659

10

Key Economic Sectors

and Services

Coordinating Lead Authors:

Douglas J. Arent (USA), Richard S.J. Tol (UK)

Lead Authors:

Eberhard Faust (Germany), Joseph P. Hella (Tanzania), Surender Kumar (India),

Kenneth M. Strzepek (UNU/USA), Ferenc L. Tóth (IAEA/Hungary), Denghua Yan (China)

Contributing Authors:

Francesco Bosello (Italy), Paul Chinowsky (USA), Kristie L. Ebi (USA), Stephane Hallegatte

(France), Robert Kopp (USA), Simone Ruiz Fernandez (Germany), Armin Sandhoevel

(Germany), Philip Ward (Netherlands), Eric Williams (IAEA/USA)

Review Editors:

Amjad Abdulla (Maldives), Haroon Kheshgi (USA), He Xu (China)

Volunteer Chapter Scientist:

Julius Ngeh (Cameroon)

This chapter should be cited as:

Arent

, D.J., R.S.J. Tol, E. Faust, J.P. Hella, S. Kumar, K.M. Strzepek, F.L. Tóth, and D. Yan, 2014: Key economic

sectors and services. In: Climate Change 2014: Impacts, Adaptation, and Vulnerability. Part A: Global and

Sectoral Aspects. Contribution of Working Group II to the Fifth Assessment Report of the Intergovernmental

Panel on Climate Change [Field, C.B., V.R. Barros, D.J. Dokken, K.J. Mach, M.D. Mastrandrea, T.E. Bilir,

M. Chatterjee, K.L. Ebi, Y.O. Estrada, R.C. Genova, B. Girma, E.S. Kissel, A.N. Levy, S. MacCracken,

P.R. Mastrandrea, and L.L. White (eds.)]. Cambridge University Press, Cambridge, United Kingdom

and New York, NY, USA, pp. 659-708.

10

660

Executive Summary............................................................................................................................................................ 662

10.1. Introduction and Context ....................................................................................................................................... 664

10.2. Energy ..................................................................................................................................................................... 664

10.2.1. Energy Demand ................................................................................................................................................................................ 664

10.2.2. Energy Supply ................................................................................................................................................................................... 665

10.2.3. Transport and Transmission of Energy ............................................................................................................................................... 668

10.2.4. Macroeconomic Impacts ................................................................................................................................................................... 669

10.2.5. Summary .......................................................................................................................................................................................... 672

10.3. Water Services ........................................................................................................................................................ 672

10.3.1. Water Infrastructure and Economy-Wide Impacts ............................................................................................................................. 672

10.3.2. Municipal and Industrial Water Supply ............................................................................................................................................. 673

10.3.3. Wastewater and Urban Stormwater ................................................................................................................................................. 673

10.3.4. Inland Navigation ............................................................................................................................................................................. 673

10.3.5. Irrigation ........................................................................................................................................................................................... 673

10.3.6. Nature Conservation ......................................................................................................................................................................... 674

10.3.7. Recreation and Tourism .................................................................................................................................................................... 674

10.3.8. Water Management and Allocation .................................................................................................................................................. 674

10.3.9. Summary .......................................................................................................................................................................................... 674

10.4. Transport ................................................................................................................................................................. 674

10.4.1. Roads ................................................................................................................................................................................................ 674

10.4.2. Rail ................................................................................................................................................................................................... 675

10.4.3. Pipeline ............................................................................................................................................................................................. 675

10.4.4. Shipping ........................................................................................................................................................................................... 675

10.4.5. Air ..................................................................................................................................................................................................... 676

10.5. Other Primary and Secondary Economic Activities ................................................................................................. 676

10.5.1. Primary Economic Activities .............................................................................................................................................................. 676

10.5.1.1. Crop and Animal Production ............................................................................................................................................. 676

10.5.1.2. Forestry and Logging ......................................................................................................................................................... 676

10.5.1.3. Fisheries and Aquaculture ................................................................................................................................................. 676

10.5.1.4. Mining and Quarrying ....................................................................................................................................................... 676

10.5.2. Secondary Economic Activities .......................................................................................................................................................... 677

10.5.2.1. Manufacturing ................................................................................................................................................................... 677

10.5.2.2. Construction and Housing ................................................................................................................................................. 677

Table of Contents

661

Key Economic Sectors and Services Chapter 10

10

10.6. Recreation and Tourism .......................................................................................................................................... 677

10.6.1. Recreation and Tourism Demand ...................................................................................................................................................... 677

10.6.1.1. Recreation ......................................................................................................................................................................... 677

10.6.1.2. Tourism .............................................................................................................................................................................. 678

10.6.2. Recreation and Tourism Supply ......................................................................................................................................................... 679

10.6.3. Market Impacts ................................................................................................................................................................................. 679

10.7. Insurance and Financial Services ............................................................................................................................ 680

10.7.1. Main Results of the Fourth Assessment Report and IPCC Special Report on Managing the Risks of Extreme Events

and Disasters to Advance Climate Change Adaptation on Insurance ................................................................................................ 680

10.7.2. Fundamentals of Insurance Covering Weather Hazards .................................................................................................................... 680

10.7.3. Observed and Projected Insured Losses from Weather Hazards ........................................................................................................ 680

10.7.4. Fundamental Supply-Side Challenges and Sensitivities .................................................................................................................... 683

10.7.5. Products and Systems Responding to Changes in Weather Risks ..................................................................................................... 684

10.7.6. Governance, Public-Private Partnerships, and Insurance Market Regulation ..................................................................................... 686

10.7.7. Financial Services .............................................................................................................................................................................. 686

10.7.8. Summary .......................................................................................................................................................................................... 687

10.8. Services Other than Tourism and Insurance ............................................................................................................ 687

10.8.1. Sectors Other than Health ................................................................................................................................................................ 687

10.8.2. Health ............................................................................................................................................................................................... 687

10.9. Impacts on Markets and Development ................................................................................................................... 689

10.9.1. Effects of Markets ............................................................................................................................................................................. 689

10.9.2. Aggregate Impacts ........................................................................................................................................................................... 690

10.9.3. Social Cost of Carbon ....................................................................................................................................................................... 690

10.9.4. Effects on Growth ............................................................................................................................................................................. 691

10.9.4.1. The Rate of Economic Growth ........................................................................................................................................... 691

10.9.4.2. Poverty Traps ..................................................................................................................................................................... 692

10.9.5. Summary .......................................................................................................................................................................................... 692

10.10. Summary; Research Needs and Priorities .............................................................................................................. 693

References ......................................................................................................................................................................... 694

Frequently Asked Questions

10.1: Why are key economic sectors vulnerable to climate change? ......................................................................................................... 664

10.2: How does climate change impact insurance and financial services? ................................................................................................ 680

10.3: Are other economic sectors vulnerable to climate change too? ....................................................................................................... 688

662

Chapter 10 Key Economic Sectors and Services

10

Executive Summary

This chapter assesses the implications of climate change on economic activity in key economic sectors and services, on economic welfare, and

on economic development.

For most economic sectors, the impact of climate change will be small relative to the impacts of other drivers (medium evidence,

high agreement). Changes in population, age, income, technology, relative prices, lifestyle, regulation, governance, and many other aspects of

socioeconomic development will have an impact on the supply and demand of economic goods and services that is large relative to the impact

of climate change. {10.10}

Climate change will reduce energy demand for heating and increase energy demand for cooling in the residential and commercial

sectors (robust evidence, high agreement); the balance of the two depends on the geographic, socioeconomic, and technological conditions.

Increasing income will allow people to regulate indoor temperatures to a comfort level that leads to fast growing energy demand for air

conditioning even in the absence of climate change in warm regions with low income levels at present. Energy demand will be influenced by

changes in demographics (upward by increasing population and decreasing average household size), lifestyles (upward by larger floor area of

dwellings), the design and heat insulation properties of the housing stock, the energy efficiency of heating/cooling devices, and the abundance

and energy efficiency of other electric household appliances. The relative importance of these drivers varies across regions and will change over

time. {10.2}

Climate change will affect different energy sources and technologies differently, depending on the resources (water flow, wind,

insolation), the technological processes (cooling), or the locations (coastal regions, floodplains) involved (robust evidence, high

agreement).

Gradual changes in various climate attributes (temperature, precipitation, windiness, cloudiness, etc.) and possible changes in the

frequency and intensity of extreme weather events will progressively affect operation over time. Climate-induced changes in the availability

and temperature of water for cooling are the main concern for thermal and nuclear power plants. Several options are available to cope with

reduced water availability but at higher cost; however, decreased efficiency of thermal conversion remains a primary concern. Similarly, already

available or newly developed technological solutions allow firms to reduce the vulnerability of new structures and enhance the climate suitability

of existing energy installations. {10.2}

Climate change may influence the integrity and reliability of pipelines and electricity grids (medium evidence, medium agreement).

Pipelines and electric transmission lines have been designed and operated for more than a century in diverse and often extreme climatic conditions

on land from hot deserts to permafrost areas and increasingly at sea. Owing to the private nature and high economic value to the energy sector,

they have been designed to higher tolerance levels than most transportation infrastructure. Climate change may require changes in design

standards for the construction and operation of pipelines and power transmission and distribution lines. Adopting existing technology from

other geographical and climatic conditions may reduce the cost of adapting new infrastructure as well as the cost of retrofitting existing

pipelines and grids to the changing climate, sea level, and weather conditions, which is likely to become more intense over time. {10.2}

Climate change will have impacts, positive and negative and varying in scale and intensity, on water supply infrastructure and

water demand (robust evidence, high agreement), but the economic implications are not well understood.

Economic impacts

include flooding, scarcity, and cross-sectoral competition. Flooding can have major economic costs, both in term of impacts (capital destruction,

disruption) and adaptation (construction, defensive investment). Water scarcity and competition for water—driven by institutional, economic,

or social factors—may mean that water is not available in sufficient quantity or quality for some uses or locations. {10.3}

Climate change may negatively affect transport infrastructure (limited evidence, high agreement). Transport infrastructure

malfunctions if the weather is outside the design range, which would happen more frequently as the climate continues to change. All

infrastructure is vulnerable to freeze-thaw cycles. Paved roads are particularly vulnerable to temperature extremes, and unpaved roads and

bridges to precipitation extremes. Transport infrastructure on ice or permafrost is especially vulnerable. {10.4}

663

10

Key Economic Sectors and Services Chapter 10

Climate change will affect tourism resorts, particularly ski resorts, beach resorts, and nature resorts (robust evidence, high

agreement) and tourists may spend their holidays at higher altitudes and latitudes (medium evidence, high agreement).

The

economic implications of climate change-induced changes in tourism demand and supply entail gains for countries closer to the poles and

higher up the mountains and losses for other countries. The demand for outdoor recreation is affected by weather and climate, and impacts will

vary geographically and seasonally. {10.6}

Climate change will affect insurance systems (robust evidence, high agreement). More frequent and/or intensive weather disasters as

projected for some regions/hazards will increase losses and loss variability in various regions and challenge insurance systems to offer affordable

coverage while raising more risk-based capital, particularly in low- and middle-income countries. Economic-vulnerability reduction through

insurance has proven effective. Large-scale public-private risk prevention initiatives and government insurance of the non-diversifiable portion

of risk offer example mechanisms for adaptation. Commercial reinsurance and risk-linked securitization markets also have a role in ensuring

financially resilient insurance and risk transfer systems. {10.7}

Climate change will affect the health sector (medium evidence, high agreement) through increases in the frequency, intensity, and

extent of extreme weather events as well as increasing demands for health care services and facilities, including public health programs,

disease prevention activities, health care personnel, infrastructure, and supplies related to treatment of infectious diseases and temperature-

related events. {10.8}

Well-functioning markets provide an additional mechanism for adaptation and thus tend to reduce negative impacts and

increase positive ones for any specific sector or country (medium evidence, high agreement). The impacts of climate on one sector of

the economy of one country in turn affect other sectors and other countries though product and input markets. Markets increase overall welfare,

but not necessarily welfare in every sector and country. {10.9}

The impacts of climate change may decrease productivity and economic growth, but the magnitude of this effect is not well

understood (limited evidence, high agreement). Climate could be one of the causes why some countries are trapped in poverty, and

climate change may make it harder to escape poverty. {10.9}

Global economic impacts from climate change are difficult to estimate. Economic impact estimates completed over the past 20 years

vary in their coverage of subsets of economic sectors and depend on a large number of assumptions, many of which are disputable, and many

estimates do not account for catastrophic changes, tipping points, and many other factors. With these recognized limitations, the incomplete

estimates of global annual economic losses for additional temperature increases of ~2°C are between 0.2 and 2.0% of income (±1 standard

deviation around the mean) (medium evidence, medium agreement). Losses are more likely than not to be greater, rather than smaller, than

this range (limited evidence, high agreement). Additionally, there are large differences between and within countries. Losses accelerate with

greater warming (limited evidence, high agreement), but few quantitative estimates have been completed for additional warming around 3°C

or above. Estimates of the incremental economic impact of emitting carbon dioxide lie between a few dollars and several hundreds of dollars

per tonne of carbon (robust evidence, medium agreement). Estimates vary strongly with the assumed damage function and discount rate.

{10.9}

Not all key economic sectors and services have been subject to detailed research. Few studies have evaluated the possible impacts of

climate change on mining, manufacturing, or services (apart from health, insurance, and tourism). Further research, collection, and access to

more detailed economic data and the advancement of analytic methods and tools will be required to assess further the potential impacts of

climate on key economic systems and sectors. {10.5, 10.8, 10.10}

664

Chapter 10 Key Economic Sectors and Services

10

10.1. Introduction and Context

This chapter discusses the implications of climate change on key economic

sectors and services, for example, economic activity. Other chapters discuss

i

mpacts from a physical, chemical, biological, or social perspective.

Economic impacts cannot be isolated; therefore, there are a large

number of cross-references to sections in other chapters of this report.

In some cases, particularly agriculture, the discussion of the economic

impacts is integrated with the other impacts.

Focusing on the potential impact of climate change on economic activity,

this chapter addresses questions such as: How does climate change

affect the demand for a particular good or service? What is the impact

on its supply? How do supply and demand interact in the market? What

are the effects on producers and consumers? What is the effect on the

overall economy, and on welfare?

An inclusive approach was taken, discussing all sectors of the economy.

Section SM10.1 found in this chapter’s on-line supplementary material

shows the list of sectors according to the International Standard Industrial

Classification. This assessment reflects the breadth and depth of the

state of knowledge across these sectors; many of which have not been

evaluated in the literature. We extensively discuss five sectors: energy

(Section 10.2), water (Section 10.3), transport (Section 10.4), tourism

(Section 10.6), and insurance (Section 10.7). Other primary and secondary

sectors are discussed in Section 10.5, and Section 10.8 is devoted to

other service sectors. Food and agriculture is addressed in Chapter 7.

Sections 10.2 through 10.8 discuss individual sectors in isolation. Markets

are connected, however. Section 10.9 therefore assesses the implications

of changes in any one sector on the rest of the economy. It also discusses

the effect of the impacts of climate change on economic growth and

development. Chapter 19 assesses the impact of climate change on

economic welfare—that is, the sum of changes in consumer and

producer surplus, including for goods and services not traded within the

formal economy. This is not attempted here. The focus is on economic

activity. Section 10.10 discusses whether there may be vulnerable sectors

that have yet to be studied.

P

revious assessment reports by the IPCC did not have a chapter on “key

economic sectors and services.” Instead, the material assembled here

was spread over a number of chapters. The Fourth Assessment Report

(AR4) is referred to in the context of the sections below. In some cases,

however, the literature is so new that previous IPCC reports did not

discuss these impacts at any length.

10.2. Energy

Studies conducted since AR4 and assessed here confirm the main insights

about the impacts of climate change on energy demand as reported in

the Second Assessment Report (SAR; Acosta et al., 1995) and reinforced

by the Third Assessment Report (TAR; Scott et al., 2001) and AR4 (Wilbanks

et al., 2007): ceteris paribus, in a warming world, energy demand for

heating will decline and energy demand for cooling will increase; the

balance of the two depends on the geographic, socioeconomic, and

technological conditions. The relative importance of temperature changes

among the drivers of energy demand varies across regions and will

change over time. Earlier IPCC assessments did not write much about

energy supply, but an increasing number of studies now explore its

vulnerability, impacts, and adaptation options (Karl et al., 2009; Troccoli,

2010; Ebinger and Vergara, 2011). The energy sector will be transformed

by climate policy (WGIII AR5 Chapter 7) but impacts of climate changes

too will be important for secure and reliable energy supply.

10.2.1. Energy Demand

Most studies conducted since AR4 explore the impacts of climate

change on residential energy demand, particularly electricity (Mideksa

and Kallbekken, 2010). Some studies encompass the commercial sector

as well but very few deal with industry and agriculture. In addition to a

few global studies based on global energy or integrated assessment

models, the new studies tend to focus on specific countries or regions

(Zachariadis, 2010; Olonscheck et al., 2011), rely on improved methods

(more advanced statistical techniques; de Cian et al., 2013) and data (both

Frequently Asked Questions

FAQ 10.1 | Why are key economic sectors vulnerable to climate change?

Many key economic sectors are affected by long-term changes in temperature, precipitation, sea level rise, and

extreme events, all of which are impacts of climate change. For example, energy is used to keep buildings warm in

winter and cool in summer. Changes in temperature would thus affect energy demand. Climate change also affects

energy supply through the cooling of thermal plants, through wind, solar, and water resources for power, and

through transport and transmission infrastructure. Water demand increases with temperature but falls with rising

carbon dioxide (CO

2

) concentrations as CO

2

fertilization improves the water use efficiency plant respiration. Water

supply depends on precipitation patterns and temperature, and water infrastructure is vulnerable to extreme

weather, while transport infrastructure is designed to withstand a particular range of weather conditions, and climate

change would expose this infrastructure to weather outside historical design criteria. Recreation and tourism are

weather-dependent. As holidays are typically planned in advance, tourism depends on the expected weather and

will thus be affected by climate change. Health care systems are also impacted, as climate change affects a number

of diseases and thus the demand for and supply of health care.

665

10

Key Economic Sectors and Services Chapter 10

h

istorical and regional climate projections), and many of them explicitly

include non-climatic drivers of energy demand (e.g., sources). A few

studies consider changes in demand together with changes in climate-

dependent energy sources, such as hydropower (Hamlet et al., 2010).

Sorting the assessed studies according to the present climate (represented

by mean annual temperature based on 1971–2000 climatology) and

current income (represented by gross domestic product (GDP) per capita

in 2009), the general patterns are as follows. In countries and regions

with already high incomes, climate-related changes in energy demand

will be driven primarily by increasing temperatures. In countries/regions

with high incomes and warm climates, increasing temperatures will be

associated with heavier use of air conditioning. In countries/regions with

high incomes and temperate and cold climates, increasing temperatures

will result in lower demands for various energy forms (electricity, gas,

coal, oil). Increasing incomes will play a marginal role in these countries

and regions. In contrast, changes in income will be the main driver of

increasing demand for energy (mainly electricity for air conditioning

and transportation fuels) in present-day low-income countries in warm

climates. Neither indicator is ideal because country-level mean annual

temperatures for large countries can hide large regional differences and

average incomes may conceal large disparities, but they help cluster

the national and regional studies in the search for general finding.

At the global scale, energy demand for residential air conditioning in

summer is projected to increase rapidly in the 21st century under the

reference climate change scenario (medium population and economic

growth globally, but faster economic growth in developing countries;

no mitigation policies in addition to those in place in 2008) by the Targets

IMAGE Energy Regional Model/Integrated Model to Assess the Global

Environment (TIMER/IMAGE) model (Isaac and Van Vuuren, 2009). The

increase is from nearly 300 TWh in 2000 to about 4000 TWh in 2050

and more than 10,000 TWh in 2100, about 75% of which is due to

increasing income in emerging market countries and 25% is due to

climate change. Energy demand for heating in winter increases too,

but much less rapidly, since in most regions with the highest need for

heating, incomes are already high enough for people to heat their

homes to the desired comfort level (except in some poor households).

In these regions, energy demand for heating will decrease.

These general patterns and especially the quantitative results of the

projected shifts in energy and electricity demand can be modified by

many other factors. In addition to changes in temperatures and incomes,

the actual energy demand will be influenced by changes in demographics

(upward by increasing population and decreasing average household

size, mixed effects from urbanization), lifestyles (upward by larger floor

area of dwellings), building codes and regulations for the design and

insulation of the housing stock, the energy efficiency of heating/cooling

devices, the abundance and energy efficiency of other electric household

appliances, the price of energy, and so forth.

10.2.2. Energy Supply

Changes in climate attributes (temperature, precipitation, windiness,

cloudiness, etc.) will affect different energy sources and technologies

differently. Gradual climate change will progressively affect the operation

o

f energy installations and infrastructure over time. Possible changes

in the frequency and intensity of extreme weather events (EWEs) as a

result of climate change represent a different kind of hazard for them.

(EWEs are weather events that are rare at a particular place and time

of the year; they are usually defined as rare or rarer than the 10th and

90th percentiles of a probability density function estimated from

observations; see Glossary). Rummukainen (2013) and Mika (2013)

summarize recent trends and prospects relevant for the energy sector.

This section assesses the most important impacts and adaptation options

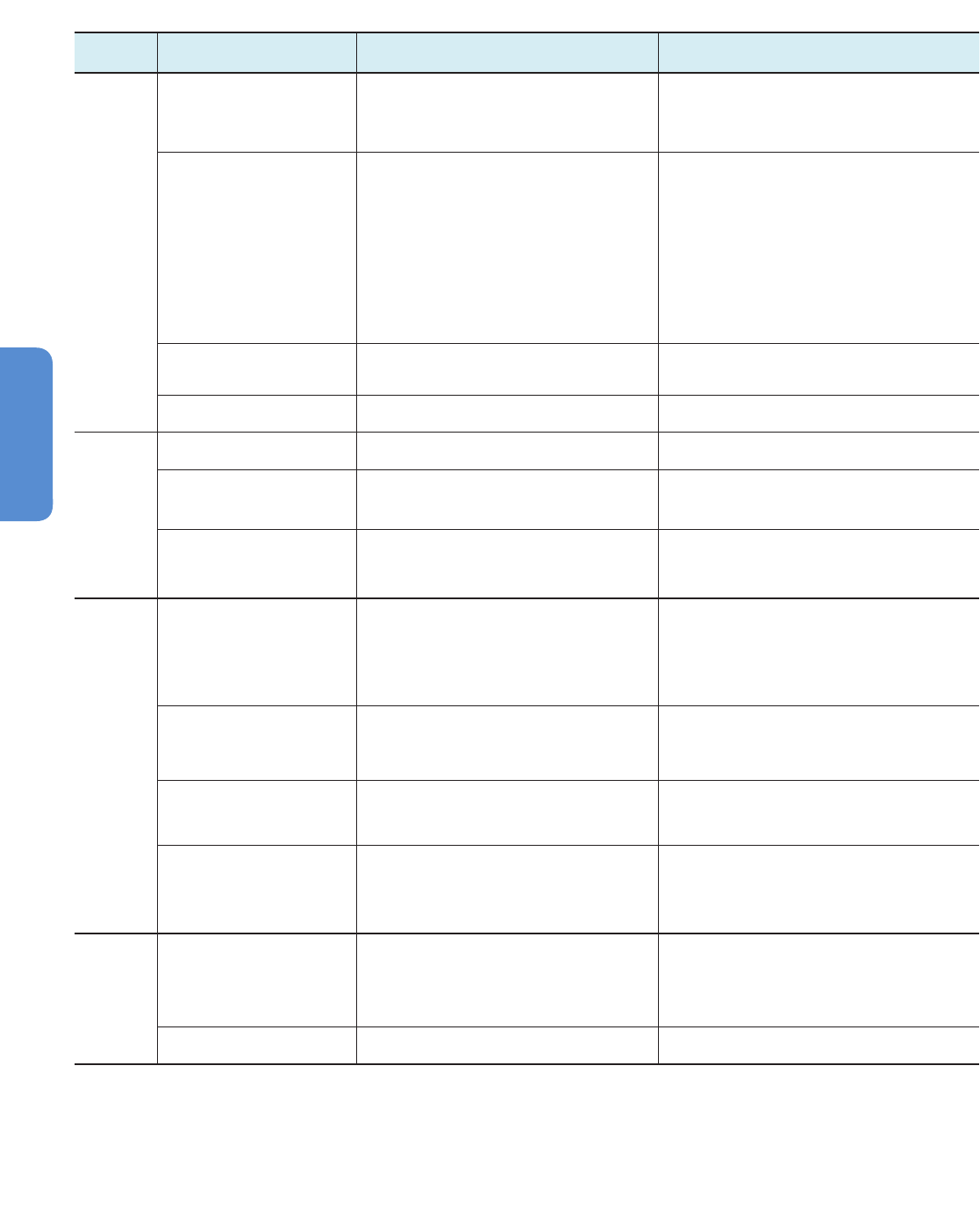

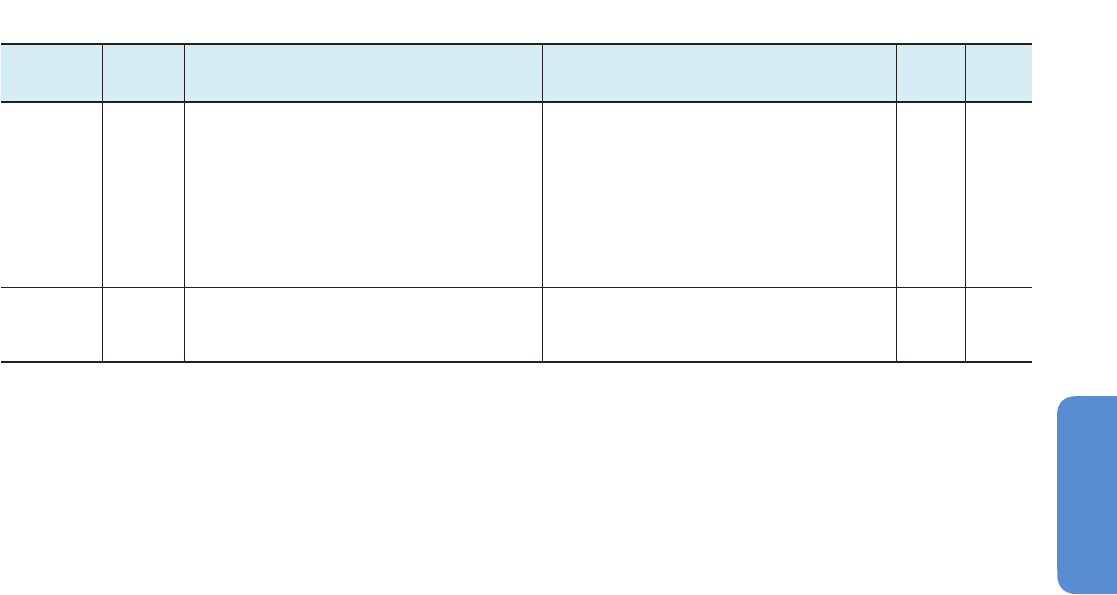

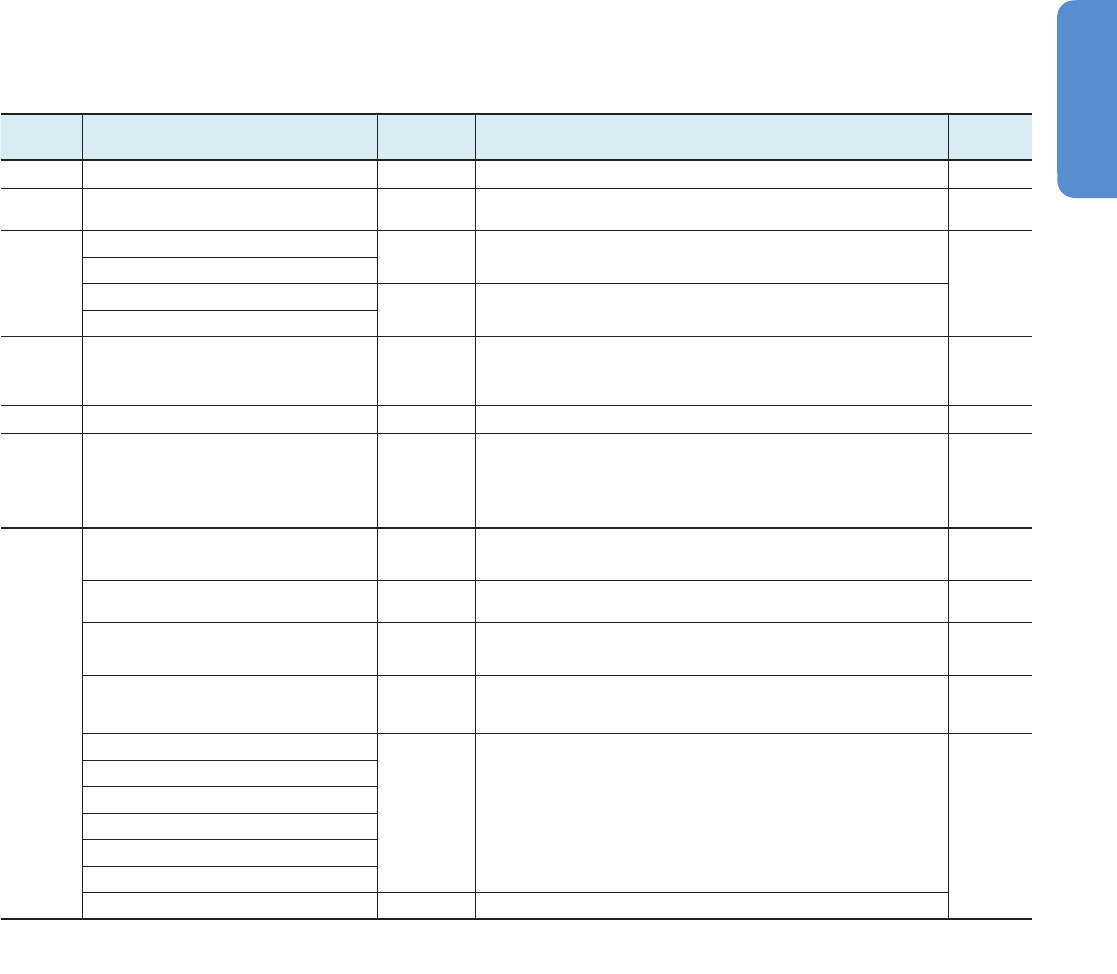

in both categories. Table 10-1 provides an overview.

Currently, thermal power plants provide about 80% of global electricity

and their share is projected to remain high in most mitigation scenarios

(IEA, 2010a). Thermal power plants can be designed to operate under

diverse climatic conditions, from the cold Arctic to the hot tropical regions

and are normally well adapted to the prevailing conditions. However,

they might face new challenges and will need to respond by hard

(design or structural methods) or soft (operating procedures) measures

as a result of climate change.

A general impact of climate change on thermal power generation

(including combined heat and power) is the decreasing efficiency of

thermal conversion as a result of rising temperature that cannot be

offset per se. Yet there is much room to improve the efficiency of

currently operating subcritical steam power plants (IEA, 2010b). As new

materials allow higher operating temperatures in coal-fired power plants

(Gibbons, 2012), supercritical and ultra-supercritical steam-cycle plants

(operating at much higher pressure and temperature conditions than

conventional power plants) will reach even higher efficiency that can

more than compensate the efficiency losses due to higher temperatures.

Yet in the absence of climate change, these efficiency gains from

improved technology would reduce the costs of energy, so there is still

a net economic loss due to climate change. Another problem facing

thermal power generation in many regions is the decreasing volume

and increasing temperature of water for cooling, leading to reduced

power generation, operation at reduced capacity, and even temporary

shutdown of power plants (Ott and Richter, 2008; Hoffmann et al., 2010;

IEA, 2012; Sieber, 2013). Both problems will be exacerbated if carbon

dioxide (CO

2

) capture and handling equipment is added to fossil-fired

power plants: energy efficiency declines by 8 to 14% (IPCC, 2005) and

water requirement per MWh electricity generated can double (Macknick

et al., 2011). Using partial equilibrium river basin models, (Hurd et al.,

2004; Strzepek et al., 2013) estimate USA welfare loses due to thermal

cooling water changes at US$622 million per year up to 2100, a 6.5%

welfare loss in the energy sector. Van Vliet et al. (2012) find that the

southeastern United States, Europe, eastern China, southern Africa, and

southern Australia could potentially be affected by reduced water

available for thermoelectric power and drinking water, inducing changes

to dry or hybrid cooling (with concomitant loss in electric output), or plant

shut downs, with associated impacts on local and regional economic

activity.

Adaptation possibilities range from relatively simple and low-cost

options such as exploiting non-traditional water sources and re-using

process water to measures such as installing dry cooling towers, heat

pipe exchangers, and regenerative cooling (Ott and Richter, 2008; De

Bruin et al., 2009), all which increase costs. Water use regulation, heat

666

Chapter 10 Key Economic Sectors and Services

10

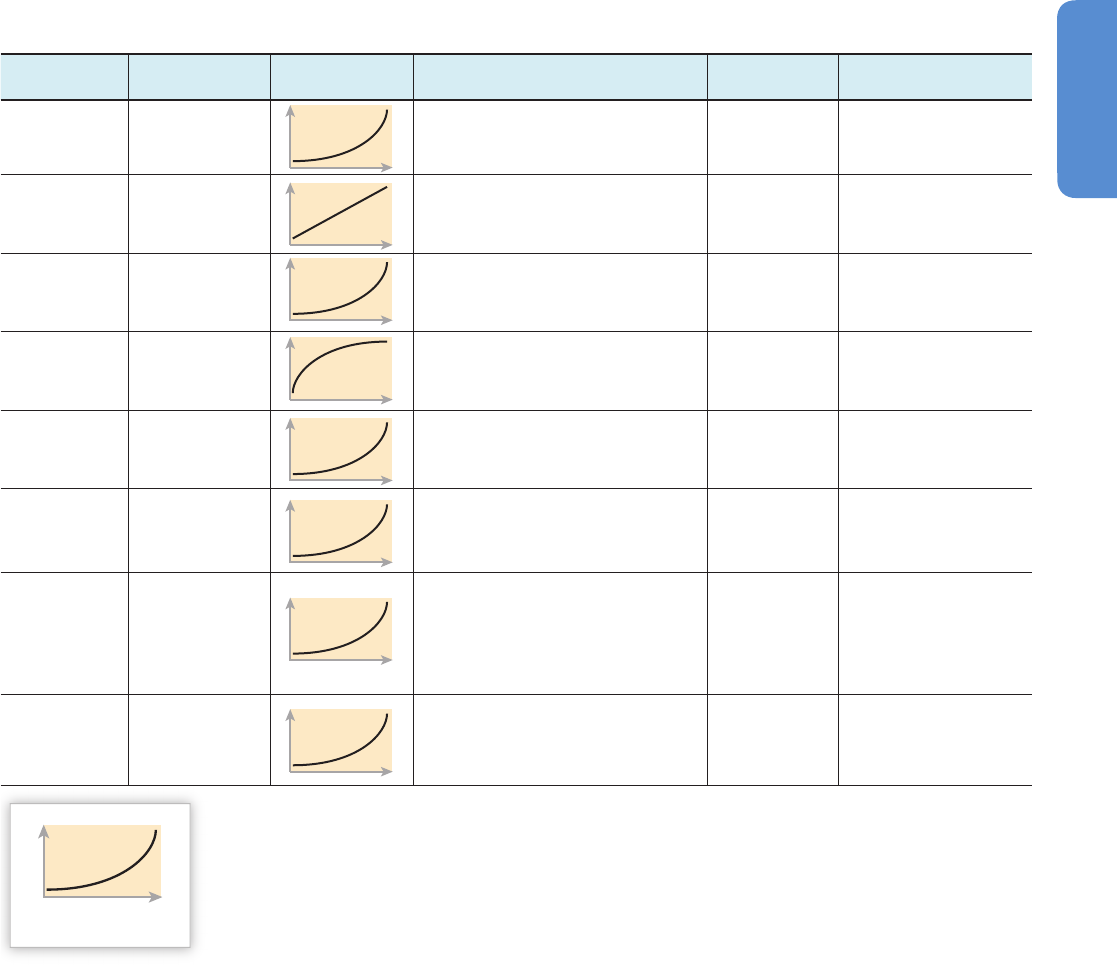

Technology

Changes in climatic

or related attributes

Possible impacts Adaptation options

Thermal

and nuclear

power plants

Increasing air temperature Reduces effi ciency of thermal conversion by 0.1– 0.2% in

t

he USA; by 0.1– 0.5% in Europe, where the capacity loss

i

s estimated in the range of 1– 2% per 1°C temperature

increase, accounting for decreasing cooling effi ciency and

r

educed operation level /shutdown

Siting at locations with cooler local climates where possible

Changing (lower) precipitation and

increasing air temperature increases

t

emperature and reduces the

availability of water for cooling.

Less power generation; annual average load reduction by

0.1– 5.6% depending on scenario

Use of non-traditional water sources (e.g., water from oil and

gas fi elds, coal mines and treatment, treated sewage); re-use

o

f process water from fl ue gases (can cover 25 – 37% of the

power plant’s cooling needs), coal drying, condensers (drier coal

h

as higher heating value, cooler water enters cooling tower),

fl ue-gas desulfurization; using ice to cool air before entering the

gas turbine increases effi ciency and output, melted ice used in

c

ooling tower; condenser mounted at the outlet of cooling tower

to reduce evaporation losses (by up to 20%). Alternative cooling

t

echnologies: dry cooling towers, regenerative cooling, heat

pipe exchangers; costs of retrofi tting cooling options depend on

f

eatures of existing systems, distance to water, required additional

equipment, estimated at US$250,000 – 500,000 per megawatt

Increasing frequency of extreme hot

t

emperatures

Exacerbating impacts of warmer conditions: reduced thermal

a

nd cooling effi ciency; limited cooling water discharge;

overheating buildings; self-ignition of coal stockpiles

Cooling of buildings (air conditioning) and of coal stockpiles

(

water spraying)

D

rought: reduced water availability Exacerbating impacts of warmer conditions, reduced

operation and output, shutdown

S

ame as reduced water availability under gradual climate change

Hydropower

I

ncrease /decrease in average water

a

vailability

I

ncreased / reduced power output Schedule release to optimize income

Changes in seasonal and inter-annual

variation in infl ows (water availability)

Shifts in seasonal and annual power output; fl oods and lost

output in the case of higher peak fl ows

Soft: adjust water management

Hard: build additional storage capacity, improve turbine runner

capacity

Extreme precipitation causing fl oods Direct and indirect (by debris carried from fl ooded areas)

damage to dams and turbines, lost output due to releasing

water through bypass channels

Soft: adjust water management

Debris removal

Hard: increase storage capacity

Solar energy

Increasing mean temperature Improving performance of TH (especially in colder regions),

reducing effi ciency of PV and CSP with water cooling; PV

effi ciency drops by ~0.5% per 1°C temperature increase

for crystalline silicon and thin-fi lm modules as well, but

performance varies across types of modules, with thin fi lm

modules performing better; long-term exposure to heat

causes faster aging.

Changing cloudiness Increasing unfavorable (reduced output), decreasing

benefi cial (increased output) for all types, but evacuated tube

collectors for TH can use diffuse insolation.

CSP more vulnerable (cannot use diffuse light)

Apply rougher surface for PV panels that use diffuse light better;

optimize fi xed mounting angle for using diffuse light, apply

tracking system to adjust angle for diffuse light conditions;

install / increase storage capacity

Hot spells Material damage for PV, reduced output for PV and CSP;

CSP effi ciency decreases by 3 – 9% as ambient temperature

increases from 30 to 50°C and drops by 6% (tower) to 18%

(trough) during the hottest 1% of time

Cooling PV panels passively by natural air fl ows or actively by

forced air or liquid coolants

Hail Material damage to TH: evacuated tube collectors are more

vulnerable than fl at plate collectors.

Fracturing as glass plate cover, damage to photoactive

material

Flat plate collectors: using reinforced glass to withstand

hailstones of 35 mm (all of 15 tested) or even 45 mm (10 of 15

tested); only 1 in 26 evacuated tube collectors withstood 45-mm

hailstones.

Increase protection to current standards or beyond them

Wind power

Windiness: total wind resource

(multi-year annual mean wind power

densities); likely to remain within ±50%

of current values in Europe and North

America; within ±25% of 1979 – 2000

historical values in contiguous USA

Change in wind power potential Site selection

Wind speed extremes: gust, direction

change, shear

Structural integrity from high structural loads; fatigue,

damage to turbine components; reduced output

Turbine design, lidar-based protection

Table 10-1 | Main projected impacts of climate change and extreme weather events on energy supply and the related adaptation options.

Notes: CSP = concentrating solar power; PV = photovoltaic; TH = thermal heating.

Sources: EPA (2001); Parkpoom et al. (2005); Norton (2006); Pryor et al. (2006); Walter et al. (2006); Christensen and Busuioc (2007); DOE (2007); NETL National Energy

Technology Laboratory (2007); Schaefl i et al. (2007); Bloom et al. (2008); Feeley III et al. (2008); Haugen and Iversen (2008); Leckebusch et al. (2008); Markoff and Cullen (2008);

Ott and Richter (2008); Sailor et al. (2008); Droogers (2009); Förster and Lilliestam (2009); Honeyborne (2009); Kurtz et al. (2009); SPF (2009); Hoffmann et al. (2010); Pryor and

Barthelmie (2010, 2011, 2013); Pryor and Schoof (2010); Kurtz et al. (2011); Linnerud et al. (2011); Mukheibir (2013); Patt et al. (2013); Sieber (2013); Williams (2013).

667

10

Key Economic Sectors and Services Chapter 10

d

ischarge restrictions, and occasional exemptions might be an institutional

adaptation (Eisenack and Stecker, 2012). Though it is easier to plan for

changing climatic conditions and select the site and the conforming

cost-efficient cooling technology for new builds, response options are

more limited for existing power plants, especially for those toward the

end of their economic lifetime.

Climate change impacts on thermal efficiency and cooling water

availability affect nuclear power plants as well but the safety regulations

are stricter than for fossil-fired plants (Williams and Toth, 2013). A range

of alternative cooling options are available to deal with water deficiency,

ranging from re-using wastewater and recovering evaporated water

(Feeley III et al., 2008) to installing dry cooling (EPA, 2001).

The implications of EWEs for nuclear plants can be severe if not properly

addressed. Reliable interconnection (on-site power and instrumentation

connections) of intact key components (reactor vessel, cooling equipment,

control instruments, back-up generators) is indispensable for the safe

operation and/or shutdown of a nuclear reactor. For most of the existing

global nuclear fleet, a reliable connection to the grid for power to run

cooling systems and control instruments in emergency situations is

another crucial item (IAEA, 2011). Several EWEs can damage the

components or disrupt their interconnections. Preventive and protective

measures include technical and engineering solutions (circuit insulation,

shielding, flood protection) and adjusting operation to extreme conditions

(reduced capacity, shutdown) (Williams and Toth, 2013).

Hydropower is by far the largest of renewable energy sources in the

current electricity mix. It is projected to remain important in the future,

irrespective of the climate change mitigation targets in many countries

(IEA, 2010a,b). The resource base of hydropower is the hydrologic cycle

driven by prevailing climate and topology. The former makes the

resource base and hence hydropower generation highly dependent on

future changes in climate and related changes in extreme weather

events (Ebinger and Vergara, 2011; Mukheibir, 2013).

Assessing the impacts of climate change on hydropower generation is

highly complex. A series of nonlinear and region-specific changes in

mean annual and seasonal precipitation and temperatures, the resulting

evapotranspiration losses, shifts in the share of precipitation falling as

snow and the timing of its release from high elevation, and the climate

response of glaciers make resource estimates difficult (see Chapters 2

and 3) while regional changes in water demand due to changes in

population and economic activities (especially irrigation demand for

agriculture) present competition for water resources that are hard to

project (see Section 10.3). Further complications stem from the possibly

increasing need to combine hydropower generation with changing flood

control and ecological (minimum dependable flow) objectives induced

by changing climate regimes. For hydropower locations, adaption to

climate change to maintain output has been reported; in Ethiopia, Block

and Strzepek (2012) report that capital expenditures through 2050 may

either decrease by approximately 3% under extreme wet scenarios or

increase by up to 4% under a severe dry scenario. In the Zambezi river

basin, hydropower may fall by 10% by 2030, and by 35% by 2050 under

the driest scenario (Strzepek et al., 2012). Lower generation is likely in

the upstream power stations of the Zambezi basin and increases are

likely downstream (Fant et al., 2013).

F

ocusing on the possible impacts of climate change on hydroelectricity

and the adaptation options in the sector in response to the changes in

the amount, the seasonal and interannual variations of available water,

and in other demands, the conclusion from the literature is that the

overall impacts of climate change and EWEs on hydropower generation

by 2050 is expected to be slightly positive in most regions (e.g., in Asia,

by 0.27%) and negative in some (e.g., in Europe, by –0.16%), with

diverging patterns across regions, watersheds within regions, and even

river basins within watersheds (IPCC, 2011). Adaptation responses and

planning tools for long-term hydrogeneration may need to be enhanced

to cope with slow but persistent shifts in water availability. Short-term

management models may need to be enhanced to deal with the impacts

of EWEs. A series of hard (raising dam walls, adding bypass channels)

and soft (adjusting water release) measures are available to protect the

related infrastructure (dams, channels, turbines, etc.) and optimize incomes

by timing generation when electricity prices are high (Mukheibir, 2013).

Solar energy is expected to increase from its currently small share in

the global energy balance across a wide range of mitigation scenarios

(IEA, 2008, 2009, 2010a,b). The three main types of technologies for

harnessing energy from insolation include thermal heating (TH; by flat

plate, evacuated tube, and unglazed collectors), photovoltaic (PV) cells

(crystalline silicon and thin film technologies), and concentrating solar

power (CSP; power tower and power trough producing heat to drive a

steam turbine for generating electricity). The increasing body of literature

exploring the vulnerability and adaptation options of solar technologies

to climate change and EWEs is reviewed by Patt et al. (2013).

All types of solar energy are sensitive to changes in climatic attributes

that directly or indirectly influence the amount of insolation reaching

them. If cloudiness increases under climate change (WGI AR5 Chapters

11, 12), the intensity of solar radiation and hence the output of heat or

electricity would be reduced. Efficiency losses in cloudy conditions are

less for technologies that can operate with diffuse light (evacuated tube

collectors for TH, PV collectors with rough surface). Since diffuse light

cannot be concentrated, CSP output would cease under cloudy conditions

but the easy and relatively inexpensive possibility to store heat reduces

this vulnerability if sufficient volume of heat storage is installed (Khosla,

2008; Richter et al., 2009).

The exposure of sensitive material to harsh weather conditions is another

source of vulnerability for all types of solar technologies. Windstorms

can damage the mounting structures directly and the conversion units

by flying debris, whereby technologies with smaller surface areas are

less vulnerable. Hail can also cause material damage and thus reduced

output and increased need for repair. Depending on regional conditions,

strong wind can deposit sand and dust on the collector’s surface, reducing

efficiency and increasing the need for cleaning.

Climate change and EWE hazards per se do not pose any particular

constraints for the future deployment of solar technologies. Technological

development continues in all three solar technologies toward new

designs, models, and materials. An objective of these development efforts

is to make the next generation of solar technologies less vulnerable to

existing physical challenges, changing climatic conditions, and the

impacts of EWEs. Technological development also results in a diverse

portfolio of models to choose from according to the climatic and

668

Chapter 10 Key Economic Sectors and Services

10

w

eather characteristics of the deployment site. These development

efforts can be integrated in addressing the key challenge for solar

technologies today: reducing the costs.

Harnessing wind energy for power generation is an important part of

the climate change mitigation portfolio in many countries. Assessing

the possible impacts of climate change and EWEs and identifying

possible adaptation responses for wind energy is complicated by the

complex dynamics characterizing this generation source. Relevant

attributes of climate are expected to change; the technology is evolving

(blade design, other components); see Kong et al. (2005) and Barlas and

Van Kuik (2010); there is an increasing deployment offshore and a

transition to larger turbines (Garvey, 2010) and to larger sites (multi

megawatt arrays) (Barthelmie et al., 2008).

The key question concerning the impacts of a changing climate regime

on wind power is related to the resource base: how climate change will

rearrange the temporal (inter- and intra-annual variability) and spatial

(geographical distribution) characteristics of the wind resource. In the

next few decades, wind resources (measured in terms of multi-annual

wind power densities) are estimated to remain within the ±50% of the

mean values over the past 20 years in Europe and North America (Pryor

and Barthelmie, 2010). The wide range of the estimates results from the

circulation and flow regimes in different General Circulation Models

(GCMs) and Regional Climate Models (RCMs) (Bengtsson et al., 2006;

Pryor and Barthelmie, 2010). A set of four GCM-RCM combinations for

the period 2041–2062 indicates that average annual mean energy

density will be within ±25% of the 1979–2000 values in all 50-km grid

cells over the contiguous USA (Pryor et al., 2011; Pryor and Barthelmie,

2013). Yet, little is known about changes in the interannual, seasonal,

or diurnal variability of wind resources.

Wind turbines already operate in diverse climatic and weather conditions.

As shown in Table 10-1, siting, design, and engineering solutions are

available to cope with various impacts of gradual changes in relevant

climate attributes over the coming decades. The requirements to

withstand extreme loading conditions resulting from climate change

are within the safety margins prescribed in the design standards,

although load from combinations of extreme events may exceed the

design thresholds (Pryor and Barthelmie, 2013). In summary, the wind

energy sector does not face insurmountable challenges resulting from

climate change.

In the coal fuel cycle, vulnerability in mining depends on mining method.

Surface mining might be particularly affected by high precipitation

extremes and related floods and erosion, and temperature extremes,

especially extreme cold that might encumber extraction for some time,

whereas impacts on coal cleaning and operation of underground mines

will probably be less severe (Ekman, 2013). Changes in drainage and

runoff regulation for on-site coal storage as well as in coal handling

might be required due to the increased moisture content of coal and

more energy might be required for coal drying before transportation

(CCSP, 2007). At the back end of the fuel cycle, the management of fly-

ash, bottom ash, and boiler slag may need to be modified in response

to changes in some EWE patterns such as wind, precipitation, and

floods. Impacts on biomass-based energy sources are discussed in

Chapter 7 of this report.

C

limate- and weather-related hazards in the oil and gas sector include

tropical cyclones with potentially severe effects on offshore platforms

and onshore infrastructure as well, leading to more frequent production

interruptions and evacuation (Cruz and Krausmann, 2013). Gradual

changes in air temperature and precipitation are projected to generate

risk and opportunities for the oil and gas industry. For example, new

areas for oil and gas exploration could open in the Arctic, potentially

increasing the technically recoverable resource base (Cruz and

Krausmann, 2013). Reduced sea ice thickness and coverage might open

new shipping routes, thus reducing shipping costs, while ice scour and

ice pack loading on marine structures would increase. However, most

changes involve increased risks, such as thawing permafrost would

increase construction costs on unstable ground relative to ice-based

construction, while thaw subsidence would trigger increased maintenance

costs. Sea level rise (SLR) and coastal erosion would degrade coastal

barriers, damage facilities, and trigger relocation (Dell and Pasteris,

2010).

10.2.3. Transport and Transmission of Energy

Primary energy sources (coal, oil, gas, uranium), secondary energy forms

(electricity, hydrogen, warm water), and waste products (CO

2

, coal ash,

radioactive waste) are transported in diverse ways to distances ranging

from a few to thousands of kilometers. The transport of energy-related

materials by ships (ocean and inland waters), rail, and road are exposed

to the same impacts of climate change as the rest of the transport sector

(see Section 10.4). This subsection deals only with transport modes that

are unique to the energy sector (power grid) or predominantly used by

it (pipelines). Table 10-2 provides an overview of the impacts of climate

change and EWEs on energy transmission, together with the options to

reduce vulnerability.

Pipelines play a central role in the energy sector by transporting oil and

gas from the wells to processing and distributing centers to distances

from a few hundred to thousands of kilometers. With the potential

spread of CO

2

capture and storage (CCS) technology, another important

function will be to deliver CO

2

from the capture site (typically fossil

power plants) to the storage site onshore or offshore. Pipelines have

been operated for over a century in diverse climatic conditions on land

from hot deserts to permafrost areas and increasingly at sea. This

implies that technological solutions are available for the construction

and operation of pipelines under diverse geographical and climatic

conditions. Yet adjustments may be needed in existing pipelines and

improvements in the design and deployment of new ones in response

to the changing climate and weather conditions.

In addition to reduced line-heating and dilution needs due to reduced

viscosity of liquid fuels under warmer temperatures, pipelines will be

affected mainly by secondary impacts of climate change: SLR in coastal

regions, melting permafrost in cold regions, floods washing away

infrastructure, landslides triggered by heavy rainfall, and bushfires

caused by heat waves or extreme temperatures in hot regions. A

proposed way to reduce vulnerability to these events is to amend land

zoning codes, risk-based design, and construction standards for new

pipelines, and structural upgrades to existing infrastructure (Antonioni

et al., 2009; Cruz and Krausmann, 2013).

669

10

Key Economic Sectors and Services Chapter 10

Owing to the very function of the electricity grid to transmit power from

generation units to consumers, the bulk of its components (overhead

lines, substations, transformers) are located outdoors and exposed to

EWE. The power industry has developed numerous technical solutions

and related standards to protect assets and provide reliable electricity

supply under existing climate and weather conditions worldwide.

However, these assets and the reliability of supply may be vulnerable

to changes in the frequency and intensity of EWEs under changing

climate conditions (DOE, 2013). Higher average temperatures increase

transmission efficiency and reduce current carrying capacity, but this

effect is relatively small compared to the physical and monetary

damages that can be caused by EWEs (Ward, 2013). Historically, high

wind conditions, including storms, hurricanes, and tornados, have been

the most frequent cause of grid disruptions (mainly due to damages to

the distribution networks); and more than half of the damage was

caused by trees (Reed, 2008). Other impacts include freezing precipitation,

ice and winter storms, wildfires caused by higher temperatures, less

precipitation, and increased tree death caused by pests. If the frequency

and power of high wind conditions, as well as extreme precipitation

events, will increase in the future, vegetation management along

existing power lines, and rerouting new transmission lines along roads

or across open fields or moving them underground might help reduce

related risks. An important institutional option is to redefine technical

standards to provide incentives for grid operators to implement

appropriate adaptation measures. Such measures are less expensive to

implement as part of the maintenance-renewal cycle than as independent

retrofit measures.

The economic importance of a reliable transmission and distribution

network is highlighted by the fact that the damage to customers tends

to be much higher than the price of electricity not delivered (lost

production, electricity enabled commerce, service delivery, food spoilage,

lost or restricted water availability). Losses can be minimized through

efficient rationing of electricity (de Nooij et al., 2009) if generation is the

limiting factor. Designing and building climate-resilient infrastructure

will depend on technical standards, market governance, and the type

and degree of liberalization and deregulation of grid services.

10.2.4. Macroeconomic Impacts

Most economic research related to climate change impacts on the energy

sector has focused on mitigation rather than the economic implications

of climate change itself. Table 10-3 summarizes the recent studies on the

economic implications of climate change and extreme weather impacts

in the energy sector.

Assessing across a broad array of studies that focus on different regions

and regional divisions, examine different climate change impacts,

include a different mix of sectors, model different time frames, make

different assumptions about adaptation, and employ different types of

models with different output metrics leads to the overall conclusion

that the macroeconomic impact of climate change on energy demand

is likely to be minimal in developed countries (Bosello et al., 2007a,

2009; Aaheim et al., 2009; Jochem et al., 2009; Eboli et al., 2010).

The current literature sheds less light on the implications for developing

countries and on other climate impacts in the energy sector beyond

those related to changes in energy demand. Europe is the focus of most

of the literature so far. Only two studies focus on developing countries:

Mexico and Brazil (Boyd and Ibarraran, 2009; de Lucena et al., 2010).

Asia and Africa are not well represented, appearing as aggregated

regions in only three global studies (Bosello et al., 2007a, 2009; Eboli

et al., 2010). The limited results indicate that developing countries likely

face a greater negative GDP impact with respect to climate change

implications for the energy sector than developed countries, largely

because of higher expected temperature changes (Aaheim et al., 2009;

Boyd and Ibarraran, 2009; Eboli et al., 2010).

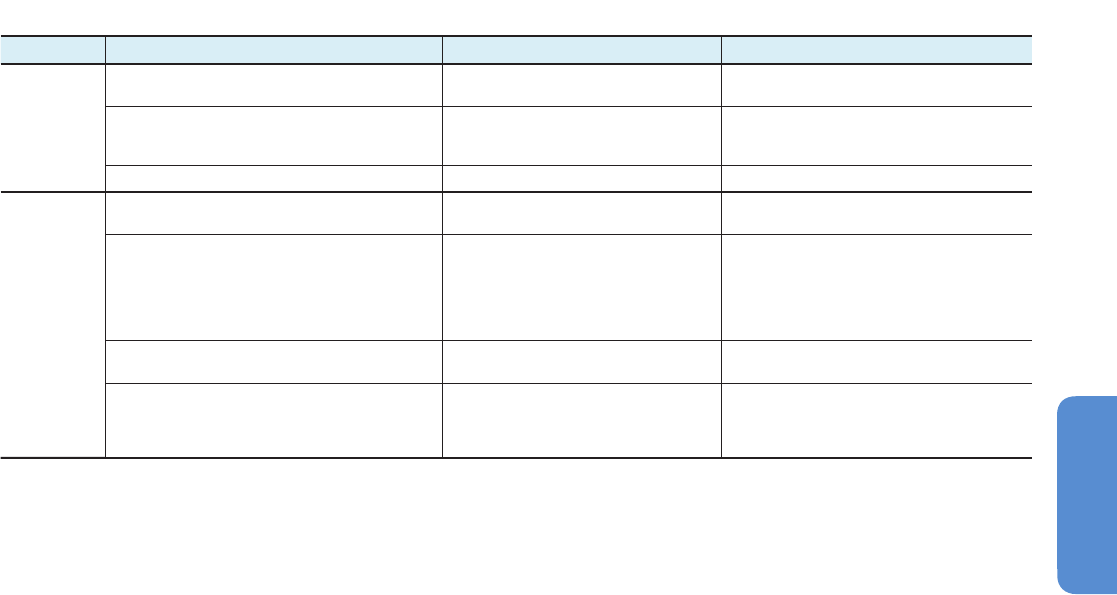

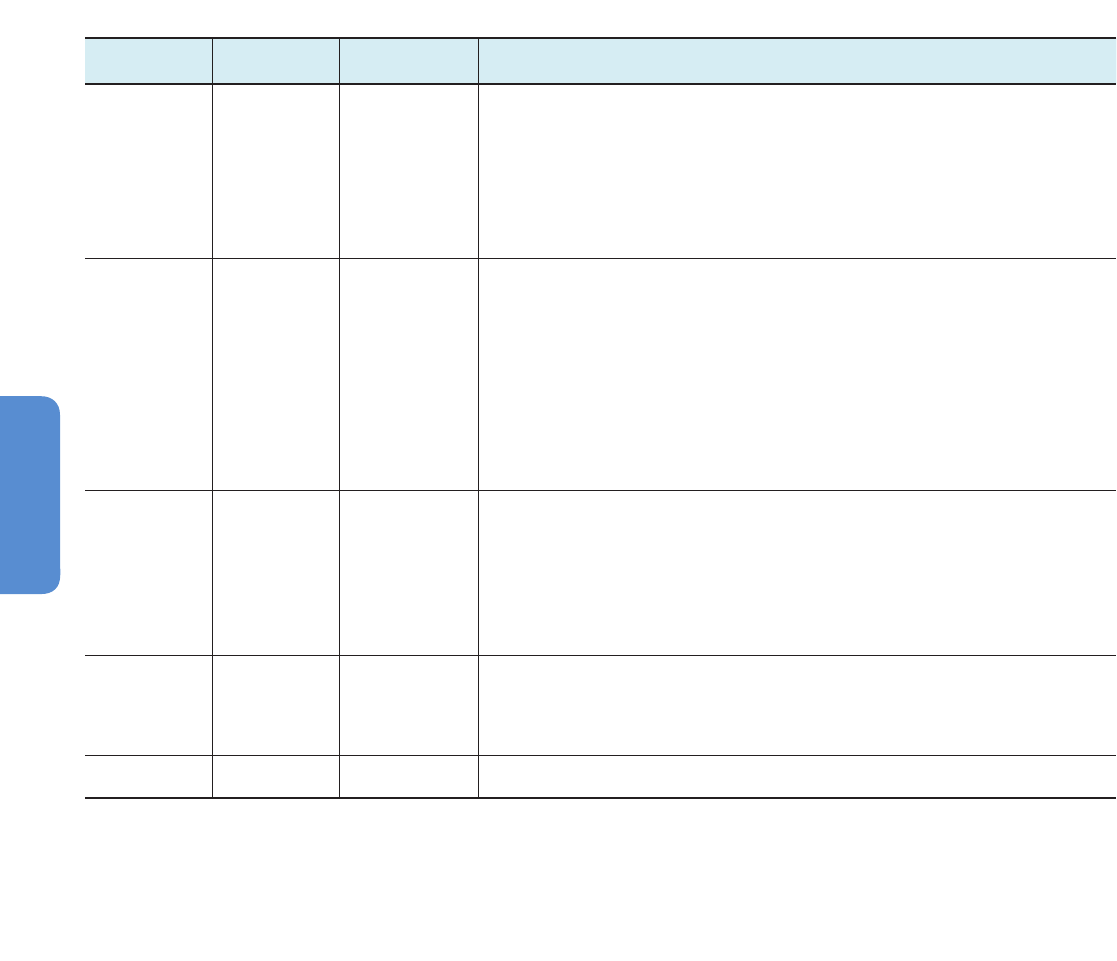

Technology Changes in climatic or related attribute Impacts Adaptation options

Pipelines

Melting permafrost Destabilizing pillars, obstructing access for

m

aintenance and repair

Adjust design code and planning criteria, install

d

isaster mitigation plans

Increasing high wind, storms, hurricanes Damage to offshore and onshore pipelines and

r

elated equipment, spills; lift and blow heavy

objects against pipelines, damage equipment

Enhance design criteria, update disaster preparedness

F

looding caused by heavy rain, storm surge, or sea level rise Damage to pipelines, spills Siting (exclude fl ood plains), waterproofi ng

Electricity grid

I

ncreasing average temperature Increased transmission line losses Include increasing temperature in the design

calculation for maximum temperature

/

rating

I

ncreasing high wind,

storms, hurricanes

D

irect mechanical damage to overhead lines

,

towers

, poles, substations, fl ashover caused by

live cables galloping and thus touching or getting

t

oo close to each other;

indirect mechanical

damage and short circuit by trees blown over or

d

ebris blown against overhead lines

A

djust wind loading standards

,

reroute lines alongside

roads or across open fi

elds; manage vegetation;

improve storm and hurricane forecasting

Extreme high temperatures Lines and transformers may overheat and trip off;

fl

ashover to trees underneath expanding cable

Increase system capacity,

increase tension in the line to

r

educe sag,

add external coolers to transformers

Combination of low temperature

, wind and rain, ice storm

Physical damage (including collapse) of overhead

lines and towers caused by ice build-up on them

Enhance design standard to withstand larger ice and

wind loading,

reroute lines alongside roads or across

o

pen fi

elds; improve forecasting of ice storms impacts

on overhead lines and on transmission circuits

Table 10-2 | Main impacts of climate change and extreme weather events on pipelines and the electricity grid.

Sources: Bayliss (1996); Krausmann and Mushtaq (2008); Reed (2008); Hines et al. (2009); Winkler et al. (2010); Vlasova and Rakitina (2010); McColl (2012); Cruz and

Krausmann (2013); Ward (2013).

670

Chapter 10 Key Economic Sectors and Services

10

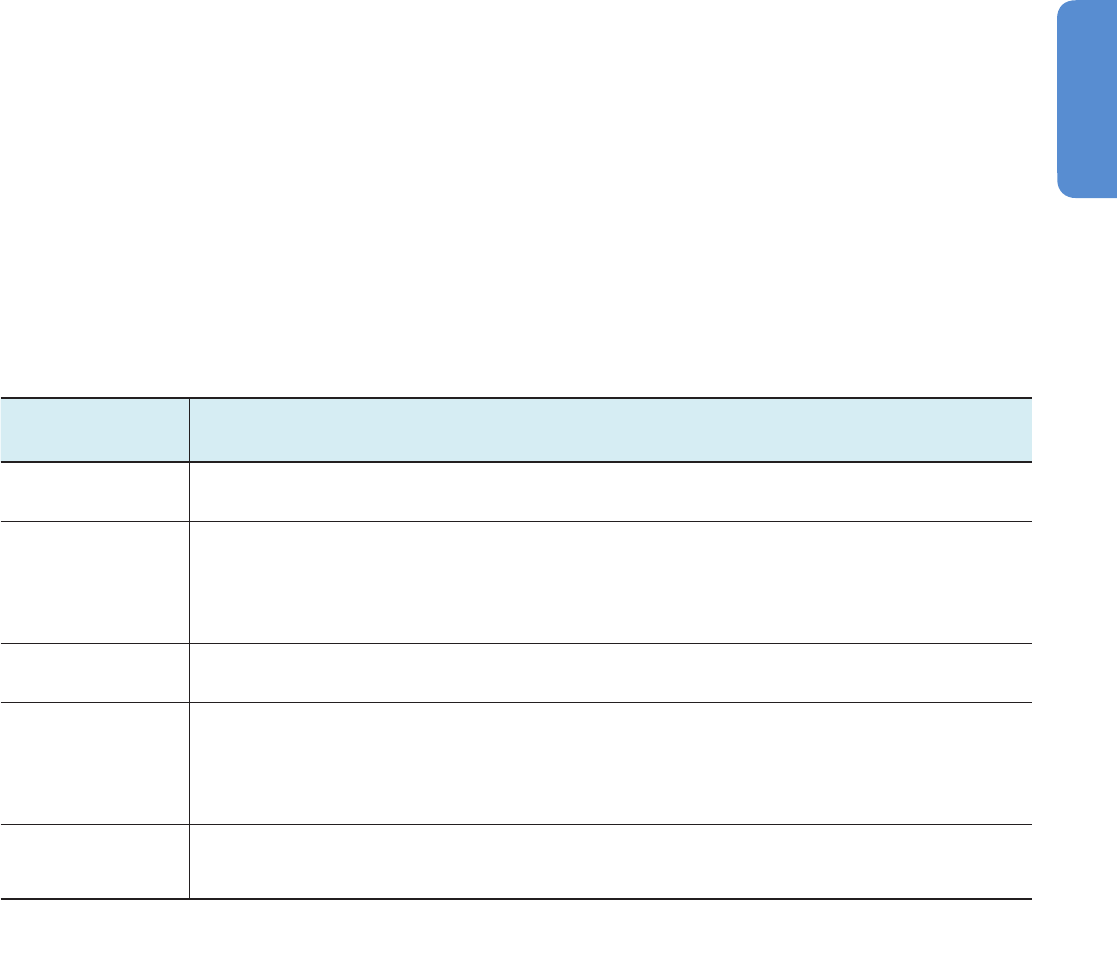

Study

Model

type

Climate impacts modeled Energy /economic impacts Regions

Sectors

studied

B

osello et al.

(2009)

I

AM Rising temperatures /changing demand for energy; impacts from

four other sectors /events (Global, 2001– 2050)

C

hange in gross domestic product (GDP) in 2050 due to

rising temperatures and changing energy demand: 0 – 0.75%

(

+1.2°C); – 0.1% to 1.2% (+3.1°C)

1

4 4

J

orgenson et al.

(2004)

C

GE Rising temperatures /changing demand for energy; climate

impacts from three other sectors (USA, 2000 – 2100)

O

ptimistic adaptation: 4 – 6.7% higher energy productivity per

year (2000 – 2100)

O

utput from electricity: – 6% in 2050; GDP is +0.7% (aggregate

all sectors, average annual 2000 – 2100)

P

essimistic adaptation: 0.5 – 2.2% lower energy productivity

per year

O

utput from electricity: +2% in 2050; GDP is – 0.6% (aggregate

impact all sectors)

1

35

B

osello et al.

(2007a)

C

GE Rising temperatures /changing demand for energy (Global, 2050) Change in GDP in 2050 (perfect competition): – 0.297% to

0.027%

C

hange in GDP in 2050 (imperfect competition): – 0.303% to

0.027%

8

1

Aaheim et al.

(

2009)

CGE Change in precipitation

affects share of hydroelectric power;

r

ising temperatures /changing demand for energy; impacts from

four other sectors (Western Europe, 2071– 2100)

Impact from all sectors in 2100: GDP in cooler regions: – 1%

t

o – 0.25%

GDP in warmer regions: – 3% to – 0.5%

Adaptation can mitigate 80 – 85% of economic impact

8 11

Boyd and

I

barraran

(2009)

CGE Drought scenario affecting hydroelectric plus three other sectors

(

Mexico, 2005 – 2026)

• Generation output in 2026: – 2.1%

•

R

efi ning output: – 10.1%

• Coal output: – 7.8%

•

N

G output: – 2%

• Crude oil output: +1.7%

• GDP: – 3%

With adaptation:

• Generation output in 2026: 0.24%

• Refi ning output: 1.36%

• Coal output: 1.09%

• NG output: 0.34%

• Crude oil output: 0.22%

• GDP: 0.33%

1 2

Jochem et al.

(2009)

PE /CGE Rising temperatures /changing demand for energy; change in

technical potential of renewables; change in rainfall induces

change in hydroelectric production; high temperatures induce

water temperatures exceeding regulatory limits (Europe); high

temperatures induce greater electric grid losses and lower

thermal effi ciency; generic extreme events induce reduced

capital stock in CGE model (EU27+2, 2005 – 2050)

• GDP (Europe): – 50 billion € p.a. in 2035

• GDP (Europe): – 240 billion € p.a. in 2050

• GDP (EU regions): – 0.1% to – 0.4% in 2035

• GDP (EU regions): – 0.6% to – 1.3% in 2050

• Jobs (Europe): – 380K in 2035

• Jobs (Europe): – 1 million in 2050

25 1

Eboli et al.

(2010a)

CGE Rising temperatures /changing demand for energy; climate

impacts in four other sectors modeled (Global, 2002 – 2100)

By 2100, change in GDP due to climate impacts on energy

demand vary by country between about – 0.15% and 0.7%.

USA and Japan were negative and all other countries positive.

Overall economic impact from all sectors is neutral to positive

for developed countries and negative for developing ones.

8 17

Golombek et al.

(2011)

PE Rising temperatures /changing demand for energy; rising

temperatures /reduced thermal effi ciency; change in water

infl ow (Western Europe, 2030)

Net impact on the price of electricity is a 1% increase.

Generation decreases by 4%.

13 4

de Lucena et al.

(2010)

PE Changing precipitation induces change in hydroelectric

production; rising temperatures induce lower NG thermal

effi ciency; rising temperatures induce change in demand for

energy (Brazil, 2010 – 2035)

New generating capacity needed to produce additional

153 – 162 TWh per year.

Capital investment of US$48 – 51 billion, which is equivalent to

10 years of capital expenditures in Brazil’s long-term energy

plan.

US$6.9 – 7.2 billion in additional annual operating expenses for

each year in which worst-case hydroelectric production occurs

1 11

Bye et al. (2008) PE Water shortages (Nordic countries, hypothetical 2-year period) Water shortage scenarios can lead to a 100% increase in

electricity prices at peak demand over a 2-year period. Higher

prices lead to marginal reductions in demand (about 1 – 2.25%).

41

Koch et al.

(2012)

PE High temperatures induce water temperatures exceeding

regulatory limits (Berlin, 2010 – 2050)

Thermal plant outages amounting to 60 million € for plants in

Berlin through 2050

11

Gabrielsen et al.

(2005)

Econometric Rising temperatures /changing demand for energy; change

in water infl ow; change in wind speeds (Nordic countries,

2000 – 2040)

Net change in electricity supply in 2040: 1.8%

Change in electricity demand: 1.4%

Change in electricity price: – 1.0%

41

Table 10-3 | Economy-wide implications of impacts of climate change and extreme weather on the energy sector.

671

10

Key Economic Sectors and Services Chapter 10

Despite the considerable number of potential climate change and

extreme weather phenomena—higher mean temperatures, changes in

rainfall patterns, changes in wind patterns, changes in cloud cover and

average insolation, lightning, high winds, hail, sand storms and dust,

extreme cold, extreme heat, floods, drought, fire, and SLR—and their

potential impacts on electricity generation and transmission systems,

fuel infrastructure and transport systems, and energy demand (Williams,

2013), the range of impacts modeled in the literature (Table 10-3) is quite

limited. Most studies consider changing energy demand (specifically,

changes in electricity and fuel consumption for space heating/cooling)

resulting from rising temperatures as the only or primary climate change

impact. These studies draw on recent literature refining the relationship

between climate change and energy demand: the demand for natural

gas and oil in residential and commercial sectors tends to decline with

climate change because of less need for space heating, and demand for

electricity tends to increase because of greater need for space cooling

(Gabrielsen et al., 2005; Kirkinen et al., 2005; Mansur et al., 2005;

Eskeland and Mideksa, 2010; Mideksa and Kallbekken, 2010; Rübbelke

and Vögele, 2010).

Studies using a Computable General Equilibrium (CGE) model that

consider only climate impacts in the energy sector find that the effect

on GDP in 2050 is in the range of –0.3% to 0.03% (Bosello et al., 2007a)

and –1.3% to –0.6% (Jochem et al., 2009). These findings are largely

consistent despite the fact that Bosello et al. (2007a, 2009) are global

studies that model only the change in demand due to rising temperatures,

whereas Jochem et al. (2009) focus on the European Union (EU) and

model the change in demand plus six other climate impacts.

Studies using CGE models that examine the aggregate changes in GDP

brought on by climate impacts in energy and several other sectors have

also primarily found similar shifts in GDP. Aaheim et al. (2009) conclude

that in 2100 in cooler regions in the EU, GDP changes by –1% to –0.25%

and in warmer regions changes by –3% to –0.5%. Boyd and Ibarraran

(2009) project a –3% change in GDP in 2026 for Mexico, consistent

with the warmer regions modeled by Aaheim et al. (2009). Roughly

consistent with each other, Aaheim et al. (2009) and Eboli et al. (2010)

find GDP impacts for the predominantly cooler regions of Japan, the EU,

Eastern Europe and the Former Soviet Union (EEFSU), and Rest of Annex I

as having a “significant positive impact,” while the predominantly

warmer regions of the USA, EEx (China/India, Middle East/Most of

Africa/Mexico/parts of Latin America), and the Rest of the World have

a “significantly negative impact.” Jorgenson et al. (2004) find that

overall GDP impacts are –0.6% to 0.7% in 2050 for the USA, which

stands in contrast to Eboli et al. (2010) with a “significantly negative

impact” in the USA.

Several CGE studies attempt to evaluate how adaptation changes in

the energy sector impact GDP but do not examine specific adaptation

options since CGE models lack the necessary technological detail. They

make general assumptions about the effectiveness of adaptation policy

in reducing climate impacts. Jorgenson et al. (2004) find that pessimistic

assumptions about adaptation imply a 0.6% reduction in GDP in 2050

but optimistic assumptions lead to a 0.7% gain in GDP. Aaheim et al.

(2009) conclude that adaptation can mitigate the costs of climate change

by 80% to 85%, and Boyd and Ibarraran (2009) find that adaptation

can shift a 3% GDP loss in 2026 in Mexico to a gain in GDP of 0.33%.

Partial equilibrium models, by their nature, do not have a full

macroeconomic representation and therefore rarely report changes in

GDP. Instead, these models focus on details in the energy sector, such

as price and quantity effects for fuels and electricity (and the mix of

generation). For example, Rübbelke and Vögele (2013) conclude that the

short-term effects of climate-related problems affecting water cooling

and hydropower production can have negative distributional effects. de

Lucena et al. (2010) find that rising temperature and changing precipitation

lead to the need for an additional 153 to 162 TWh per year by 2035

with a capital investment of US$48 to 51 billion.

Golombek et al. (2011) report a 1% increase in the price of electricity

for Western Europe in 2030 stemming from rising temperatures that

affect demand and thermal efficiency of supply, as well as water inflow.

UNDP (2011) finds between a 0.06% and 1.74% increase in electricity

system costs for Macedonia resulting from temperature changes.

Gabrielsen et al. (2005) conclude that for Nordic countries in 2040, as

a result of rising temperatures that affect demand, changes in water

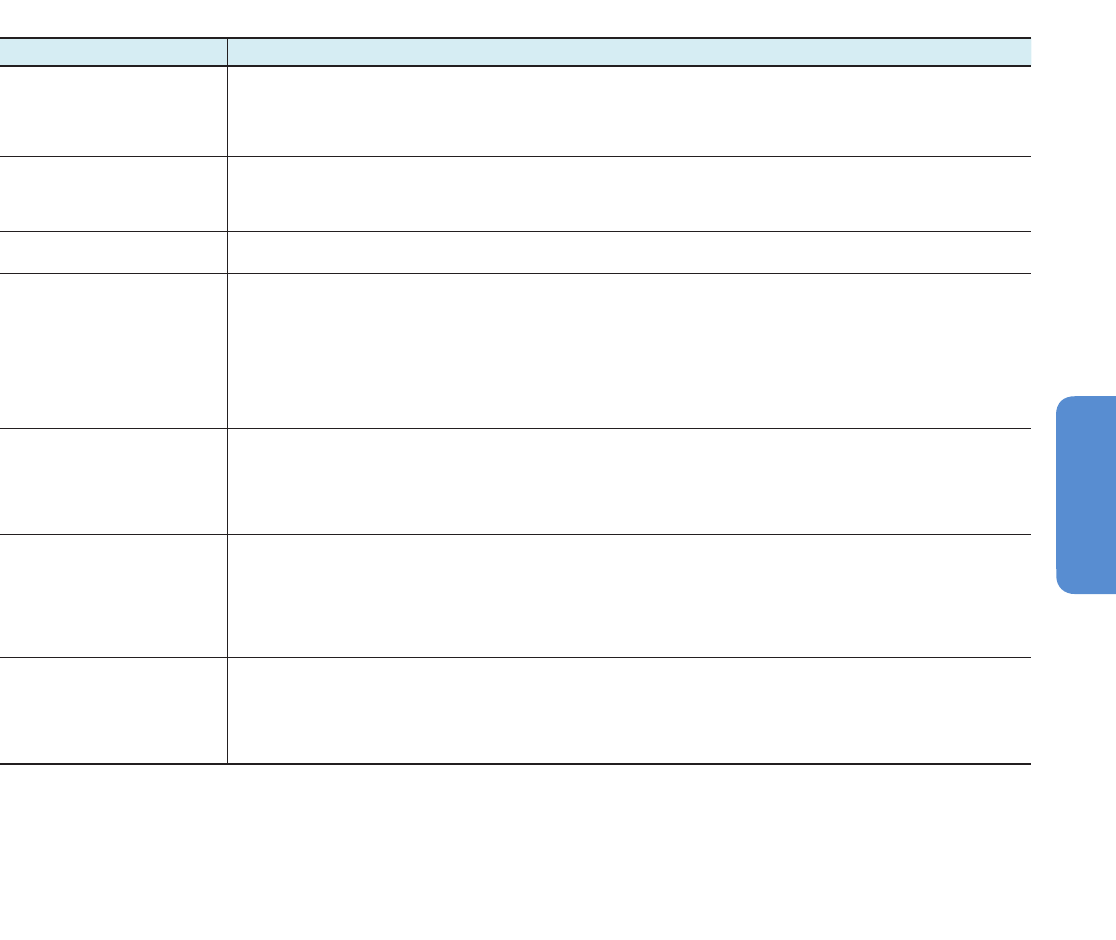

Study

Model

type

Climate impacts modeled Energy /economic impacts Regions

Sectors

studied

UNDP (2011) PE Damage Case 1 (DC1): hotter in both winter and summer—

d

ecreased demand for heating and increased demand for

cooling;

D

amage Case 2 (DC2): colder in both winter and summer—

increased demand for heating and decreased demand for

c

ooling;

Damage Case 3 (DC3): colder in the winter and hotter in the

s

ummer—increased demand for heating and increased demand

for cooling (Macedonia, 2009 – 2030)

Change in electricity demand in residential and commercial

s

ectors:

• DC1: 3.5%

•

D

C2: 0.3%

• DC3: 8%

C

hange in electricity system cost:

• DC1: 0.8%

•

D

C2: 0.06%

• DC3: 1.74%

95

D

OE (2009) PE Drought scenario (Western Electric Coordinating Council, USA,

2010 – 2020)

I

n 2020, 3.7% reduction in coal generation; 43.4% increase in

NG generation; 29.3% reduction in hydroelectric generation.

Production cost increase of US$3.5 billion. Average monthly

e

lectricity prices up 8.1% (Nov) to 24.1% (July)

1

1