-, and long-term

16�2�1 Current financial flows and sources

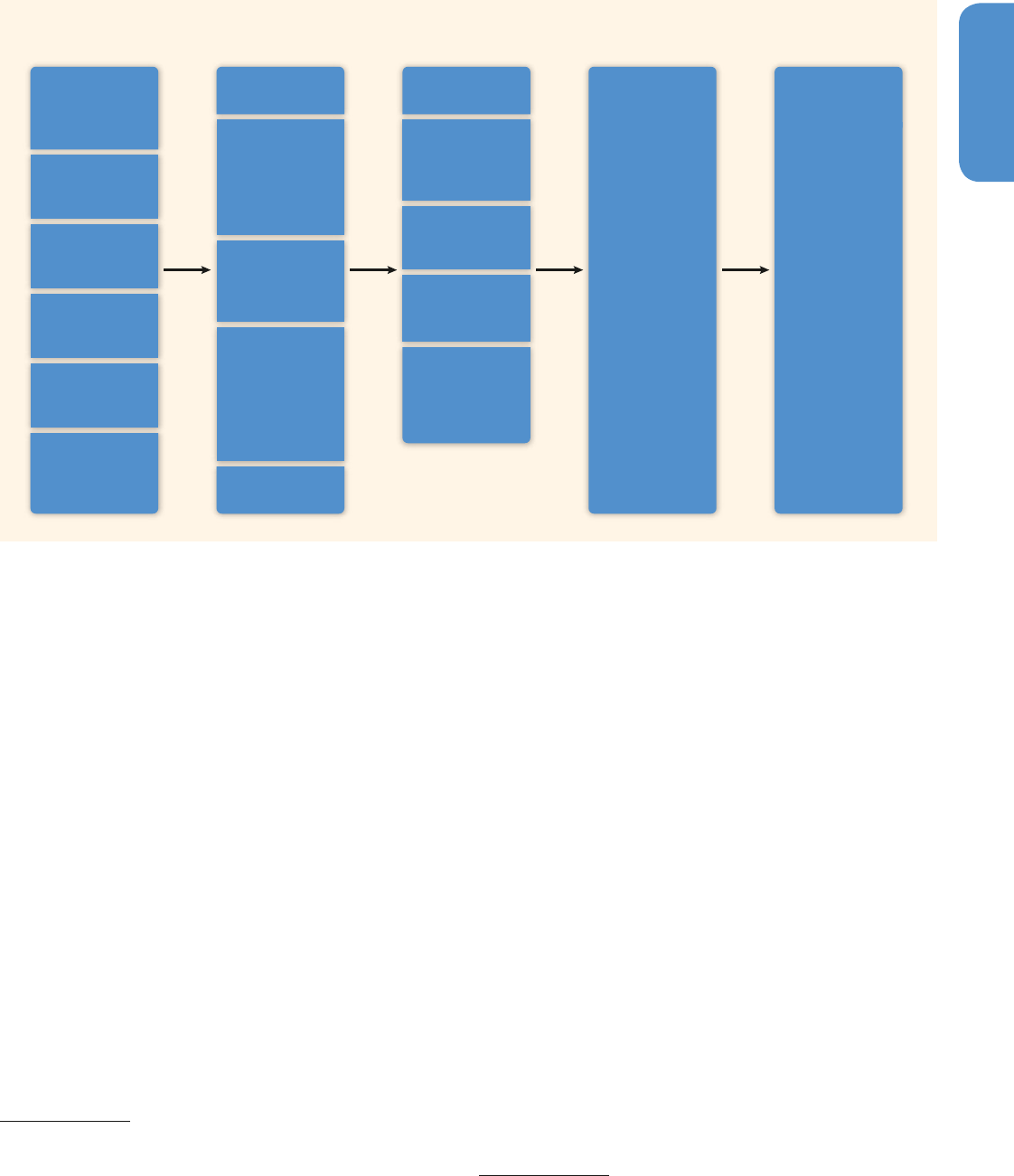

Figure 16.1 provides an overview of climate finance and the terms

used in this chapter. The term ‘capital’ is used because most climate

finance involves an investment, but it should be understood to include

all relevant financial flows

2

. One or more capital managers mobilize

the required capital and invest it in an adaptation or mitigation proj-

ect. Project owners or sponsors — governments, corporations, or

households — implement a project using their own and other sources

of capital. However, projects often obtain capital from multiple capital

managers (Buchner etal., 2011, 2012; Jürgens etal., 2012). An instru-

ment defines the financial agreement between a project owner / spon-

sor and a manager of capital. A project that obtains capital from sev-

2

Terms that cover both capital and operating costs, such as ‘financial resources’ or

‘funds’ are cumbersome (sources / managers of financial resources) or potentially

confusing (‘funds’ can also be institutions).

Figure 16�1 | Overview of climate finance flows. Note: Capital should be understood to include all relevant financial flows. The size of the boxes is not related to the magnitude of

the financial flow.

Source of Capital

Carbon Taxes

and Auction of

Allowances

General Tax

Revenue

International

Levies

Funds from

Capital Markets

Corporate

Cash Flow

Household

Income

Manager of Capital

Governments

National,

Bilateral and

Multilateral

Financial

Institutions

Commercial

Financial

Institutions

Corporate

Actors and

Institutional

Investors

(Private and

Public)

Households

Financial Instrument

Grants

Project Debt

(Market Based/

Concessional)

Project Level

Equity

Balance Sheet

Financing

Credit

Enhancement /

Risk

Management

Project Owner/Sponsor

Governments,

Corporations,

and Households

(Developed and

Developing

Countries)

Project

Adaptation

Mitigation

(incl. REDD)

12141214

Cross-cutting Investment and Finance Issues

16

Chapter 16

eral managers would use multiple instruments. The size of the boxes is

not related to the magnitude of the financial flow.

Data on current climate finance, summarized below, indicate that most

capital deployed is private — private corporations and households. That

is not surprising since they dominate the economy in most countries.

Domestically, government funds are disbursed directly as financial

incentives or tax credits, or through national financial institutions.

Climate finance under the UNFCCC currently is provided mainly by

the national governments of Annex II Parties. Climate finance from

the budgets of these government flows through bilateral institutions

being a national public entity, such as Japan International Coopera-

tion Agency (JICA), Agence Française de Développement (AFD), Kredi-

tanstalt für Wiederaufbau (KfW), or through multilateral institutions

having several countries as shareholders, such as the World Bank,

regional development banks, and multilateral climate funds.

There is no internationally agreed definition of mitigation and adapta-

tion projects; for example, whether a high-efficiency gas-fired gener-

ating unit is a mitigation project or which capacity building activities

help to address climate change. The relevant projects, and hence the

scale of climate finance, depend upon the definition of mitigation and

adaptation projects adopted. In practice, the definition varies across

studies and is often determined by the data available.

16�2�1�1 Estimates of current climate finance

This section reviews estimates of current global total climate finance,

total climate finance flowing to developing countries, public climate

finance provided to developing countries and climate finance under

the UNFCCC.

There is no comprehensive system for tracking climate finance (Clapp

etal., 2012; Tirpak etal., 2012), therefore, estimates must be compiled

from disparate sources of variable quality and timeliness, sources that

use different assumptions and methodologies and have gaps and

may occasionally duplicate coverage. Available data typically relate to

commitments rather than disbursements, so the amount reported may

not equal the amount received by the project owner during a given

year. Changes in exchange rates further complicate the picture. For

these and other reasons, estimates of current climate finance exhibit

considerable uncertainties.

Global total climate finance is estimated at 343 to 385 billion

USD per year for 2010 / 11 (2010 / 11 USD) and 356 to 363 billion USD

per year for 2011 / 12 (2011 / 12 USD), with mitigation accounting for

approximately 95 % of this amount (350 billion USD and 337 billion

USD, respectively) (Buchner etal., 2012, 2013b). This estimate includes

a mix of instruments, e. g., grants, concessional loans, commercial

loans and equity, as well as the full investment in mitigation measures

such as renewable energy generation technologies that also produce

other goods or services

3

. The figures reflect new commitments by capi-

tal managers using a mix of 2010 / 11 and 2011 / 12 data, respectively.

Private finance dominates the total, but its share declined from 74 %

(267billion USD) on average in 2010 and 2011 to 62 % (224 billion

USD) on average in 2011 and 2012 (2010 / 2011 USD and 2011 / 2012

USD) (Buchner et al., 2012, 2013b). Investment in renewable gen-

eration technologies dominates the mitigation investment (Frankfurt

School-UNEP Centre and BNEF, 2012).

Reasonably robust estimates of total climate finance for individual

countries are available for only a few cases, for instance, for Germany

(Jürgens etal., 2012). However, some institutions report on their financ-

ing commitments for climate and environment. Data from 19 develop-

ment banks indicate that commitments of mitigation finance increased

from 51 billion USD in 2011 to 65 billion USD in 2012 with commit-

ments of adaptation finance rising from 6 to 14 billion USD over the

same period (2011 / 2012 USD). Concessional funding provided by pub-

lic development banks plays an important role in financing domestic

climate projects, e. g., in Brazil, China, and Germany.

A growing number of developed and developing countries, including

Bangladesh, Colombia, Indonesia, Nepal, Samoa, Tanzania, Uganda,

and the United States as well as the European Commission, calculates

the share of their annual budget devoted to climate change mitiga-

tion and adaptation often using a methodology known as a Climate

Public Expenditure and Institutional Review (UNDP, 2013a). Country

estimates range from 3 – 15 % of the national budget.

A few estimates of total climate finance flowing to developing coun-

tries are available. Clapp etal. (2012) estimate the total at 70 – 120

billion USD per year based on 2009 – 2010 data (2009 / 2010 USD). Data

from Buchner etal. (2013a) suggest a net flow to developing countries

of the order of 40 to 60billion USD for 2010 and 2011 (2010 / 2011

USD).

4

For 2011 and 2012, North-South flows are estimated at 39

to 62 billion USD (2011 / 2012 USD) (Buchner et al., 2013b). Clapp

et al. (2012) estimate the private investment at 37 – 72 billion USD

(2009 / 2010 USD) per year based on 2009 – 2010 data and Stadelmann

3

Methodology used by Buchner et al. (2012, 2013b): Finance flows are limited to

‘climate-specific finance’, capital flows targeting low-carbon, and climate-resilient

development with direct or indirect mitigation or adaptation objectives / outcomes.

The focus is on current financial flows (upfront capital investment costs and grants

expressed as commitments, so risk management instruments are excluded). Data

are for total rather than incremental investment because incremental investment

requires assumptions on the baseline on a project-by-project basis. The data are

for ‘gross’ investment, the full value of the investment, and reflect commitments

because disbursement data is not widely available. The data are a mix of 2010

and 2011 data, and 2011 and 2012 data, respectively.

4

Buchner et al. (2013) estimate that developed countries mobilized 213 to 255 bil-

lion USD climate finance per year during 2010 and 2011 while 160 to 208 billion

USD climate finance had been committed to climate change projects in developed

countries. Developing countries mobilized 120 to 141 billion USD climate finance

per year during 2010 and 2011 and 162 to 202 billion USD had been commit-

ted to climate change projects in developing countries. Those figures suggest a

net flow to developing countries of the order of 40 to 60 billion USD per year

(2010 / 2011 USD).

12151215

Cross-cutting Investment and Finance Issues

16

Chapter 16

etal. (2013) estimate foreign direct investment as equity and loans in

the range of 10 to 37 billion USD per year based on 2008 – 2011 data

(2010 USD and 2008 USD).

The investment in registered Clean Development Mechanism

(CDM) projects is estimated at over 400 billion USD over the period

2004 to 2012 (2004 – 2012 USD) (UNEP Risø, 2013). Of that amount

almost 80 billion USD was for projects registered during 2011 and

195 billion USD for projects registered during 2012 (2011 USD and

2012 USD). The majority of the investment in CDM projects is private.

Renewable energy projects account for over 70 % of the total invest-

ment. The share of CDM renewable energy projects with some foreign

investment has grown over time, representing almost 25 billion USD in

2011 (2011 USD) (Kirkman etal., 2013).

5

Since 1999 almost 100 carbon funds with a capitalization of 14.2

billion USD have been established (Alberola and Stephan, 2010).

6

Carbon funds are investment vehicles that raise capital to purchase

carbon credits (52 %) and / or invest in emission reduction projects

(23 %). A fund may have only private investors (48 %), only public

investors (29 %) or a mix of both (23 %) (Alberola and Stephan, 2010).

Investment may be restricted to a specific region or project type (e. g.,

REDD+). Financial data, especially for private funds, is often confiden-

tial so the amount of finance provided to developing countries via

carbon funds is not available. Scaling up data from 29 funds on the

amount invested in projects suggests a maximum cumulative invest-

ment of 18 billion USD (1999 – 2009 USD) (Kirkman etal., 2013).

Public climate finance provided to developing countries was esti-

mated at 35 to 49 billion USD per year in 2011 and 2012 (2011 / 2012

USD) (Buchner etal., 2013b).

7

These public funds flow mainly through

bilateral and multilateral institutions

8

. Most of the climate finance is

implemented by development banks, frequently involving the blend-

ing of government resources with their own funds. There are two main

reporting systems for public support in place that are not fully compa-

rable due to differences in respective methodologies.

The Organisation for Economic Co-operation and Development (OECD)

Development Assistance Committee (DAC) reports the amount of offi-

cial development assistance (ODA) committed bilaterally for projects

5

CDM projects sell emission reduction credits, Certified Emission Reductions (CERs),

to developed country buyers, which provide a return to developed country inves-

tors.

6

United Nations Environment Program (UNDP) estimates that in addition up to

6000 private equity funds have been established for the purpose of funding

climate change-related activities (UNDP, 2011).

7

Buchner et al. (2013b) count climate finance provided by bilateral finance institu-

tions, multilateral finance institutions, government bodies, and climate funds as

public flows. The difference between lower- and upper-bound results when taking

the ownership structure of multilateral institutions into account and excluding all

bilateral flows marked as having climate as ‘significant’ objective.

8

Ryan et al. (2012) estimate the annual average finance provided to developing

countries for energy efficiency at 18.9 billion USD in 2010 from bilateral financial

institutions and 4.9 billion USD from multilateral financial institutions over the

period 2008 – 2011.

that have climate change mitigation or adaptation as a ‘principal’ or

‘significant’ objective by its 23 member countries and the European

Commission. The DAC defines ODA as those flows to countries on the

DAC List of ODA Recipients and to multilateral institutions provided

by official agencies or by their executive agencies. Resources must be

used to promote the economic development and welfare of develop-

ing countries as a main objective and they must be concessional in

character, meaning as grants or as concessional loans including a grant

element of at least 25 %, calculated at a rate of discount of 10 %. The

amount is the total funding committed to each project, not the share

of the project costs attributable to climate change (OECD, 2013a).

Researchers have questioned the accuracy of the project classification

(Michaelowa and Michaelowa, 2011; Junghans and Harmeling, 2013).

Bilateral commitments averaged 20 billion USD per year in 2010 and

2011 (2010 / 2011 USD) (OECD, 2013a) and were implemented by

bilateral development banks or other bilateral agencies, provided to

national government directly or to dedicated multilateral climate funds

(Buchner etal., 2012, 2013b).

Seven multilateral development banks (MDBs)

9

reported climate

finance commitments of about 24.1 and 26.8 billion USD in 2011 and

2012, respectively (2011 / 2012 USD). The reporting is activity-based

allowing counting entire projects but also project components. Recipi-

ent countries include developing countries and 13 European Union

(EU) member states. It covers grant, loan, guarantee, equity, and per-

formance-based instruments, not requiring a specific grant element.

The volume covers MDBs’ own resources as well as external resources

managed by the MDBs that are also reported to OECD DAC (such as

contributions to the Global Environment Facility (GEF), Climate Invest-

ment Funds (CIFs), and Carbon Funds) (AfDB etal., 2012a; b, 2013).

Under the UNFCCC, climate finance is not well-defined. Annex II

Parties committed to provide new and additional financial resources

to cover the “agreed full incremental costs” of agreed mitigation mea-

sures implemented by developing countries (Article 4.3), to “assist

the developing country Parties that are particularly vulnerable to the

adverse effects of climate change in meeting costs of adaptation”

(Article 4.4) and to cover the agreed full costs incurred by developing

countries for the preparation of their national communications (Article

4.3) (UNFCCC, 1992). None of these terms are operationally defined

(Machado-Filho, 2011). These commitments are reaffirmed by the Kyoto

Protocol (UNFCCC, 1998, Art. 11). The Conference of Parties (COP) has

agreed that funds provided to developing country Parties may come

from a wide variety of sources, public, and private, bilateral and multi-

lateral, including alternative sources (UNFCCC, 2010, para. 99).

AnnexII Parties report the financial resources they provide to develop-

ing countries through bilateral and multilateral channels for climate

9

African Development Bank (AfDB), the Asian Development Bank (ADB), the Euro-

pean Bank for Reconstruction and Development (EBRD), the European Investment

Bank (EIB), the Inter-American Development Bank (IDB), the World Bank (WB) and

the International Finance Corporation (IFC).

12161216

Cross-cutting Investment and Finance Issues

16

Chapter 16

change action to increase transparency about public flows of climate

finance vis-à-vis expectations and needs. The latest summary of the

AnnexII reports on their provided climate finance indicates that they

provided a total of 58.4 billion USD for the period 2005 through

2010, an average of nearly 10 billion USD per year (2005 – 2010 USD)

(UNFCCC, 2011a).

10

Most of the funds provided are concessional loans

and grants. In addition, a range of developed countries promised FSF

of about 10 billion USD per year from 2010 to 2012 (2010 / 2011 / 2012

USD) (see Section16.2.1.3).

11

Operating entities of the financial mechanism of the UNFCCC deal

with less than 10 % of the climate finance reported under the Conven-

tion, although that could change once the Green Climate Fund (GCF)

becomes operational. AnnexII Party contributions to the Trust Fund of

the GEF, the Special Climate Change Fund (SCCF) and the Least Devel-

oped Countries Fund (LDCF) amounted to about 3.3billion USD for

2005 through 2010, an average of less than 0.6 billion USD per year

(2005 – 2010USD) (UNFCCC, 2011a). Most of the funds are used for

mitigation. The Adaptation Fund derives most of its funds from the sale

of its share of the CERs issued for CDM projects

12

.

16�2�1�2 Current sources of climate finance

Climate finance comes from the sources of capital shown in Figure

16.1 including capital markets, carbon markets, and government bud-

gets. Most government funding comes from general revenue but some

governments also raise revenue from sources — carbon taxes and auc-

tioned GHG-emission allowances — that have mitigation benefits. Most

corporate funding comes from corporate cash flow including corporate

borrowing, often called balance-sheet finance (Frankfurt School-UNEP

Centre, 2013).

13

Household funding comes from household income from

wages, investments, and other sources. Governments, corporations, and

households can all access capital markets to mobilize additional funds.

10

Although there is an agreed reporting format, the UNFCCC Secretariat notes

that many data gaps and inconsistencies persist in the reporting approaches of

AnnexII Parties. The information is compiled by the UNFCCC Secretariat from

AnnexII national communications. The figures represent ‘as committed’ or ‘as

spent’ currency over the 6 years. The procedures used by different countries and

the Secretariat to convert currencies into USD are not known.

11

Although COP took note of the ´fast start finance’ (FSF) commitment in paragraph

95 of Decision 1 / CP.16 (UNFCCC, 2010) and the funds committed have been

reported annually to the UNFCCC, the FSF is not formally climate finance under

the UNFCCC.

12

Currently the only international levy is the 2 % of the CERs issued for most CDM

projects provided to the Adaptation Fund. The Fund sells the CERs and uses the

proceeds for adaptation projects in developing countries. Sale of CERs gener-

ated revenue of over 90 million USD for FY 2010 (2010 / 2011 USD) and over 50

million USD for FY 2011 (World Bank, 2012a). In December 2012 Parties agreed

to extend the share of proceeds levy to the issuance of emission reduction unit

(ERUs) and the first international transfers of AAUs (UNFCCC, 2012a, para. 21).

13

General revenue includes revenue collected from all taxes and charges imposed

by a government. Balance sheet finance means that a new investment is financed

by the firm rather than as a separate project. The firm may seek external funding

(debt and / or equity) but that funding is secured by the operations of the firm

rather than the new investment.

This section summarizes estimates of the revenue currently generated

by carbon taxes and auctioned GHG-emission allowances. Fuel taxes,

fossil fuel royalties, and electricity charges can be converted to CO

2

eq

charges but they are excluded here because they are usually imple-

mented for different policy goals.

Carbon taxes generate about 7 billion USD in revenue annually

mainly in European countries (2010 / 2011 USD).

14

Denmark, Finland,

Germany, Ireland, Italy, Netherlands, Norway, Slovenia, Sweden, Swit-

zerland, and the United Kingdom — generated about 6.8 billion USD in

2010 (2010 USD) and 7.3 billion USD (2011 USD) in 2011. India

15

, Aus-

tralia, and Japan introduced carbon taxes in July 2010, July 2012, and

October 2012, respectively. In some countries, part or all of the rev-

enue is dedicated to environmental purposes or reducing other taxes;

none is earmarked for international climate finance.

Auctioned allowances, fixed price compliance options, and the interna-

tional sale of surplus Assigned Amount Units (AAUs) generate about

2 billion USD per year for national governments (2010 / 2011 USD).

Among the 30 countries participating in the EU emissions trading

scheme, Austria, Germany, Hungary, Ireland, the Netherlands, Norway,

and the United Kingdom auctioned some emission allowances during

the second (2008 – 2012) phase (European Commission, 2012). Buch-

ner etal. (2011, 2012) estimate auction revenue at 1.4 and 1.6 bil-

lion USD for 2010 and 2011 (2010 / 2011 USD). Germany has so far

earmarked a portion of its auction revenue for international climate

finance (Germany Federal Ministry for the Environment Nature Con-

servation and Nuclear Safety, 2012). New Zealand collected 1.25 and

1.42 million USD for 2010 (6 months) and 2011, respectively, from its

fixed price compliance option of 10.8 USD per tonne of CO

2

(15 NZD)

(New Zealand Ministry for the Environment, 2012).

Several eastern European countries (Estonia, Czech Republic, Poland,

and Russia) sell surplus AAUs to generate revenue. Others such as Bul-

garia, Latvia, Lithuania, Slovakia, and Ukraine, sell their surplus AAUs

to fund Green Investment Schemes that support domestic emission

reduction measures (Linacre etal., 2011).

16

Revenue rose from 276 mil-

lion USD in 2008 (2008 USD) to 2 billion USD in 2009 (2009 USD) and

then declined to less than 1.1 billion USD in 2010 (2010 USD) (Kossoy

and Ambrosi, 2010; Linacre etal., 2011; Tuerk etal., 2013). Buchner at

al. (2011, 2012) estimate the revenue at 580 and 240 million USD for

2010 and 2011, respectively (2010 and 2011 USD).

14

Revenue from taxes explicitly named carbon taxes in the OECD database of

environmentally related taxes, available at http: / / www2. oecd. org / ecoinst /

queries / index.htm.

15

In India, the carbon tax is on coal only.

16

The Green Investment Schemes are a source of climate finance for these countries.

12171217

Cross-cutting Investment and Finance Issues

16

Chapter 16

16�2�1�3 Recent developments

Climate finance has been affected by the financial crisis of late 2008,

the subsequent stimulus packages and the FSF commitment of 30 bil-

lion USD for 2010 – 2012 made by developed countries in December

2009 for climate action in developing countries.

The financial crisis in late 2008 reduced investment in renewable

energy (Hamilton and Justice, 2009). In late 2008 and early 2009,

investment in renewable generation fell disproportionately more than

that in other types of generating capacity (IEA, 2009). Global invest-

ment in renewable energy fell 3 % during 2009 but rebounded strongly

in 2010 and 2011. In developed countries, where the financial crisis hit

hardest, investment dropped 14 % while renewable energy investment

continued to grow in developing countries (Frankfurt School-UNEP

Centre and BNEF, 2012).

In response to the financial crisis, Group of Twenty Finance Ministers

(G20) governments implemented economic stimulus packages

amounting to 2.6 trillion USD. Of that amount, 180 to 242 billion USD

was low-carbon funding (2008 and 2009 USD) (IEA, 2009; REN21,

2010). The stimulus spending supported the rapid recovery of renewable

energy investment by compensating for reduced financing from banks.

Some countries facing large public sector deficits scaled down green

spending when the economy started recovering (Eyraud etal., 2011).

At the UNFCCC in Copenhagen in 2009, developed countries committed

to provide new and additional resources approaching 30 billion USD of

FSF to support mitigation and adaptation action in developing countries

during 2010 – 2012 (UNFCCC, 2009a). The sum of the announced com-

mitments exceeds 33 billion USD (UNFCCC, 2011b, 2012b; c, 2013a)

17

.

Japan, United States, United Kingdom, Norway, and Germany being the

five biggest donors have reported commitments amounting to 27 billion

USD (2010 / 2011 / 2012 USD). Nakooda et al. (2013) finds that around

45 % have been provided as grants and around 47 % in the form of

loans, guarantees, and insurance. Approximately 61 % of the funds had

been committed for mitigation, 10 % for REDD+, ,18 % for adaptation,

9 % for multiple objectives and for 2 % of the funding the purpose is

unknown. The funders reported commitments to recipient country gov-

ernments via bilateral channels (33 %), multilateral climate funds (20 %),

recipient countries companies (12 %), and multilateral institutions (9 %).

Data on actual disbursements is not available to date because of the

multi-year time lag between commitment and disbursement.

The announced pledges triggered questions as to whether they were

‘new and additional’ as promised (Fallasch and De Marez, 2010; BNEF,

2011). Some countries explain the basis on which they consider their

pledge to be ‘new and additional’. Criteria have been proposed that

17

The information is compiled by the UNFCCC Secretariat from national reports

on FSF. The figures represent ‘as committed’ currency over the three years. The

procedures used by different countries and the Secretariat to convert currencies

into USD are not known.

indicate, when applied to the pledges, that proportions ranging from

virtually none to almost all are new and additional (Brown etal., 2010;

Stadelmann etal., 2010, 2011b). For Germany, Japan, the United King-

dom, and the United States annual FSF contributions were significantly

higher than the 2009 expenditure related to climate activities in devel-

oping countries (Nakooda etal., 2013).

16�2�2 Future low-carbon investment

As noted in Chapter 6, the stabilization of GHG concentrations will ulti-

mately require dramatic changes in the world’s energy system, includ-

ing a dramatic expansion in the deployment of low-carbon energy

sources. This change will require significant shifts in global investment

in the energy, land use, transportation, and infrastructure sector. The

future investment flows summarized in this section are based on sev-

eral large-scale analyses conducted over the past few years. For the

most part these analyses explore scenarios to achieve specified tem-

perature or concentration goals. Hence, the estimates of investment

flows drawn from these studies should not be interpreted as forecasts,

but rather, as some probable future states of the world.

Figure 16.2 presents estimates of baseline, i. e., current investment

in energy supply sub-sectors as a reference for the following consid-

erations. It illustrates the very substantial nature of investments in

today’s energy sector with global total annual investment at about

USD

2010

1200 billion and very strong roles for investments in fossil fuel

extraction, transmission and distribution (T&D), and electricity genera-

tion.

16�2�2�1 Investment needs

While a large number of studies and many modelling comparison

exercises have assessed technological transformation pathways and

the macroeconomic costs of transforming the global economy, only a

handful of studies estimate the associated investment needs. Section

16.2.2.2 summarizes available estimates of investment needs under

climate policy between 2010 – 2029 and 2030 – 2049, for the world as

a whole and for non-OECD and OECD countries. Models and scenarios

differ so the focus is on incremental investment, i. e., the differences in

the estimated investment between the reference and mitigation sce-

narios.

18

It must also be noted that the model estimates crucially rely

on assumptions about the future costs of technologies and of subsi-

dies, on the possibility of nuclear phaseout in some countries, and on

the mitigation policies already included in the reference scenarios.

Without climate policy, investments in the power sector would

mainly be directed towards fossil fuels, especially in non-OECD coun-

tries that rely on low-cost coal power plants to supply their growing

18

Adaptation costs and economic losses from future climate change are not consid-

ered in any of these estimates.

12181218

Cross-cutting Investment and Finance Issues

16

Chapter 16

demand for electricity. At the global level, fossil fuel-based power

generation would require an average annual investment of 182 (95

to 234) billion USD in 2010 – 2029 and 287 (158 to 364) billion USD

in 2030 – 2049;

19

the bulk of investments (roughly 80 %) goes to non-

OECD countries.

20

There is greater uncertainty in models about the

future of renewable and nuclear power without climate policy. Mod-

elled global investment in renewable power generation is expected

to increase over time from 123 (31 to 180) billion USD per year in

2010 – 2029 to 233 (131 to 336) billion USD over 2030 – 2049. Nuclear

power generation would attract 55 (11 to 131) billion USD annually in

2010 – 2029 and 90 (0 to 155) billion USD per year in 2030 – 2049.

The introduction of an emission reduction target in the models

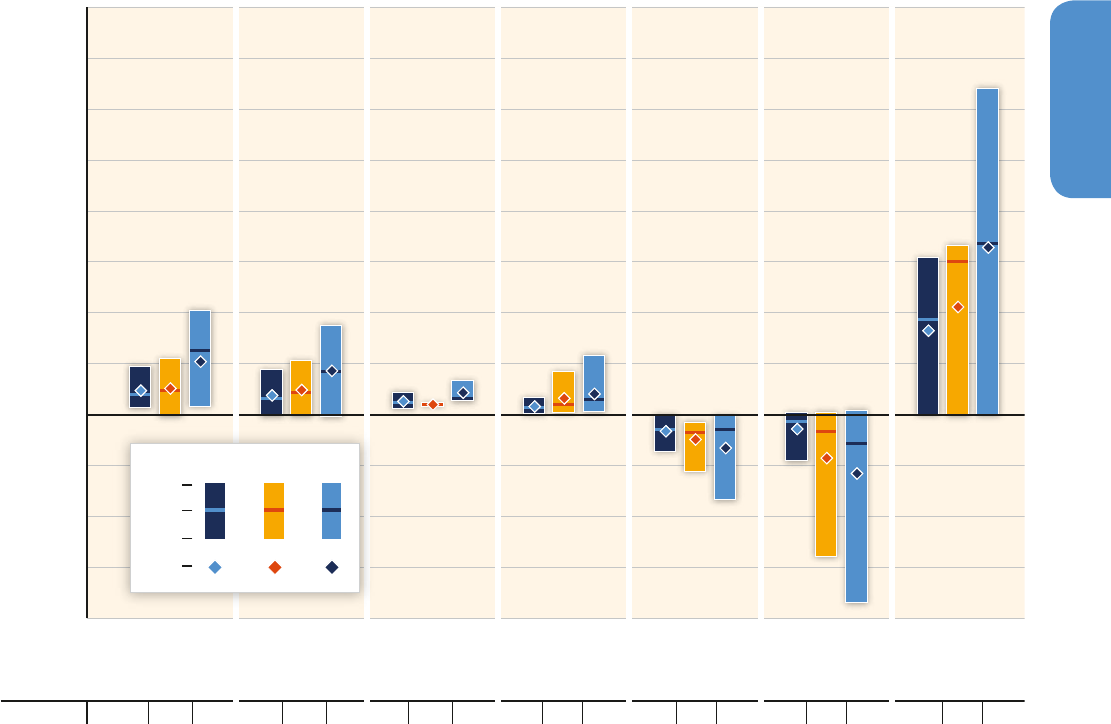

abruptly changes the investment pattern. Figures 16.3 and 16.4 report

the investment change for major power generation technologies,

fossil fuel extraction, and for end-use energy efficiency, for emission

scenarios compatible with a long-term target of keeping mean global

temperature increase below 2 °C in 2100.

21

Although the policy targets

19

The mean should not be considered as an expected value. It is not possible to

attribute any probability distribution to models’ outcomes. Therefore policymakers

face pure uncertainty in face of future investment needs. The range is presented to

provide information on the degree of uncertainty in the literature.

20

See captions of Figures 16.3 and 16.4 for a list of the studies surveyed.

21

Also in this case, the mean and median are used as synthetic indicators having no

predictive power.

are not identical, they are close enough to allow a broad comparison

of results. The dispersion across estimated emission reductions over

2010 – 2029 and 2010 – 2049 is mainly due to differences in reference

scenario emissions and because models choose different optimal emis-

sion trajectories among the many compatible with the long-term cli-

mate goal.

The results of an analysis of investment estimates in Figures 16.3 and

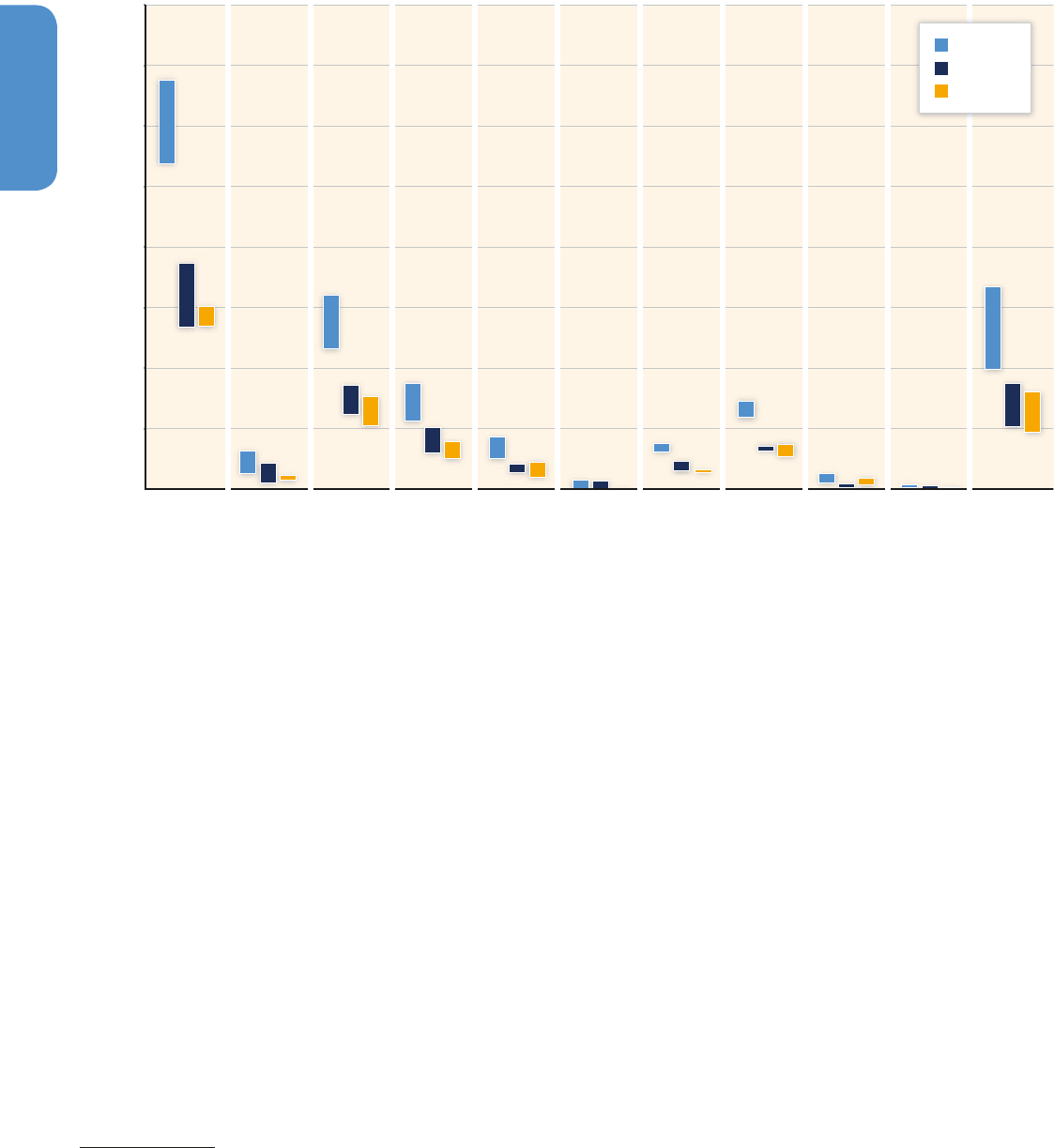

16.4 show that climate policy is expected to induce a major reallo-

cation of investments in the power sector. Investments in fossil-fired

power plants (without CCS) were equal to about 137 billion USD per

year in 2010. Investment would decline by 30 (2 to 166) billion USD

per year (about – 20 % for the median) during the period 2010 – 2029,

compared to the reference scenarios. Investment in low-emissions

generation technologies (renewable, nuclear, and electricity genera-

tion with CCS) would increase by 147 (31 to 360) billion USD per year

(about 100 % for the median) during the same period.

Based on a limited number of studies (McKinsey, 2009; IEA, 2011; Riahi

et al., 2012), annual incremental investments until 2030 in energy-

efficiency investments in the building, transport, and industry sector

increase by 336 (1 to 641) billion USD. The only three studies with sec-

toral detail in end-use technologies show an increase of investments

of 153 (57 to 228) billion USD for the building sector, 198 (98 to 344)

billion USD for the transport sector, 80 (40 to 131) billion USD for the

Present Level of Investment in Energy Supply [Billion USD

2010

/yr]

0

200

400

600

800

1000

1200

1400

1600

Total Energy

Sector

Other Energy

Technologies

Total Electricity

Sector

Total Electricity

Generation

Renewables Nuclear Total Fossil

Power Plants

Electricity

T&D

Fossil Liquid

Fuels

Liquid Biofuels Extraction of

Fossil Fuels

World

OECD

Non-OECD

Figure 16�2 | Present level of investment in energy supply. Note: The bars indicate the minimum and maximum level of investments found in the literature. Ranges result from

different sources of market information and differing definitions of the investment components to be included. Source: From McCollum etal. (2013) based on data from IEA World

Energy Outlook 2011 (IEA, 2011) and GEA (Riahi etal., 2012).

12191219

Cross-cutting Investment and Finance Issues

16

Chapter 16

industry sector. Incremental investments in end-use technologies are

particularly hard to estimate and the number of studies is limited

(Riahi etal., 2012). Results should therefore be taken with caution.

While models tend to agree on the relative importance of investments

in fossil and non-fossil power generation, they differ with respect to

the mix of low-emission power generation technologies and the over-

all incremental investment. This is mainly due to different reference

scenarios (e. g., population, economic growth, exogenous technologi-

cal progress), and assumptions about (1) the structure of the energy

system and the costs of reducing the energy intensity of the economy

versus reducing the carbon intensity of energy, (2) the investment costs

of alternative technologies over time, and (3) technological or politi-

cal constraints on technologies. Limits to the deployment of some key

technology options or the presence of policy constraints (e. g., delayed

action, limited geographical participation) would increase investment

needs (Riahi etal., 2012; McCollum etal., 2013).

Higher energy efficiency, technological innovation in transport, and

the shift to low-emission generation technologies — all contribute to

a drastic reduction in the demand for fossil fuels, thus causing a sharp

decline in investment in fossil fuel extraction, transformation, and

transportation. Scenarios from a limited number of models suggest

that average annual investment reduction in 2010 – 2029 would be

equal to 56 (– 8 to 369) billion USD. The contraction would be sharper

in 2030 – 2049, in the order of 451 (332 to 1385) billion USD per year.

Figure 16�3 | Change of average annual investment in mitigation scenarios (2010 – 2029). Investment changes are calculated by a limited number of model studies and model

comparisons for mitigation scenarios that stabilize concentrations within the range of 430 – 530 ppm CO

2

eq by 2100 compared to respective average baseline investments. Note:

The vertical bars indicate the range between minimum and maximum estimate of investment changes; the horizontal bar indicates the median of model results. Proximity to this

median value does not imply higher likelihood because of the different degree of aggregation of model results, low number of studies available, and different assumptions in the

different studies considered. The numbers in the bottom row show the total number of studies available in the literature. Sources: UNFCCC (2008). IEA (2011): 450 Scenario (450)

relative to the Constant Policies Scenario (CPS). The CPS investment in CCS is also included under Coal and Gas (retrofitting); World investment in biofuels includes international

bunkers; investment in solar photovoltaic (PV) in buildings is attributed to power plants in supply-side investment. Riahi etal. (2012): the Global Energy Assessment Mix scenario

(GEA-Mix) relative to the GEA reference scenario. Carraro etal. (2012): 460 ppm CO

2

eq in 2100 (t460) relative to reference scenario. McCollum etal. (2013): the Low Climate

Impact Scenarios and Implications of Required Tight Emission Control Strategies (LIMITS), RefPol-450 scenario (2.8 W / m

2

in 2100) relative to the reference scenarios, mean of six

models. McKinsey (2009): data obtained from Climate Desk, S2015 scenario with full technological potential, 100 % success rate, negative lever of costs, beginning of policy in

2015 | Regions: OECD, non-OECD, and World.

-400

-300

-200

-100

0

100

200

300

400

500

600

700

800

Power Plants

with CCS

Renewables Energy Efficiency

Across Sectors

Extraction of

Fossil Fuels

Fossil Fuel

Power Plants

without CCS

NuclearTotal Electricity

Generation

# of Studies: 43444444 3545

4545455 44

Changes in Annual Investment Flows 2010-2029 [USD

2010

Billion /yr]

Max

Median

Mean

Min

Non-OECD

WorldOECD

12201220

Cross-cutting Investment and Finance Issues

16

Chapter 16

All models that provide data on investments for fossil fuel extraction

show that overall investments in energy supply would decrease against

the baseline trends in scenarios consistent with the 2 °C limit (IEA,

2011; Carraro etal., 2012; Riahi etal., 2012; McCollum etal., 2013).

According to a range of models, climate policy would thus substan-

tially change the allocation of baseline energy investments rather than

increase overall demand for energy investment.

Models with a separate consideration of energy-efficiency measures fore-

see the need for significant incremental investment in energy efficiency

in the building, transport, and industry sector in addition to the realloca-

tion of investment from high-carbon to low-carbon power supply.

There is wide agreement among model results on the necessity to

ramp up investments in research and development (R&D) to increase

end-use energy efficiency and to improve low-emission generation

energy carriers and energy transformation technologies. Estimates of

the additional funding needed for energy-related R&D range from

4.5 to 78 billion USD per year during 2010 – 2029 (UNFCCC, 2007;

Carraro etal., 2012; McCollum etal., 2013) and from 115 to 126

billion USD per year in 2030 – 2049 (Carraro etal., 2012; Marangoni

and Tavoni, 2013; McCollum etal., 2013). Because of the need for

new low-carbon alternatives, investments in R&D are higher in case

of nuclear phaseout and other technological constraints (Bosetti

etal., 2011).

Figure 16�4 | Change of average annual investment in mitigation scenarios (2030 – 2049). Investment changes are calculated by a limited number of model studies and model

comparisons for mitigation scenarios that stabilize concentrations within the range of 430 – 530 ppm CO

2

eq by 2100 compared to respective average baseline investments. Note:

The vertical bars indicate the range between minimum and maximum estimate of investment changes; the horizontal bar indicates the median of model results. Proximity to this

median value does not imply higher likelihood because of the different degree of aggregation of model results, low number of studies available, and different assumptions in the

different studies considered. The numbers in the bottom row show the total number of studies available in the literature. Sources: Riahi etal. (2012): the Global Energy Assessment

Mix scenario (GEA-Mix) relative to the GEA reference scenario. Carraro etal. (2012): 460 ppm CO

2

eq in 2100 (t460) relative to reference scenario. McCollum etal. (2013): the Low

Climate Impact Scenarios and Implications of Required Tight Emission Control Strategies (LIMITS), RefPol-450 scenario (2.8 W / m

2

in 2100) relative to the reference scenarios, mean

of six models. Regions: OECD, non-OECD, and World.

# of Studies: 21222222 1323

2323

233 22

Max

Median

Mean

Min

Non-OECD

WorldOECD

Power Plants

with CCS

Fossil Fuel

Power Plants

without CCS

-1500

-1200

-900

-600

-300

0

300

600

900

Total Electricity

Generation

Renewables Energy Efficiency

Across Sectors

Extraction of

Fossil Fuels

Nuclear

Changes in Annual Investment Flows 2030-2049 [Billion USD

2010

/yr]

12211221

Cross-cutting Investment and Finance Issues

16

Chapter 16

Land-use is the second largest source of GHG emissions and within

land use, tropical deforestation is by far the largest source (see Chap-

ters 5 and 11). Efforts to stabilize atmospheric concentrations of GHGs

will require investments in land use change (LUC) as well as in the

energy sector.

Kindermann etal. (2008) use three global forestry and land use models

to examine the costs of reduced emissions through avoided deforesta-

tion over the 25 year period from 2005 – 2030.

22

The models’ results

suggest substantial emission reductions can be achieved. The mod-

els estimate that 1.6 to 4.3 GtCO

2

per year could be reduced for 20

USD tCO

2

with the greatest reductions coming from Africa followed

by Central and South America and Southeast Asia. They also use the

models to estimate the costs to reduce deforestation by between 10 %

and 50 % of the baseline. Deforestation could be reduced by 10 %

(0.3 – 0.6 GtCO

2

per year) over the 25-year period for an investment

of 0.5 to 2.1 billion USD per year in forest preservation activities, and

a 50 % reduction (1.5 – 2.7 GtCO

2

per year) could be achieved for an

investment of 21.2 to 34.9 billion USD per year. This is comparable to

what has been found by UNFCCC (2008) and McCollum etal. (2013).

Investment needs in other sectors commonly relate to energy-effi-

ciency measures included above. Information on global or regional

investment needs to abate process emissions or non-CO

2

emissions in

sectors like the waste, petroleum, gas, cement, or the chemical industry

is virtually unavailable. For instance, McKinsey (2009) does not pro-

vide information that could be separated from energy-efficiency mea-

sures in the sectors. An indicative estimate for the waste sector can

be derived from Pfaff-Simoneit (2012) suggesting investment needs of

approximately 10 – 20 billon USD per year if access to a modern waste

management system were to be provided for an additional 100million

people per year.

16�2�2�2 Incremental costs

Incremental costs can be calculated for an individual project, a pro-

gramme, a sector, a country, or the world as a whole. The incremental

costs reflect the incremental investment and the change of operating

and maintenance costs for a mitigation or adaptation project in com-

parison to a reference project. It can be calculated as the difference of

the net present values of the two projects. Estimates of the incremen-

tal costs of mitigation measures for key sectors or the entire economy

have been prepared for over 20 developing countries (Olbrisch etal.,

2011). When estimates of both the incremental costs and the incre-

mental investment are available, the former is generally lower because

of the annualization of incremental investments for the calculation of

incremental costs.

22

The models used are the Dynamic Integrated Model of Forestry and Alternative

Land Use (DIMA) (Roktiyanskiy et al., 2007), the Generalized Comprehensive

Mitigation Assessment Process Model (GCOMAP) (Sathaye et al., 2006), and the

Global Timber Model (GTM) (Sohngen and Mendelsohn, 2003).

From an economic perspective, macroeconomic incremental costs can

be defined as the lost gross domestic product (GDP). This measure

provides an aggregate cost of the mitigation actions (estimates pro-

vided in Chapter 6), but it does not provide information on the specific

micro-economic investments that must be made and costs incurred to

meet the mitigation commitments. This distinction is important if inter-

national climate finance commitments will be implemented through

institutions designed to provide financial support for specific invest-

ments and costs rather than macro-level compensation.

Other than on the project-level, investment needs are thus frequently

only a fraction of incremental costs on the level of the macro-economy.

This difference is largely due to reduced growth of carbon-constrained

economies in many models. Adaptation costs and economic losses

from future climate change, which are not considered in these esti-

mates, should be lower for climate policy scenarios than in the refer-

ence scenario.

16�2�3 Raising public funding by developed

countries for climate finance in

developing countries

Comparison of the model estimates of future mitigation investment

(Section 16.2.2) with the current level of global total climate finance

(Section 16.2.1.1) indicates that global climate finance needs to be

scaled up. Increased financial support by developed countries for

mitigation (and adaptation) in developing countries will be needed

to stimulate the increased investment. This section reviews possible

sources of additional funds that could be implemented by developed

country governments to finance mitigation in developing countries.

In December 2009, developed countries committed to a goal of mobi-

lizing jointly 100 billion USD a year by 2020 to address the needs of

developing countries in the context of meaningful mitigation actions

and transparency on implementation. This funding will come from a

wide variety of sources, public and private, bilateral and multilateral,

including alternative sources of finance (UNFCCC, 2009a).

23

This goal

has been recognized by the COP (UNFCCC, 2010, para. 98). This rec-

ognition does not change the commitments of AnnexII Parties speci-

fied in Article 4 of the Convention to provide financial resources for

climate-related costs incurred by developing countries.

Studies by the High-level Advisory Group on Climate Change Financ-

ing (AGF) (AGF, 2010) and the World Bank Group etal. (2011) at the

request of G20 finance ministers have analyzed options for mobilizing

100 billion USD per year by 2020. The AGF concluded that it is chal-